Yeah my bad, I’d have posted that in Sept had I heard of Kerrisdale before yesterday. Yesterday I made an effort to compile a list of short activist funds/individuals, and when I bookmarked that page I happened to see ASTS. It doesn’t surprise me, I knew it was a lottery ticket stonk but didn’t know it was this big of a longshot or that dilution was near. At some point the reddit hype made me suspect it was overpriced, so I sold with the plan of buying back in later just to play the test launch pump. That pump came sooner than I expected and I was distracted and missed it.

In light of the report, ASTS might be a good short but I’ll pass unless another pump tempts me to play the dump. I’m short enough companies at the moment.

They had a pretty big miss on ad revenue. Looks like it’s still at 22 - 25x forward pe based on the report today. I’m still long some shares but it’s not as great of a buy as it might seem if earnings growth slows by this much.

The miss on YouTube ad rev is the big hit. I believe this is the first time that YouTube revs declined quarter over quarter. And the decline wasn’t insignificant, about 7%.

The question to ask: is the platform growth slowing or is it a bellweather for the economy?

On the other hand, suppose that operating income declines a bit year-over-year. So maybe $77 billion of operating income (compared to $78.7 billion last year). Apply a conservative 20% tax rate to get to after-tax operating income of $61.6 billion. Unless I’m screwing something up, that’s a P/E ratio of about 22, closer to 20 when you account for excess cash on the Balance Sheet.

You don’t need a ton of growth to make that an attractive price to pay for a business that is almost certainly going to exist in 10-20 years. Moreover, you could sort of view almost any growth as gravy, since they’ve recently been paying out most of their net income in terms of repurchases. Just looking at the recent 10-Q, they repurchased $36.8 billion relative to $55.39 billion in earnings for the first 9 months of 2021 (66%), and repurchased $43.9 billion relative to $46.3 billion in earnings for the first 9 months of 2022 (79%). So it’s really hard to expect a firm to grow earnings materially if they’re not retaining their earned capital.

Again, I don’t own individual stocks, so I’m not a buyer here or anywhere else. But it strikes me as a very reasonable investment to make at this price.

Today and tomorrow are my days to re-assess all of my positions and decide if I’m making any new moves. I’m leaning towards buying more, but I’m only like 60-40. Partially because I don’t want to be too overweight on it, and partially because I think there will likely be more value options available and I may want to add a couple and still maintain adequate dry powder.

"The phase 1 ruling, issued on September 1, 2022, said that the merger “may be expected to result in a substantial lessening of competition within a market or markets in the United Kingdom”.

Maybe they are flexing their post-Brexit sovereignty?

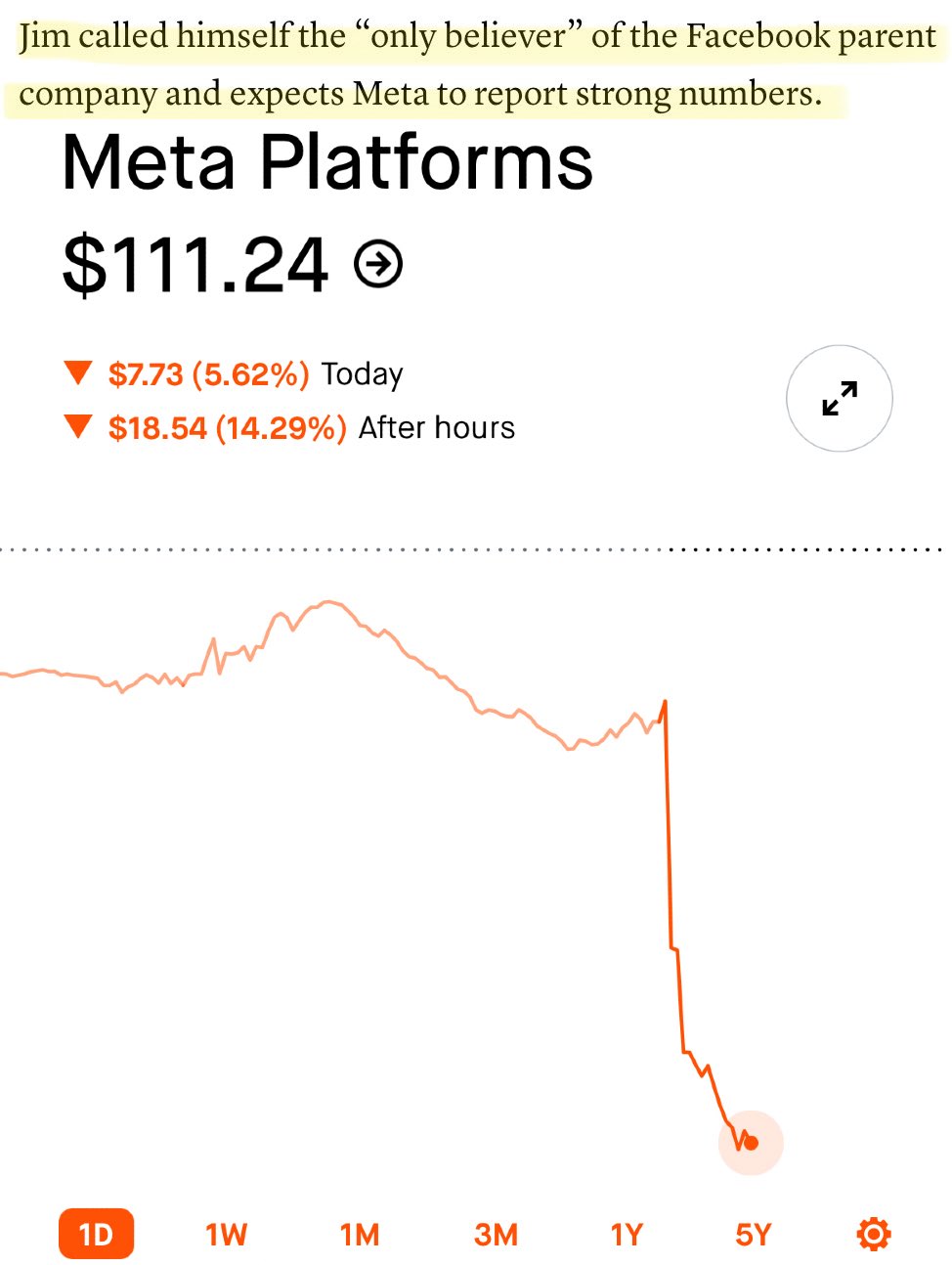

I didn’t touch any individual big tech stocks until META tanked to $205… well that’s going great. The only saving grace is I know I’m a moran so I sized the bet appropriately.

Just as an aside, everything theatre debt is in free fall. AMC first lien now back at 70 (might be pandemic low levels I can’t remember), PIK notes trade north of 30 percent.

Very very very real chance that equity is a zero as soon as 2023.

I hate Facebook in its theory and its practice and I’ve never bought a share of FB/Meta but I am tempted to shove some serious money in at 105. This seems like their blood in the street moment and some idiot today tried to compare them to Netflix like it connected in any way - and he ended up being wrong on them too at 180. Facebooks still has a ton of power.