Just to comment on the won’t crypto get vaporized if the stock market really crashes question, the answer there is probably yes. But crypto has basically already crashed. BTC/ETH are off almost 50% from late 2021 highs and most shitcoins are down much more. It’s also actually up since the night of the invasion in the 5-10% range.

It’s maybe arguable crypto prices are a bit of a leading indicator rather than the other way around also. Partially because they trade 24/7. I think it’s possible they digest and reflect current events faster than the S&P 500 for example.

For all the bullshit tech bro arguments for crypto, the reality is that the vast majority of “investors” are just speculators YOLOing. There is no value investing in crypto - it’s fake money that doesn’t produce anything. If the shit really hits the fan in equities, crypto will go down a lot more than 50%.

Yeah that’s like saying the stock market has already crashed bc we are 12% off ATHs. If we get a true crash this is only the beginning for both stonks and crypto

I wouldn’t really say btc has crashed. Btc did drop 85% in 2018 when the market subsequently ended up dropping around 15% later that year. I do agree that it’s generally in order of…meme stocks/coins/leveraged companies/cash reserved behemoths but folks are no where near ready to accept the possibility of prices reaching 2015 levels or 50 billion dollar companies that IPO’d after 2016 completely disintegrating or bitcoin at 2k when they’ve seen dips get bought up for 13 years.

So just to update the QIWI situation because it seems interesting to others based on responses, it’s still halted (at $4.94) but I’m starting to think there’s a significant non-zero chance that it doesn’t go to $0 and maybe even goes up when it resumes (if it ever does).

They claim that they have not had to suspend services at all and have not been impacted directly by the sanctions, they do however have a ton of exposure to the Russian economy of course.

But the most important thing is that their book value was $5.47 a share at their last filing, with $6.34 per share in cash. Their filings are in rubles, but they released a statement that their cash on the balance sheet is held in dollars, and the cash in customers accounts is like 99% in local currency for the customers. As a result, they have very little direct currency risk.

Meanwhile they were starting to get into crypto before all this happened, and some of their largest competitors have been absolutely and completely wrecked by the sanctions.

I could see a lot of Russians deciding they’d rather put some money in a QIWI wallet and use it for crypto as opposed to keeping it in rubles, so I wouldn’t be surprised if they’re doing a ton of business right now. And on the one hand that’s sort of helping evade sanctions, but it’s on an individual average person level, and if that’s the case it’s also helping the Russian people divest from rubles and that to me is probably bad for Putin and good for the world, but perhaps someone else here knows better and I’m wrong on that point?

All that said, who knows if/when I’m ever allowed to trade it or receive dividends from it. So it’s quite the interesting situation. I’m still counting it as $0.00 in my head, but it’s interesting to follow.

This doesn’t make sense.

Either both assets and liabilities are denominated in the same currency, and they don’t have foreign currency risk, or they’re denominated in different currencies and they do have currency risk.

They are primarily traded on MOEX (if it ever reopens), with an ADR on NASDAQ. Their official filings are on MOEX, so their entire filing is denominated in rubles, but their cash on hand is held in dollars.

Around 99% of their customers’ balances are in local currencies for the customers, regardless of location, so that risk is on the customers’ end not theirs.

They haven’t specified, but I would imagine that some of their liabilities are contracted in rubles, though, which would be good for them if their cash was held in dollars.

Yeah, I’m 99% sure CW is reading the statement wrong (unless there is another statement about just cash reserves). Here it is - “We would like to highlight QIWI’s strong financial position with negative Net Debt and an equivalent of RUB 35.5 billion of cash and cash equivalents as of the end of 3Q 2021. Our business has limited exposure to currency risks, as majority of our operations and over 98% of cash balances are nominated in local currency.”

That seems to imply that they don’t have currency risk since their cash assets match their cash liabilities (which makes sense). So if the rubble plummets they have no currency risk since both their assets and liabilities for their Russian business will move in the same direction, but the value of their cash in USD terms will go down.

I think you might also be confusing assets and liabilities?

Financial institutions need to make sure that their assets (cash and investments on hand) are well-aligned with their liabilities (the customer balances/deposits that represent an obligation on the part of the financial institution). So if there are customer balances in a foreign currency (which there seems to be here), the financial institution needs to maintain assets in that foreign currency in order to satisy those liabilities. Failure to match would represent currency for the financial institution.

Sorry for piling on, but this doesn’t appear to be right? On their most recent filing (that I know of), they list total equity attributable to equity holders of the parent of 41,175RUB. With 62.4 million shares outstanding, that’s 660RUB/share of book value. At current exchange rates, that translates to about $4.82 per share in book value as of 9/30/2021. I mean, I’m sure book value per share in US$ was much higher several months ago, but that seems fairly irrelevant right now.

No, if I’m misunderstanding something it’s not that statement. That statement got me to do some additional digging into how they handle their cash balances, and I’m not 100% sure but I think they hold a substantial amount of their own cash balances in dollars. Not their customers’ cash balances, the company’s cash balances.

This is the key part. They didn’t have 35.5 billion rubles in cash at the end of Q3, they had an equivalent of it. If you dig into their balance sheet and some of the fine print in their 20-F, they state that their profits for the year will go up if the dollar rises against the ruble, due to balances held in dollars.

The impact on the Group’s profit before tax is due to changes in the carrying amount of monetary assets and liabilities denominated in US Dollar and Euro when these currencies are not functional currencies of the respective Group subsidiary. The Group’s exposure to foreign currency changes for all other currencies is not material.

But those wash out. To simplify this, if QIWI has $1M USD in cash owned by the company, and their customers’ accounts are holding a billion rubles, when the ruble crashes their customers get wiped out, not them. They are hurt by the earnings going forward, of course, because their fees and thus earnings are going to be received and denoted in rubles. However, their existing cash balance is would not be hurt.

Am I missing something? I think I might not have been clear about what I meant.

For the purposes of the discussion and saving time, I just pulled them off Schwab, which probably stopped updating them with the exchange rate when QIWI was halted.

Yeah when I bought it, book value was $8.64 per share.

I mean given that the majority of their assets are cash holdings, and given that the customers accounts are going to zero out between assets/liabilities because they’re maintained in local currency, the question is what the remainder of the cash holdings are in.

If I’m correct and they’re largely in dollars, then simply applying the current RUB/USD exchange rate to the entire balance would not yield the correct current book value. If I’m wrong, then they’re lying and their currency risk is massive and they’re getting wiped out.

I guess another way to put it is the only people who know the actual current book value are the people at QIWI who know exactly what currencies the company’s cash holdings are in. But, I think some of the breadcrumbs in their filings seem to indicate a substantial amount in US dollars. There are numerous notes about converting everything to RUB at the exchange rates at the time of filing for the purposes of the filings, and that the actual money is held in a variety of currencies. There are other notes about significant dollar exposure.

I don’t think there’s any reason to believe that a financial institution would hold its liquid assets in a different currency than its primary short-term customer deposits. That generates currency risk. You can’t say, “Well, they hold non-risky U.S. dollars in assets and have liabilities denominated in risky Rubles that are probably worthless, so they don’t face any risk.” Of course they would have risk in that scenario!

But we don’t need to speculate. It’s laid out pretty clearly in the 20-F, and I’m not sure what has made you think they hold a substantial amount of U.S. dollars.

The 20-F is here.

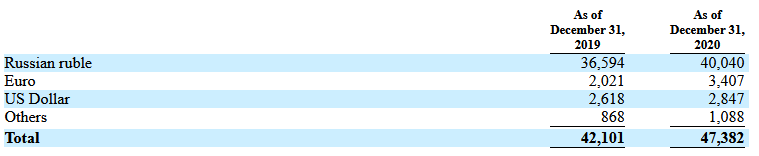

Their Balance Sheet (statement of financial position) shows cash and cash equivalents of 47,382 (in millions of Rubles)