We’re always stonking.

Stonks up → booming corporate profits, BUY BUY BUY.

Stonks down → opportunity get in while prices are attractive, BUY BUY BUY.

We’re always stonking.

Stonks up → booming corporate profits, BUY BUY BUY.

Stonks down → opportunity get in while prices are attractive, BUY BUY BUY.

Yup every winning play I made today was to the short side. I guess something had to give, what with indices bumping into new ATHs almost daily lately. They have to take profits sooner or later.

NVDA and TSLA are getting nailed quite hard.

CNBC bubbleheads blame TSLA drop on them moving the “robotaxi rollout” ![]() back from 8/8 to October. Anyone with a brain knew that tweet he made saying that it was coming “8/8” was just another nazi moment from Elmo and there was never a plan to debut a new car on August 8th. (And I’ll be shocked if there is one come October, either….Elmo is just getting it out there now so it doesn’t further wreck what should be another train wreck earnings call.) That shit is obviously overbought as hell. It’s up to $250 on basically no news outside of finally hitting a delivery target along with Elmo saying “AI” a lot.

back from 8/8 to October. Anyone with a brain knew that tweet he made saying that it was coming “8/8” was just another nazi moment from Elmo and there was never a plan to debut a new car on August 8th. (And I’ll be shocked if there is one come October, either….Elmo is just getting it out there now so it doesn’t further wreck what should be another train wreck earnings call.) That shit is obviously overbought as hell. It’s up to $250 on basically no news outside of finally hitting a delivery target along with Elmo saying “AI” a lot.

DAL and PEP also both fell off a cliff after downbeat outlooks in their earnings calls.

ETA though PEP recovered through the day and actually finished positive

I’ve been shopping interest rates for a new build. Within the last 7 days they have dropped from 7.25% to 6.25% on a 7/1 ARM. I don’t see how house prices don’t soar if this keeps up.

Supply and demand can be fickel. If everyone who was waiting for rates to come to sell there home decided to sell there home you might end up with a dynamic of 2 sellers for every buyer. In that case prices will come down even with lower rates.

If rates come down and prices go up then prospective buyers will still have an affordability problem. Nothing changes in that scenario and lots of buyers will still not be able to qualify for the loan.

It’s not high prices or high rates that are preventing people from buying a home. It’s the inability to get qualified for the mortgage.

Damn how much higher can they go though?

I know zip codes can fluctuate wildly, but in FL we have a weird situation where houses* are still expensive as hell compared to ten years ago, there’s a ton of supply yet no one is buying. I don’t even know how that’s possible.

*but not condos, you can get a nice beachside condo for relatively dirt-cheap now. At least it will be dirt cheap until your first assessment.

My college buddy and his wife just sold their home outside Boston and moved down to the east coast of Florida to temporary digs while they looked for a place to buy. This is what he wrote:

The prices are coming down here, but still way up from 2020/2019. Sellers tried to take advantage and they are coming down now. Lots of inventory sitting on the market.

We started looking in Boynton Beach and Delray and it has turned into Long Island with palm trees.

People from NY in their mid/late 80s selling houses that had not been updated since they bought them in the late 90s, looking for well over 700K for small 2-3 bedroom homes. Stacy nearly gagged going into them. After a week of that, we realized it was not for us and went up north and loved it.

They actually are set to close on a house up near Port St. Lucie.

Yeah, like I said location plays a huge role here.q they will probably be happier up there, we vacation down there yearly and it’s a great area. Metro Miami’s market is one of the most ridiculous in the country: overpriced houses that are difficult-to-impossible to insure, and condos whose prices are plummeting to aughts levels which sounds awesome.

But then you find out that the reason those prices are cratering is because condo boards are ramping up assessments to cover their asses in the wake of new legislation passed after the Surfside building collapse. Condo owners who can’t afford their share of assessments, which are five-six figures, are being forced to let their units go at fire sale prices IF they can even find a buyer rich (dumb) enough to buy in to that shitshow.

I have been looking into establishing a HELOC and my own 3/2 was appraised at over $315k just recently. I bought in 2016 for $152k.

Does there exist a diversified ETF (ideally a Vanguard product) that acts as a hedge to the S&P 500?

My favorite ETF is VOO, which is one of Vanguard’s flagship ETFs that tracks the S&P 500, with an industry leading expense ratio of just 3 basis points.

In a macro sense, I’m long for big US tech companies, which have been among the best asset classes in US history. However, I think there’s some chance that the current AI boom could be a bubble. I can’t say when it’ll happen, but we’re overdue for a recession at some point. If it does pop, I think it could hit tech stocks particularly hard.

All my retirement savings, and my taxable brokerage account, are in diversified index funds, so I feel like I’m doing the right things.

What I want to know is, if there’s a systemic market correction coming, what could I add to my portfolio now that would do better in the event of a big tech market pullback?

I’m not sure the kind of tactical moves one would make to anticipate a “big tech market pullback,” since it’s not like “tech” is being replaced by other industries.

I think the best plan is just to construct your portfolio so that you’re prepared for the inevitable slowdown / correction.

Cash?

![]()

Yes there are many options depending on your broker. What brokerage do you use?

Fidelity.

Basically I was wondering if there was an easily identifable asset class that’s negatively correlated with the big tech stocks that make up the S&P.

Whether that’s small caps, bonds, gold, btc, cash, whatever.

Also this ![]() Cash and equivalents work great. Not investment advice obv but if I felt like we were facing another 2022-like downturn, I’d have no problem at all selling all my equities and shipping my cheese straight into something like a money market fund. Unfortunately not all brokerages offer this as an option which is why I asked. Like for example Webull only offers two or three kind of crappy MMF’s with crappy expense ratios, and those are all strictly worse options than letting the cash sit in their Cash Management account for a straight 5% apy with no fees.

Cash and equivalents work great. Not investment advice obv but if I felt like we were facing another 2022-like downturn, I’d have no problem at all selling all my equities and shipping my cheese straight into something like a money market fund. Unfortunately not all brokerages offer this as an option which is why I asked. Like for example Webull only offers two or three kind of crappy MMF’s with crappy expense ratios, and those are all strictly worse options than letting the cash sit in their Cash Management account for a straight 5% apy with no fees.

Robinhood doesn’t offer ANY mutual funds, whether or not the fees suck, but if you have Robinhood Gold you get the same 5% that Webull offers. Another excellent option you can get with pretty much any brokerage is a bond ETF. If we are in a severe downturn, interest rates will be falling, so the yields won’t be great on a bond ETF like it is now, but at least you won’t have to worry about your cash evaporating.

I carry some SCHQ, which follows the 10-year and I like to keep an eye on the 10-year as so much of the rest of the economy revolves around it. It currently sports a 30-day yield of 4.51% and has an expense ratio of .03% which is as low as anything Vanguard offers. I’m sure there is a Vanguard equivalent if you simply must have one of their funds.

Other options include floating rate inflation-protected ETFs like TFLO, .15% ratio and over 5% yield currently. Or if you don’t mind trading a bit more risk for higher yield you can look into JAAA. It’s a collateralized loan obligation fund, so a bit riskier than a straight government bond fund, but the bonds are AAA rated and the 30-day yield is currently almost 7%.

I am also building up a position in NDMO in my taxable trading account. It’s a Nuveen muni fund. The expense ratio is kind of high (over 1%). However, this is highly mitigated by the fact that it yields a nominal rate of nearly 7%, with the added benefit of distributionss being exempt from federal income taxes. So the tax equivalent yield is well over 7%.

So when the reaper comes just dump your equities and dump into these safe havens. IMHO there’s no need to “hold” shit through downturns. Just sell and buy back in later at a lower cost. This will of course exacerbate the stock crash because it’s not like we just invented this concept right here and now, but wtf do we care amirite??

I have an online high yield savings account that I like with a 5.1% APY.

If I were staring at the landscape that looked like March 2020, you think I should just liquidate and dump it into the HYSA?

I think I’d probably just ride it out in my retirement accounts. My time horizon is long enough that I don’t want to try to time the market.

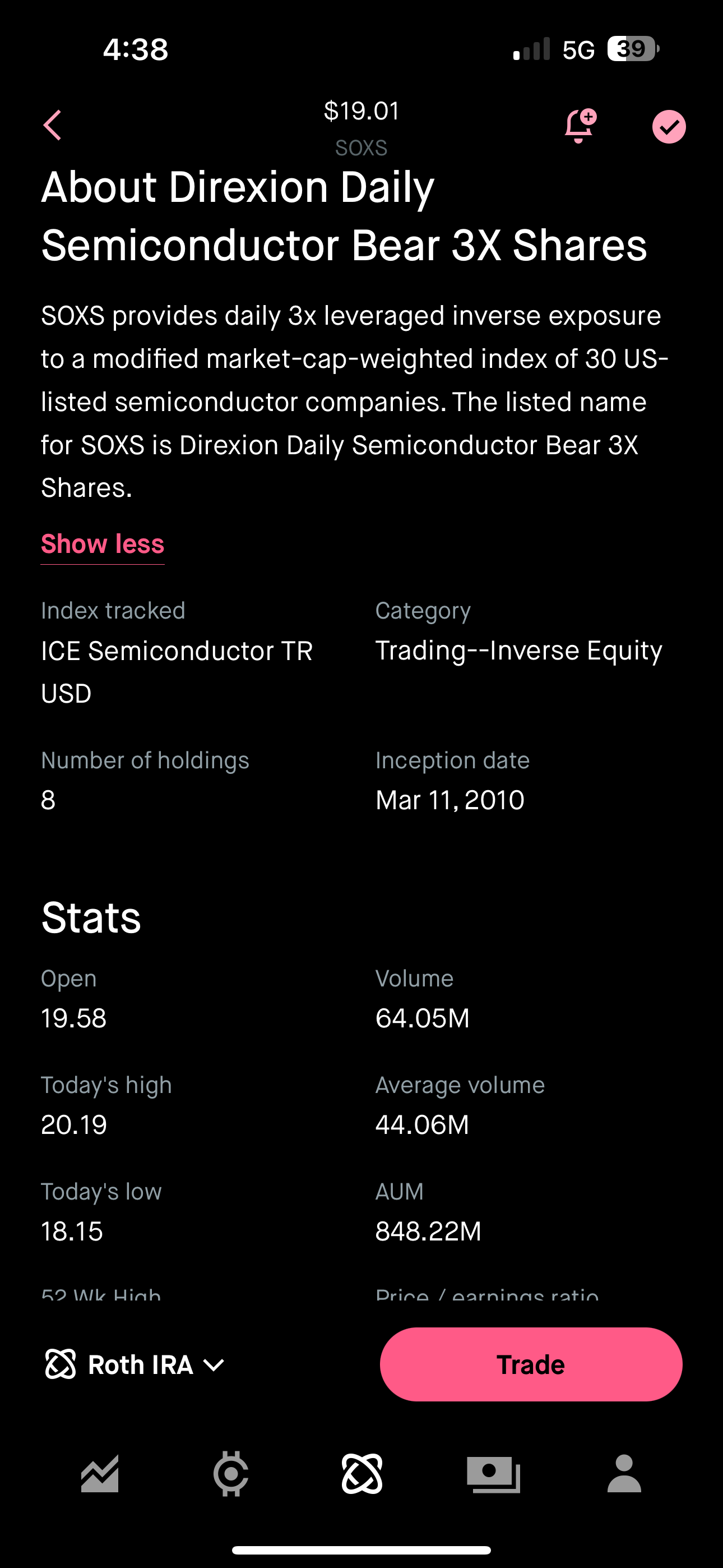

Ohhh okay I got you. I have a Fidelity account as well. They have all the mutual funds and MMFs so you won’t lack for choices. You may want to look into something like SOXS. It is a direct hedge for semis.

(There are others out there that are not 3x leveraged if that’s not your cup of tea, way too many to list here.)

Protective puts are also a nice option (heh), and I was surprised to learn recently that there’s actual viable open interest on VOO options. Nowhere near as much as SPY but enough to make it viable. Just look for “cheap” (ie 20 delta or less) leaps puts so that you will still get a return if your VOO takes a shit.

But hell man, if you’re on Fidelity you can just sell it all and keep your cash in your core position (SPAXX) for nearly risk-free, though it has a .42% ratio.

The just sell before a downturn and buy back in later advice, nothing ever goes wrong there.

8% of the time it works every time.

Are you internationally diversified?