The guy probably stays margined to the max and whenever his positions take a hit, he gets hit with a Reg T call letting him know he is essentially margined past his allowance and the broker reminds him again that he needs to cut that shit out.

The dude probably gets this message every other day and is just flaunting his degeneracy or maybe a hope that someone will give him some money.

Obviously the share price is up more than 15% today. I shorted a little more, so that I now have a weighted average basis of $77.71 (vs. current share price of $88).

A couple of things stand out in terms of my negative view:

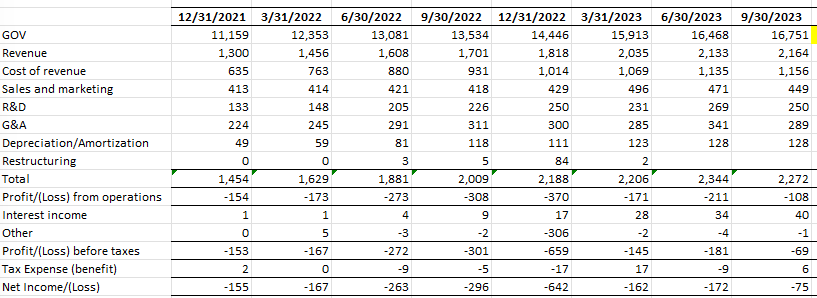

If you look at operating profit (loss) over time, it just isn’t showing much evidence that there are huge benefits to scale in this operation:

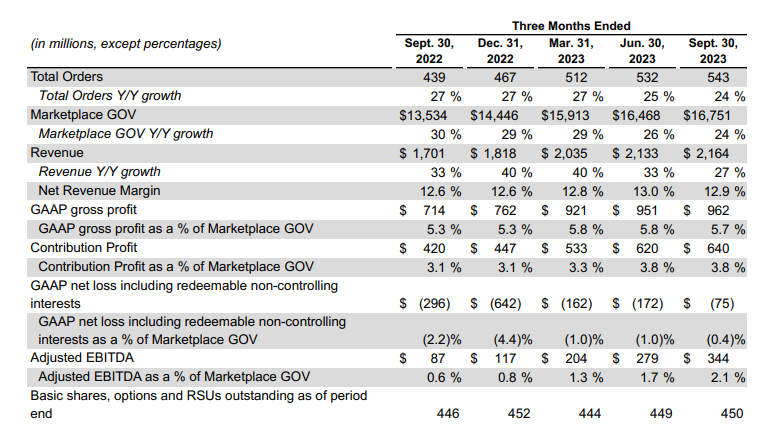

Cost of revenue isn’t really budging, so I think gross profit probably has a ceiling of less than 50% of revenue. Their remaining expenses are declining a bit, but I can’t imagine pre-tax margins are ever going to be higher than 10%, and even that seems crazily optimistic. It would mean increasing gross profit margins from their current levels and decreasing ever other expense by 2/3rds (as a % of revenue).

They’re spending a ton of money on share buybacks to offset the very large issuance of stock-based compensation. Right now, that dilutive effect is somewhat hidden, as the reported EPS number on the Income Statement is based on the pre-dilution shares O/S number. If/when the company reports a positive GAAP profit, those dilutive securities will increase the share count pretty sigificantly. (Current quarter shares outstanding used in EPS calculation is 393 million, but a fully diluted share count would include another 51 million or so shares related to options and unvested restricted stock and RSUs).

Current market cap is roughly $35 billion. I think it’s reasonable to say that a $35 billion company should be earning about $1 billion in pre-tax operating income within the next 5 years. It’s incredibly hard to see how they get there. If you assume 30% revenue growth compounded over the next 5 years (much higher than this year’s) it takes a ~3.5% operating margin to get there, which would be an absolutely incredible change from their current conditions.

But the proof of the valuation is in the results. Continued LOL for me at thinking I can value this or any other company.

I simply can’t believe that DoorDash’s model is sustainable.

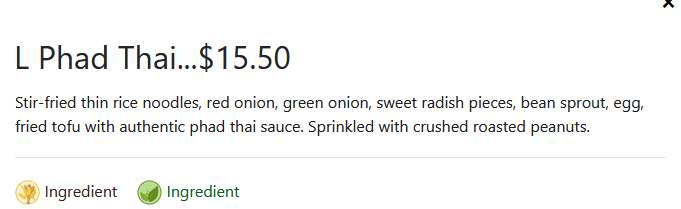

Here, in this helpful thread that X just suggested for me, someone has the ability to pay $36 for an order of Phad Thai that sells for $15.50 at the restaurant you’re ordering from.

Notice that DoorDash’s base price for this item is not the $15.50 restaurant price, but instead $25. Just a complete scam. AND YET DOORDASH STILL CAN’T MAKE MONEY.

I have a credit card that gives me at least 15 bucks on Uber every month plus I get supposedly 40% off coupon for Uber Eats almost every week. During the COVID days when I was not using cars I tried as much as I could to find a way to use these and simply failed. A couple of times I got a bottle of Pho from a place a few blocks away and even with 30 bucks of supposed discounts it cost more then just picking it up myself. Also the itemized bill is more complicated then a hospital stay (and they dock your card 2-3 times per meal for some reason). Nonetheless the sidewalks are absolutely lousy with these delivery guys, I just can’t comprehend it.

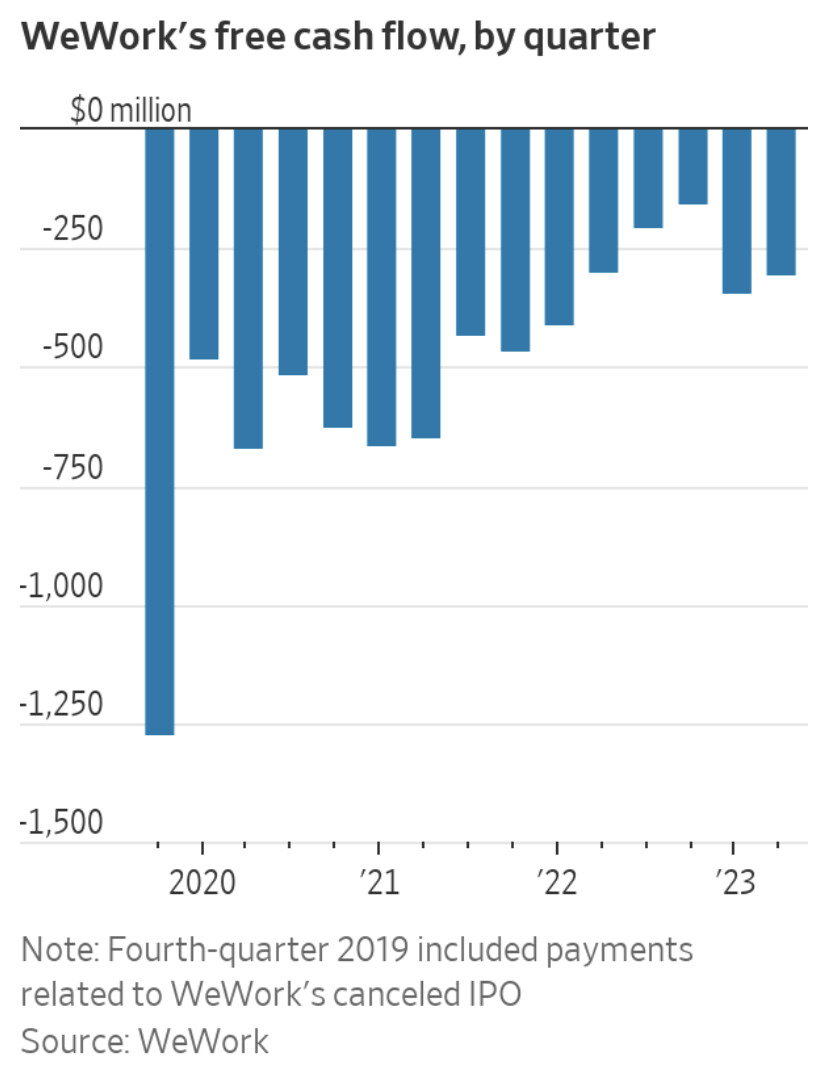

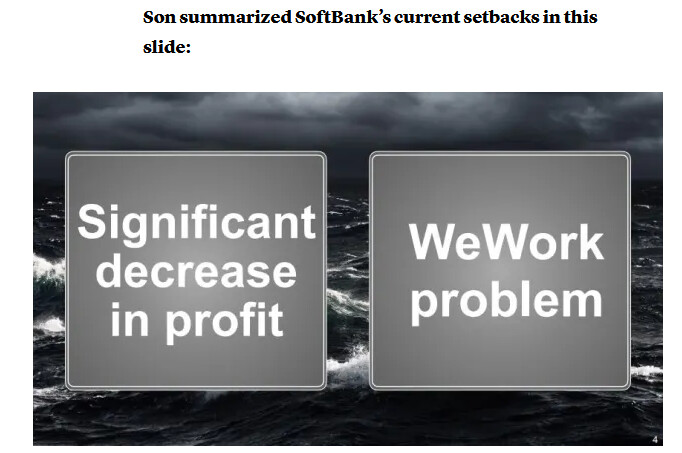

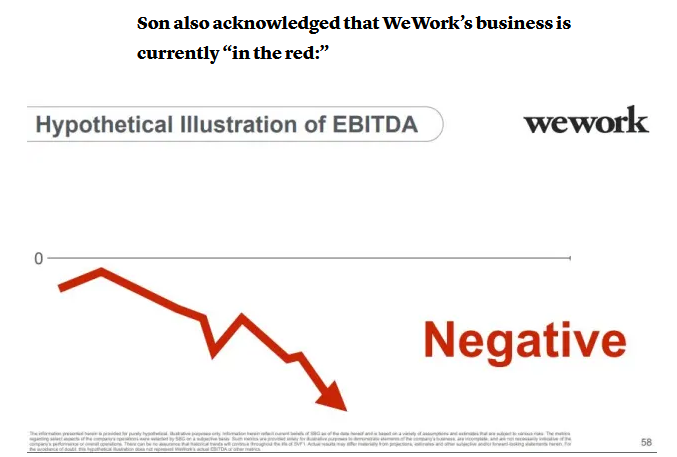

Fact check: Correct! WeWork did have a significant decrease in profit.

Fact check: Correct! (But kind of redundant with the first point. Also, not sure why this is hypothetical.)

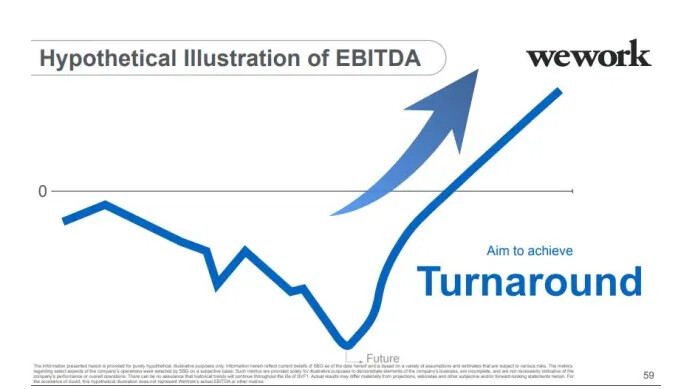

Fact check: Correct? In the sense that if they did achieve a turnaround, EBITDA would increase.

But obviously you cannot just snap your fingers and wish this turnaround into existence. Fortunately, Son provided a very clear 3-step plan that IMPORTANTLY did not skip the second step, as a typical underpants gnome strategy would:

Stunning that this level of strategic brilliance resulted in bankruptcy.

You know how this person knows that the pad thai cost 30 bucks to show up at their house while they were in their pjs playing video games? Because they bought it, and they’ll keep doing it.

Not to say DoorDash is going to be a trillion dollar company or anything, but yeah affluent people will pay a fuckload of money not to have to put pants on to go out to dinner.

I assume (and hope) doordash dies but I’m concerned about what they leave in their wake. Like all these wannabe monopolies that have subsidized their market share growth through investor losses, I assume DD has killed off a significant amount of the delivery market (and probably some restaurants too)

Speaking anecdotally, our doordashing has gone way down since the pandemic “ended” and their prices now seem insane to me. It’s only a matter of time before they price out even well-off people.

I think trying to value Doordash by looking at the sustainablity of its current model could certainly give it a gloomy outlook. But they building services for grocery stores and similar stores, they aquired Wolt, their European business is growing and theyve ankle busted a lot of their competiiton. They most certainly won’t resemble anything similar in the future if they’re still around.

Since I’ve bought an electric car (and my wife gets free charging at work), I sometimes deliver for Uber Eats.

I think the 2 craziest orders I got were 2 large cokes from Sonic, that’s it, delivered about half a mile away. I expected it to be to a shitty house with no cars but it was a nice home with 2 cars in the driveway. Maybe they were too stoned to leave the house.

The other one was a Starbucks Frappuccino delivered about 5 miles out that ended up costing like $17 with tip.

Doesn’t seem sustainable to me, but I know my wife and I paid like $40 for $12 worth of taco bell when neither of us was in any shape to drive. I think uber/door dash will grow as more states legalize weed.