I think it really depends on the medical building. If it’s a private office, I can see where you are coming from. On the flip side, I’m having a hard time picturing a VA hospital trying to scam a patient.

Yeah this. Everything feels completely predatory in the U.S.

In Costa Rica when you get surgery, they take the full amount + 20% extra up front, in case of complications. Almost always they give you that money back at the end!

Imagine a U.S. hospital having cash in hand and not finding an excuse to charge you for it.

2 Likes

You don’t have to be there for 30 minutes. I’m to lazy too look it up now, but the way the rule is written is that the doc can bill for a level 4 if one of the two conditions are met

- He spends 30-39 min on your visit that day (that includes any time spent after you left filling out medical records or whatnot or before you came in reading your old records or anything else)

OR

- He meets other criteria based on the problem(s) you had and what he did. If he meets those criteria, it doesn’t matter if he did it in 2 minutes, it would still count. If you’re interested in exactly what those are you could look them up, but it is likely stuff that could be done in less than 30 min. That is almost certainly not what the rules intended, but that’s the way it is.

For sure. Not all mechanics are scammers, after all. But you should assume they are until proven otherwise.

I don’t think “rigged” is the right word. One of the reasons it’s competitive is that there aren’t many spots and as a result there aren’t many dermatologists. It seems far fetched for a small minority specialty to “rig” anything. The rules could be easier to exploit by dermatologists, but I highly doubt it is due to their intentional rigging efforts.

Agreed.

When you first said rigged, I just took it literally. What you wrote above seems correct to me.

Just talked to the insurance company. They don’t know anything about Level IV vs. whatever, just that they seem to have negotiated that $609 (after adjustment) is ok for an office visit with this doctor. I told them I think they’re getting ripped off (since I’ll probably just meet my deductible anyway then who cares). She agreed.

Good to know the insurance companies are in there fighting to keep prices down!

I’m still never going back to that dude. I’ll find some mom & pop clinic and get a price up front. Don’t care if it’s out of network.

Oh they definitely, know. Maybe the person who you talked to on the phone didn’t know, but I wouldn’t expect that.

I’m just amazed that whoever negotiated that doc’s contracts got 4x medicare. Considering how impossible negotiating with insurance companies is in general, that’s a pretty impressive accomplishment.

As an aside, this is exactly why when you get a bill, for each service the list price is some ridiculously high, absurd number. They normally expect to get it adjusted down, but every once in a while, someone will actually pay it. It’s a free roll for the doctor/hospital. The only people that get screwed are the uninsured.

I bought a new bluetooth insulin pen. The agent on the phone checked my insurance and told me it would cost $30 for a year. I didn’t really need it, but thought for that cheap if it was even 5% better it would be worth it.

A month later I get a bill for $1000. Well 1000 - 30 because they took what they said would be the total as a deposit.

1 Like

Good luck finding a “Mom and Pop” dermatologist in LA!

Maybe see a dermatologist when you go back to KC. That might be a more effective solution.

How it is in the Czech Republic:

I got some probably benign thing on my back that I need to see a dermatologist for. Basically, it works like this:

- Schedule appointment with GP (wait 1 week)

- Get reference to visit dermatologist from her after basic checkup

- Sit in some hospital clinic for 8 hours waiting to get seen only to be told that I’m right and it’s just a cyst

But hey, I don’t pay for it like you guys do.

Now you might think, “Just schedule with a derma directly.” but then that’s a 6 week wait for my appointment unless I want to pay out of pocket instead of using insurance. Getting a reference from your GP allows you to kind of skip ahead a bit.

1 Like

I have Kaiser HMO, and this spring I had a cyst removed from my back, which took a physician and a tech close to a half hour to remove via burning.

My total bill was <$700.

My understanding is now if your medical debt is paid, it will no longer count against your credit score.

So when it went to collections it would but then if you made a deal to pay it off it would no longer count.

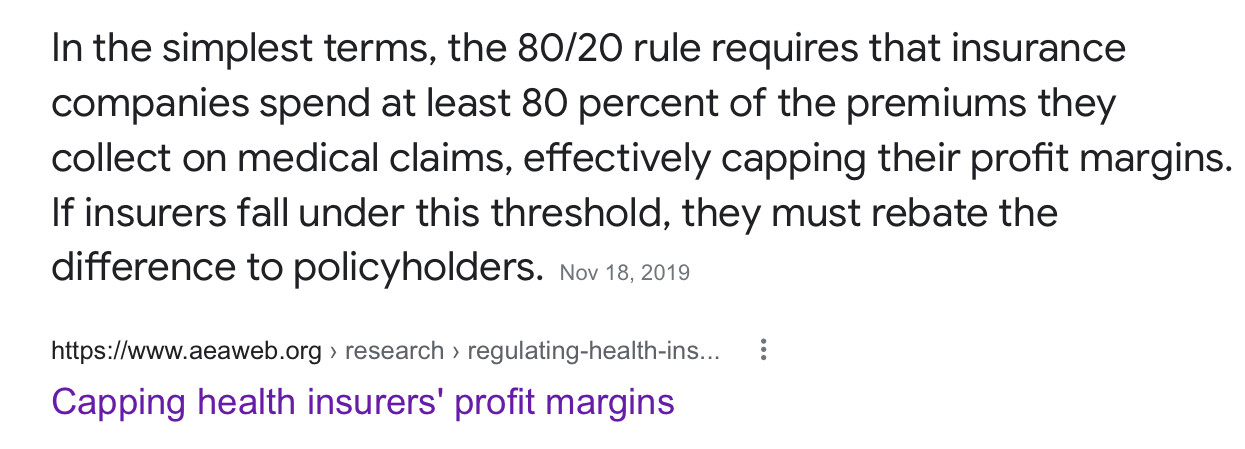

Insurance companies don’t care about being ripped off as their profits are capped based on the amount of care they pay for.

I used to go to one for plantar’s warts. Maybe she’s still around. Poor people with no insurance gotta go to the doctor too.

True, but generally they go to the county hospital system or something like that.

You might need to show your work here. Why do they fight paying for all sorts of necessary care if they don’t GAF about how much they pay out?

I think I have this on the inside of my knee cap. It feels like I have a scraped knee, but there’s nothing there. I can’t do certain stretches that push that part of my knee against the gym mat. It’s mild, but it’s not going away. There’s no rash or redness, maybe a tiny bit of swelling.

I also have an ankle that always itches - since last summer when I camped out in a tick habitat, then got bit by some kind of mite (I think) on the ankle on my parents’ deck. I never found any ticks on me on the campout. But I’m pretty sure I started itching immediately when we ate dinner on my parents’ deck. I think it might be an oak mite - whatever it was it was too small to see.

I’ve had a round of antibiotics since then, not for lyme disease but for an ear infection.

I wonder if I should get this checked out.

I’m doing further reading and no other articles tie Allodynia to lyme disease. So I dunno.

If you think you could have Lyme Disease you should get it checked out IMMEDIATELY.

1 Like