I suppose you want to live in some SOCIALIST hellscape where you’re FORCED to get health care? Sad.

1 Like

1 Like

Another on the list of Elon Musk’s accomplishments!

i do thjnk you mean george santos

I have read Lilly’s move may just be temporary while they hope the Medicare cap is removed and competitors can’t ramp up production.

If things go as they hope they will be able to raise the price back in the future.

I hope places like costplus can get their own supply going.

If by simmering they mean “complete disaster for as long as anyone can remember” then it’s definitely simmering.

1 Like

From the thread

https://twitter.com/OrthoYour/status/1630655316734910465?t=mJf4_KHtWOx_JYWjcDFa2Q&s=19

I’m not an expert in doctoring or anything, but something seems off to me

1 Like

Just a little bit.

Prior authorization stuff seems like it’s due for some major regulation

I had a new kind of mole I was a bit worried about so I went to the dermatologist. Talked to him for 10 minutes, he burned one thing off my face, told me the mole I was worried about was fine.

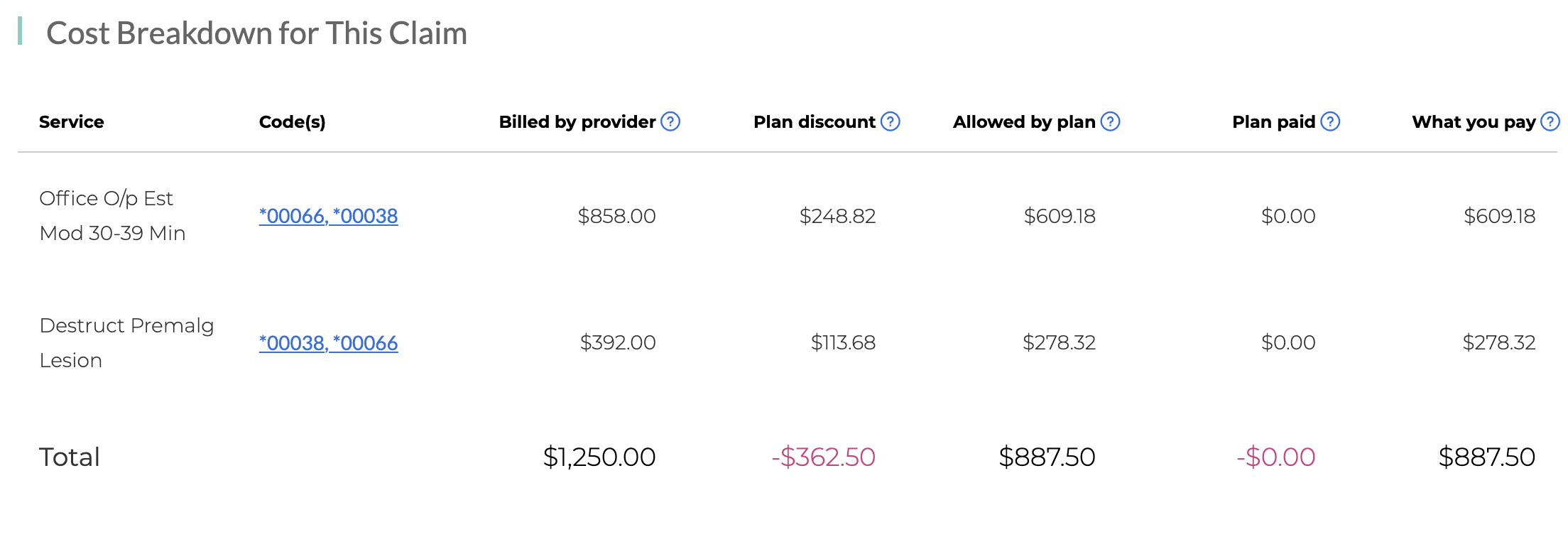

$887.50 - and that’s after the insurance adjustment.

Before adjustment: $858 for the visit, $392 for 30 seconds of burning the ting off my face.

That’s insane. That’s basically “never bother us again unless you have a serious skin problem” pricing. So much for preventative care.

This place charges $125 for a standard visit: How Much Does A Dermatologist Cost? - Galt Dermatology

Mine says Office Visit Lvl IV. Anyone know what that means?

When physicians report a level 4 evaluation and management (E/M) code, they’re telling payers they should be paid more because their patient requires medical management for an exacerbation of an existing chronic condition, a complication, or a new problem, says Raemarie Jimenez, CPC, vice president of membership and certification solutions at AAPC in Salt Lake City, Utah. Payers may deny level 4 E/M codes for patients who respond well to treatment and are generally well-managed, she adds.

10 minutes of chatter about rosacea and a mole. He did give me a prescription for a different kind of cream, even though we both thought the one I was using was ok. I guess that mushrooms the 10 minutes.

1 Like

There are 5 levels, if I remember correctly. So he billed you for the second most complicated one possible. However, there are rules that determine which of those level that should be used. And it is possible to follow those rules and still end up with a situation like your where something seemingly uncomplicated can justify a higher rate of billing.

Out of curiosity, does your EOB list what cpt codes were billed. Based on your description and some google, I’m guessing 99204 and 17000. Was it something else? Were there other ones listed?

17000 for the burning.

99214 for the Level IV office visit.

I just talked to them. Apparently they billed the same code in August '21. But my deductible was met by then so of course I didn’t notice it or care. This time it’s all coming out of pocket and I don’t have plans to meet my deductible this year.

I wonder if I can get anywhere with the insurance company? It seems really bogus to be billing $858 for 10 minutes of mostly idle chit chat. I wonder if this is why he wanted to switch prescriptions? So he can claim I had a chronic problem that wasn’t responding to treatment.

I swear I’d feel more comfortable dealing with a Moroccan rug salesman than the U.S. medical industry. Next time I’ll shop around and get a quote up front.

Hmm ya, this reminded me that my cardiac catheterization was pre-authorized and completed on Wednesday, but I have yet to receive any notifications about my surgery that is now scheduled for March 31. I’m not really worried but it is one of those things in the back of my head…

It’s very unlikely the doc does his own billing

Trying the insurance company now. Got some sweet Chuck Mangione hold music.

Everything I can find online is about disputing your insurance company for denying a claim. I can’t find anything about disputing the billing code itself.

I think I’m going to let this go to collections and see if I can pay 1/3 or something eventually. Does unpaid medical debt fuck with your real credit? Even if it does I don’t have any plans to buy anything on credit for a long time.

https://www.reddit.com/r/nova/comments/ydmxrn/dermatologist_in_fairfax_sent_me_a_massive_bill/

Looks like a similar story.

You have 1 year after it goes to collections to negotiate before it appears on your credit.

It generally takes 4 months to send it there. Haggle it down. That’s 16 months total if they’re stubborn about it.

If you can’t trust reddit user Sawstik496, who can you trust?

1 Like

Yeah this seems like a pretty terrible negotiated rate - about 30% off both things.

Just remember that any time you enter a medical building everyone is trying to scam you. Yes, they generally also want to help you, but they want to help while taking as much money from you as possible. You are at the mechanic’s shop and should act accordingly.

2 Likes

Something seems weird. You can look up what Medicare would pay him for all of that (about $220, assuming it took place in LA or close). So either this guy has managed to negotiate the insurance company into paying 4x Medicare, which I assume is high, but it is impossible to know because these things are so regional and specialty dependent. Or there is some other explanation.

When he billed for those two things last year, did the insurance pay him ~$900? If that’s the case, the insurance company seems like they are getting ripped off (again, caveat above applies) and maybe they need to negotiate their contracts better.

Yeah I asked her what the adjustment was in 2021 and it was similar.

No way I was in there 30 minutes unless you count the time waiting and getting my blood pressure taken or whatever the assistant did.

The good news is I’m only $284 away from meeting my in-network deductible after this. So I’ll probably hit it now, and then I won’t give a crap where the money I had to pay came from.