No not reporting it as rental.

My buddy’s house has gone up from $700k to $1.2M. So maybe that’s what he was thinking about. My gain will be under $250k.

No not reporting it as rental.

My buddy’s house has gone up from $700k to $1.2M. So maybe that’s what he was thinking about. My gain will be under $250k.

You may owe state tax in lol Cali not GOAT, no idea. But I’m pretty sure you will owe zero federal tax.

Are you sure it’s 437 and not 457?

Non-governmental 457s are OK, but not as good as the governmental variety which are functionally just another 401k. As I’m sure you are aware, the money is at risk if the employer goes belly up. Also if you leave, you’re forced to take the money out over a pretty short period (since you can almost never convert it to any other kind of retirement account), which can be problematic.

Of course, as a practical matter, the employers that offer these tend to be at pretty low risk for going bankrupt, so you’re probably fine on that front. In your spot I’d probably max out both of the retirement accounts first and then shove the rest in a taxable account. And that sounds like what you’re doing.

If you can’t max it out then I agree that there is no reason to have a taxable account.

Assuming you’re unmarried and living there, then I think above is correct.

It goes up to 500K if you get married. And you only have to be living there 2 out of the last 5 yrs. So you could be renting it out for 3 out of 5 years and still have it qualify as a primary residence.

This is good, but depending on your health care situation, if you can deal with a high deductible health care plan with a health savings account, then the HSA is the first and best savings vehicle to fund. They can be tax free going in and out, and you can hold stonks in them (but having cash in them is obviously a good idea too).

I don’t think so, because as someone explained above you can just convert your retirement accounts to Roths later (and at presumably a lower tax rate than where you are at now).

Well you won’t make it at max efficiency. But you will still make the conversion at a better rate than if you do it now.

If you put it in taxable now, it will have been taxed at your marginal rate, and it does not grow tax free. If you convert later, it will be taxed at lower rates and it will have grown tax free. So you’re still going to get taxed, but the tax should be less if you just wait until later to do the conversion.

I guess your point about future tax rates is true. You really can’t predict that, and I guess it’s possible that the rate at which you convert could be higher than your current marginal rate, but I’m assuming you are in a pretty high bracket now, so I think that scenario is unlikely.

Well if your buddy is married, he really shouldn’t pay any taxes on that. Also he can reduce his tax burden by deducting things like transaction costs and any money he put into renovations.

Just throw some rocket emojis in them and you’re good

This is a great write-up of Bruce Berkowitz, one-time manager of the decade and now huge underperformer:

https://canuck-analyst.blogspot.com/2021/02/bruce-berkowitz-from-morningstar.html

Takes special target at Berkowitz’s investment in Sears, with the idea that Eddie Lampert was going to generate enormous wealth:

2006 mid-year Letter: Sears Holdings, which is 4.53% of the Fund’s net assets, has also become significant because of Eddie Lampert, an unusual investment talent with a fabulous paper trail. While Fairholme is agnostic about the future of Sears’ retailing success, we believe Lampert will continue to redeploy the company’s extensive assets to our benefit.

Anyway, I don’t know who the author is, but it’s worth a read.

If you have lived there for two of the last five years (not continuously) and the gain is lower than 250,000 you pay -0- in tax.

Anyone have any idea what my buddy was thinking about with this once-in-a-lifetime get out of tax free card or whatever?

I think a long time ago (20+ yrs), it used to be a one time thing (i.e., shield some cap gains from taxes when selling primary residence). Now you can do it every two years.

Not mentioned yet: you’re also paying state taxes whenever you decide to take the tax hit, so if you’re in a high tax state now and there’s any chance you’ll retire in a state that doesn’t tax IRA distributions, lean towards pre-tax accounts. As others have mentioned it’s nice to have some of each when you retire, but if you didn’t start funding a Roth from your summer college jobs it’s not worth it now if your state + federal marginal rate is 30-40%. Watch for opportunities to pile into a Roth if your tax bracket temporarily drops in any future years though, either with new money or rollovers.

Bolded is true in a lot of cases, but not true if you can only do the Roth through the backdoor. If that’s the case, then the Roth is just a freeroll.

Futures up bigly!

Maybe, depends on when you might retire. If you retire when you’re 55, you can make penalty free withdrawals from your 401k. But if you do that it would interfere with the rollover scheme I described above, since all 401k distributions, the ones you’re living on and the one for the Roth conversion, would be taxed as income. But that still might not be a reason to do the Roth now, because you’d essentially be paying taxes now to fund a Roth so that you can put more money in a Roth later. If you aren’t going to have taxable accounts to live off in early retirement I think it becomes purely a question of what is my marginal tax rate now and what is my marginal tax rate going to be when I retire. And hedging and putting some in a Roth is fine.

edit: also, I’m not sure what the rule is for early withdrawal of Roth 401k? Is it like a Roth IRA that you can withdraw the contributions penalty free at any time? I don’t think so, I think it has the same withdrawal rules as the regular 401k (and the other 401k like instruments). A quick googling indicates that’s the case. If so, then it’s purely a tax rate now vs tax rate in retirement question. But you can actually do a Roth or backdoor Roth now, and if you want that flexibility of getting the contributions penalty free in early retirement, you should.

Also, the closer I look, Berkshire is almost certainly massively undervalued.

They have $280 billion of stocks and like $140 billion of cash, adding up to $420 billion. The market cap is $500 billion.

Meaning the market says all of their operating businesses are worth only $80 billion? That’s insane.

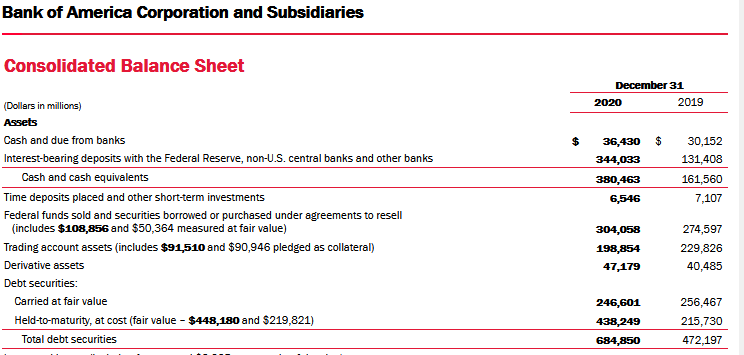

You should see Bank of America - it has a market cap of $300 billion, but has more than $1 trillion in just cash and debt securities!

[This is a snarky way of pointing out that you can’t just total the assets for a financial/insurance firm without considering the massive liabilities those assets are associated with.]

Still agree with the point that Berkshire is undervalued. If for no other reason than Buffett has been buying back shares pretty aggressively.