I don’t know, man. I think it’s not too hard to imagine that a [checks notes] Mexican poultry producer might be exposed to a lot of business risk. And the fact that their most recent quarter’s gross margin was roughly half of what it was a year ago suggests that maybe they are facing some challenges?

I mean, I don’t want to dissuade you from investing in what you think is best. And I don’t pretend to know anything about this company or what an appropriate value would be. But you seem incredibly fixated on cash holdings and P/E ratios, and I really don’t think those are as informative as you seem to think they are.

Dude is an insanely aggressive self promoter whose hedge fund performance sucked and maxed out at $180 million assets under management.

I believe I met him at a Berkshire Hathaway annual meeting, where he was interested in talking with me until he discovered I was a grad student, rather than a young trust fund kid.

My amateur way (which I have long since abandoned) was fucking great.

–Costco is such a great store. I think I should buy some of their stonk.

–I don’t know what I would do without Google or Gmail. I should buy some of their stonk.

–Holy shit, Amazon can send me anything I could possibly want in two days! I’m gonna need some of that stonk.

All of my losers (and shots I didn’t take) were a result of trying to do any more analysis than this.

I think the true sign of being a Warren Buffet is spite buying an entire company because the previous owner tried to buy your stock back from you for slightly less than you had verbally agreed to sell it for.

Inflation in the cost of feed and supplies, which they should be able to pass on if/when it persists since they’re basically selling staple products.

Yeah I mean I look at earnings history, too. I’m looking for either stability at a low p/e, growth at a reasonably but less low p/e, or deterioration with a good explanation that shouldn’t persist. But I do place more importance on tangible book value (so heavily influenced by cash) and low multiples, because I view both as a very strong margin of safety, especially if the company pays a dividend.

The main problem with IBA is that they pay out a low percentage of profits in a dividend and don’t seem interested in buying back shares. So they’re sitting on a pile of cash, and the market doesn’t like it. They want to expand into other meats, and they want to buy underpriced companies that would become more efficient as part of IBA.

My thinking is that they’re in a better position to weather inflation than their competitors, which could lead to profitable acquisitions. Or, if the market crashes, likewise. The worst case scenario seems to be that they continue to sit on the cash, payout small dividends, and trade around a similar level.

I also think we’re going to see continuing cycles of rotation from growth into value, and they should benefit from that too.

Yes, either of future earnings or current balance sheet. I mean one of the keys here is these are mostly not large cap companies. Like IBA is a $2B company, but 75% of it is owned by the founding family. So only ~$500M trades publicly. I believe only around 1/4 of that is on the NYSE, the rest is on the Mexican exchange.

So a hedge fund can’t really do much with it. APT has a market cap of $60M, same thing. So now I’m competing against a much different playing field.

The primary benefit of diversification is that it reduces uncompensated risk (i.e. the idiosyncratic risk of a particular company or industry).

Most stocks just don’t do very well. The expected return distribution of any individual stock is very skewed. Owning a diversified portfolio lets the central limit theorem work in your favor.

At least 99% of arguments for picking individual stocks are just a version of Tobias Funke “maybe it’ll work us” memes in a different form. I mean if you find it fun and interesting then by all means do it with a small part of your portfolio. I bet on hockey games, man, I get it. But I don’t bet my retirement on hockey games.

I don’t think it’s a systematic mispricing, out of like 5,500 stocks available, there may be 10-15 of them. It’s an exception, not a rule.

I do think it can exist outside of micro/small caps, although there probably has to be a specific set of circumstances leading to it. I think the broad markets are currently overpriced, and I think there are plenty of vastly overpriced mid and large cap stocks. I think there are way fewer underpriced value stocks that are mid or large caps relative to the total number of mid/large caps, although there may be a few.

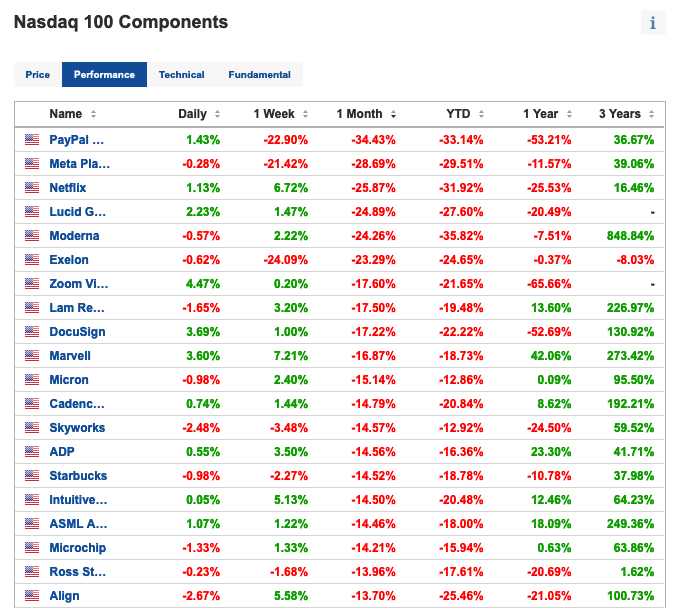

I checked the NASDAQ 100 yesterday and found one that qualifies and one that’s close. The theory was that with the tech growth stocks taking it in the teeth lately, people may be panicking and selling the QQQ or NASDAQ 100 etfs, and stuff that was borderline to qualifying as a Graham value stock could get dragged down a couple percent due to the index selloff.

One fit, but I decided to keep it back for the future as long as I could get to the allocation I wanted with other value stocks, thinking I might get an even better deal in the future… So I haven’t done the research yet to see if there are mitigating factors that make me want to stay away.

Generally I think the mistakes in large caps and the broader markets are going to tend to be made on the overpriced side, with the exception of panic selloffs during a crash. Like, tons of money poured into stocks the last several years because interest rates were low and, in theory, an overpriced stock beats a shitty bond yield. “There’s nowhere else to put the money,” people keep saying.

That was true to an extent, but not being invested was an option, buying hard assets was an option, and buying emerging markets was an option. Just because stocks at a high multiple are a better deal than bonds with a shitty yield doesn’t mean that it’s a profitable investment.

If there are some straightforward finance screens plus some follow up reading that can be used to identify stocks that have expected risk-adjusted returns in excess of the market, I would consider that to be a systematic mispricing of a particular type of company.

We’re not talking anomalies here. You’re saying that companies with certain finance ratios plus some other qualitative characteristics are self-evidently mispriced.