I’d say Cathie Wood (ARKK) is going to be a bank manager in a few years right but then I realize she probably got stupid rich anyway

fine maybe one of those holdings hits but that’s a lot of crap and why it’s majorly down

I’d say Cathie Wood (ARKK) is going to be a bank manager in a few years right but then I realize she probably got stupid rich anyway

fine maybe one of those holdings hits but that’s a lot of crap and why it’s majorly down

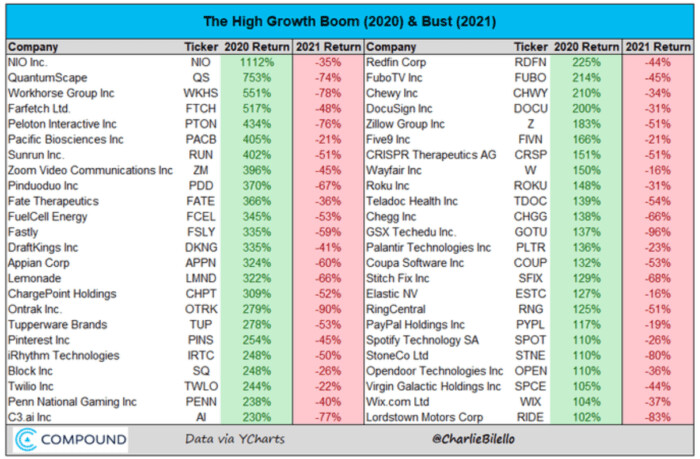

Tupperware up 278% last year, what the heck yeah that couldn’t have been the time to buy the market. don’t care what any of you say now.

Have or had three on this list last year, Draftkings and fubo both of which I dumped (phew) for different reasons, I actually am okay with draftkings but I don’t think people will have as much money to blow on sports this year, and fubo was just me being an idiot buying it I think (think I ate a loss on it instead of that nice green number), it happens and Paypal, which if I knew got to 300 I would’ve dumped all of it. sigh, should’ve dumped some when I last looked at it, it’s hard to get the bull case for it now when I only use it when it’s the only thing left that works.

Roku gotta be a terrible buy right now, nobody under the age of what 50 would ever buy one for any reason? but it’s still priced like mega growth stonk

Could you post a list of the funds you have available to buy?

Man, housing is just a hilarious bubble in FL right now. Eventually, it will start slowing down and then everyone will want to sell at the same time because they think it is the top.

Lol yessss I remember that thread and I love it, because their commercials are ridiculous.

I have my old, very shitty, very cheap exercise bike that I never used because it’s very shitty and very cheap just sitting in the basement, which has a walkout sliding glass door and faces the woods/creek. There’s nothing else in the basement, it’s just wasted space, so I just put it in front of the door facing the view as kind of an inside joke at Peloton commercials that only I get to enjoy.

I’ll probably hold on to NVDA stubbornly to the end even tho I probably shouldn’t

great the chart looks like the classic went up a lot then bull trap then goes down too.

pretty sure I’m just gonna dump 100% into brk.b and call it a day.

This isn’t a shot at you specifically, because this is how probably the majority of people think about stocks, but valuations aren’t supposed to be based on one year. Like almost through a sort of pact that a huge chunk of the market is going to be that way, prices get driven up like crazy over short-term profit windfalls that everyone knows are going to be short-term and thus shouldn’t matter that much.

I have MRNA and BNTX. MRNA I got in for like $69 or something, so I’ve lost back a ton of profits but I’m still way up. BNTX I got in more recently and am down around 50%.

I think Wall Street is out of its fucking mind on these being as low as they are. They think that the pandemic is over, vaccines are over, boosters are over, and COVID is done.

As a result, MRNA is trading at a P/E of 9.88 and BNTX is at 4.45.

Like, MRNA is making 3-4 billion doses this year. If they don’t sell the majority of them, they’re just massively incompetent, right? They have gotten $26 a dose so far and their profit margin is like 84%. Even if they only get $18 a dose because they’re selling to more countries that can’t afford higher prices, and thus only make a profit of $14 per dose, and even if they only sell 2 billion of them, that’s $28 billion in profits, plus they have like $9 billion in cash on hand through Sept 2021. Plus whatever they made in Q4.

Basically at the end of 2022, it sure seems to me like MRNA will almost certainly be sitting on approximately $40 billion in profits, and that’s if they only sell 50% to 66% of their inventory. If they actually scaled well and sell it all, they’ll have that much more cash on hand. The current market cap is $65 billion. I expect us to need annual boosters for at least a few more years, and even if uptake isn’t super high, they should be able to sell 100M-150M doses a year at $26 with an 84% margin IMO. In 2023, they expect to have their combination flu/covid/rsv vaccine on the market, and that’s going to drive the price they can sell it at quite a bit higher.

I think they should be worth something like $40B to $80B just off very conservative estimates of the long-term flu/covid /rsvvaccine sales looking forward, plus the $40B they’re going to have on hand, plus the value of their other potential vaccines and therapeutics. Their market cap pre-covid was $8B, so go with that although it’s probably higher now as they have had positive developments and can leverage their cash flow now to move faster on R&D.

So $40B to $80B plus $40B plus $8B = $88B to $128B. Currently trading at $65B.

Oh and that’s if we don’t have to do widespread boosters again, or the uptake on them isn’t good. If the healthy 20 to 65 year olds who currently think this is over decide they should get a booster, then it’s worth that much more.

And BNTX is an even better deal!

I know nothing about biotech except there’s one thing

like in crypto, fundamentals don’t mean much, it can still drop a shit ton from here.

also regarding DKNG is in a recession you don’t wanna own that one that’s for sure. It gets rekt rekt instead of everyone else’s rekt.

DraftKings is less dumb now. Valuation at peak were just stupid if you worked through the underlying assumptions needed to support the valuation. DKNG and PTON stock price some good ghosts of Christmas future for a number of these sun running tech/growth stocks though. I dont think either will ever reach their prior tops as independent companies.

I would imagine that’s true before a company becomes profitable. Like when it’s all based on speculation about their research and potential products, there’s not enough publicly available information to make a good estimate on the valuation. You need to know their odds of success, their likely market penetration, and their likely pricing… None of which is public information.

Once a company is profitable, you can at least value the profit-generating portion of the business based on fundamentals. There’s some level of guessing on the rest though, which is why I just used their per-share price pre-COVID for that side of the company. Personally I think the market probably undervalued it substantially pre-covid, and that their cancer research and other mRNA research is worth more than $20 a share, but I try to lowball my estimates for safety.

That’s a fair point.

Right but they still aren’t profitable yet. They’ve lost something like $1.85 billion in the last 12 months they’ve reported. So the question is how they plan to turn that around. It’s pretty astounding to be losing that much money as a company that should have little to no overhead. I assume marketing and lobbying are their biggest expenses.

Their fantasy sports business should be pretty mature by now, the question is how much they can expand their sports betting offerings, right? And they’re going to catch competition in every state that legalizes it from MGM and Caesars at a minimum…

Oh I wouldnt rush out to buy the stock, just dont think its an impossible valuation like it was six months ago or w/e peak was.

But yeah, the main issue right now is that sports gaming is a huge land grab so marketing costs are out of control (although profitability also was sort of shockingly bad ex marketing last time I dug into this) Also not sure some of these states have agreements with the companies that are sustainable long-term.

DFS business is immaterial to DraftKings stock price. Their stock presentations have it as a rounding error in the value of the company. DFS basically still exists as a marketing tool to acquire customers for potential sports bettors. I doubt DFS as we know it today is around it its current form in 5-10 years, its really not a very good business and will cease to be useful as the sports betting business matures. End game is probably DK gets acquired by a larger company and DFS is phased out.

I think part of the problem is probably that historically revenue is going to be capped at around 5% of the total amount wagered, assuming you’re just trying to split the action on both sides and take the vig. Sometimes they may have sucker lines and such and maybe they can get 8-10% of the total amount wagered, but that’s probably it for their gross revenue. They can also get some small amount of interest on the balances they’re holding.

Then you’ve got to subtract the overhead for the apps and customer service, financial transaction fees, and their marketing and lobbying fees.

I had an amazing idea for a business that I don’t think exists, and definitely doesn’t exist in the US market, basically a PredictIt Marketplace for sports with multiple contracts for like every draft pick, every win total, every championship…

Like you could go buy Tom Brady yes for the HOF at 99c right now or like Trevor Lawrence yes for the HOF at like 3c or whatever… and buy or sell at any time. You could have contracts for total yards in a year, in a career, etc… And do that for every sport.

The problem is the legal expenses are going to be through the roof to figure out exactly what you are and are not allowed to do, exactly how you can market it, etc… And getting from zero users to having enough liquidity in the markets is very difficult, unless you’re basically willing to make the market yourself, which means you need a huge bankroll… and you may just invest a shit load into legal analysis up front and find out, “Yeah, that’s like totally illegal, but thanks for the money!”

PI for sports would be incredible and I’m in. Surely we’re not the only ones with that idea though (I think everyone on PI has thought of it, getting it done entirely another matter), polymarket had some sports games and the CFTC just cracked down on them for some markets, idk if they do sports now or not.

Trevor for the HOF is too soon for that sort of thing though but yeah we could come up with a bunch easily.

That’s the idea though, for people to “invest” in their deeply held convictions about players, so they can prove that they were right and they knew it first. You put that market up for like every 1st round QB at a minimum. Like I bet that would have gotten to 5c or 10c around the draft, and it’d probably be at 1c to 3c now.

As stupid as people are on PredictIt regarding politics/news, they’re just as dumb if not dumber about sports. Trust me, I have hosted sports talk radio before lol…

I meant that putting up markets that don’t resolve for 15 or 20 years isn’t the sort of thing I think should be done even if LOL at that stuff.

ie, when does NO resolve? Someone could still make it in 50 years from now on that vet committee like one gets in every year 5 years after he retires and he’s not even close to first list? Just stay away from that one I think.

Oh, I mean, given that you can buy or sell at any time, it doesn’t necessarily matter how long it takes to resolve, right? It’s the stock market, but for sports fans to invest in players. The key is just the liquidity, and as long as the company can get money cheap enough, the company can provide liquidity in the markets that are essentially guaranteed.

Something like this existed pre UIGEA, I cant remember what the site was called now. Theres definitely a lot of discussion out there on whether US gambling market evolves this way. I think maybe Rufus Peabody’s podcast has spent a fair bit of time talking about this. I think, like with poker, interstate pooling of liquidity becomes an issue.