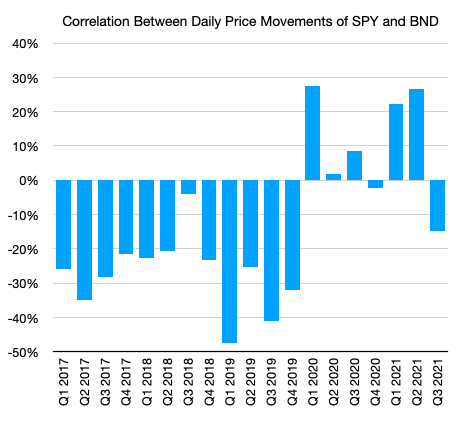

I made a post in April 2020 about this when I noticed that the pandemic crash had reversed this negative correlation, specifically in March 2020.

I never got around to digging any deeper to see if there were bond components that were disproportionately contributing to this, but I happened to revisit this last week to see if things had gone back to normal, and they haven’t. I still have no idea if it’s significant (or actionable in any way), but it still seems weird to me.