This is a tangent, but I don’t think that this is right. I think more volatility in the price level of the S&P is explained by changes in expected discount rates then in changes in expected earnings. But that’s just my intuition. If be happy to read any literature that states the opposite.

2 Likes

I think that depends on if you are including things like credit risk in the “discount rate”. We’ve had long periods of relatively stable Treasury yield curves where stock prices were still very volatile.

Anyway, I think the discussion has run it’s course. Bond math is a permanent blind spot for much of the (retail) investing space. See all the confusion in 2022 from people that didn’t (and still don’t) understand how their “safe” bonds could be down so much. It’s helpful for people to think of bonds as being a mechanism to participate in the lending market, and that tends to cool emotions because it gives people some comfort that at least when their bonds experience capital losses because of rising interest rate, that gives them an opportunity to issue future loans at the higher interest rates. This concept has some relevance to other asset classes, certainly. And it isn’t a magic bullet to make bond risk “go away”, it’s just a better and richer way to understand bonds, IMO.

1 Like

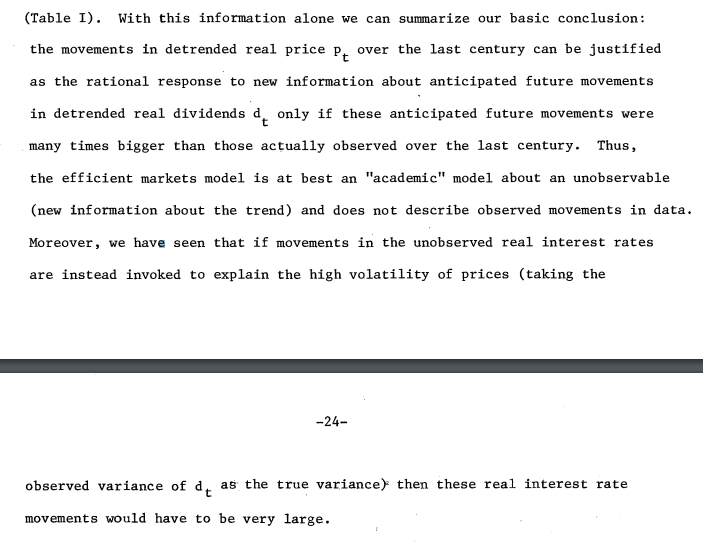

The paper that comes immediately to mind is Robert Shiller’s 1981 “Do Stock Prices Move Too Much to be Justified by Subsequent Changes in Dividends?”.

From that paper:

“We have seen that measures of stock price volatility over the past century appear to be far too high–five to thirteen times too high–to be attributed to new information about future real dividends if uncertainty about future dividends is measured by the sample standard deviations of real dividends around their long-run exponential growth path.”

This sounds more like a statement that stock price changes are not rationally tied to anything than a statement that they are tied more to changes in the risk free curve than they are to changes in the market’s expectation of future dividends.

Yes, I did read this paper (just now). And the conclusion is:

Now I’m interested to find some follow up literature with respect to this paper.

1 Like

Well, this gets into the whole divide about market efficiency vs. not. Shiller (of Irrational Exuberance fame) obviously falls on the side of this reflecting inefficient markets.

Someone like John Cochrane would look at exactly the same data and say something like, “Just like a bond’s price reflects discounted future payments, a stock price reflects discounted future dividends. Tautologically (and just like with bonds), a change in price of a stock can be viewed as a change in the required rate of return for holding that stock. Changes in that rate simply reflect changes in investors’ characteristics and expectations.”

Right, but with bonds (at least treasuries) no such speculation is necessary about the nature of the expectation and discounting. The cash flows are a contract, the price and the yield are perfect mathematical reflections of each other.

1 Like

2 and a half hours!

2 Likes

MOASS!!!

This dude’s going FPS on the production bells and whistles.

Definitely watch the part where he talks about people analyzing literal children’s books to find coded messages about BBBY and GME.

Update: last Friday was the Effective Date on which the bankruptcy plan got executed: shares were “canceled, released and extinguished”. Monday, the ticker ceased to exist after being put on OTC Markets’ deletion list as well as Finra’s. People who were long or short still see a ghost position in their accounts (I think until an action from the DTC), but it says $0 and shorts are no longer paying a borrow fee or putting up margin. Apes who direct-registered their shares (lol) can’t even log into their AST accounts (AST being the transfer agent).

Many apes are still bullish because they think this is a transition to a merger or Teddy shares or whatever. Apparently this same thing happened with Sears (SHLDQ) and there are Sears apes who are still bullish 11 months after their shares were canceled, so it’s likely that some BBBY apes will still be bullish a year or more from now.

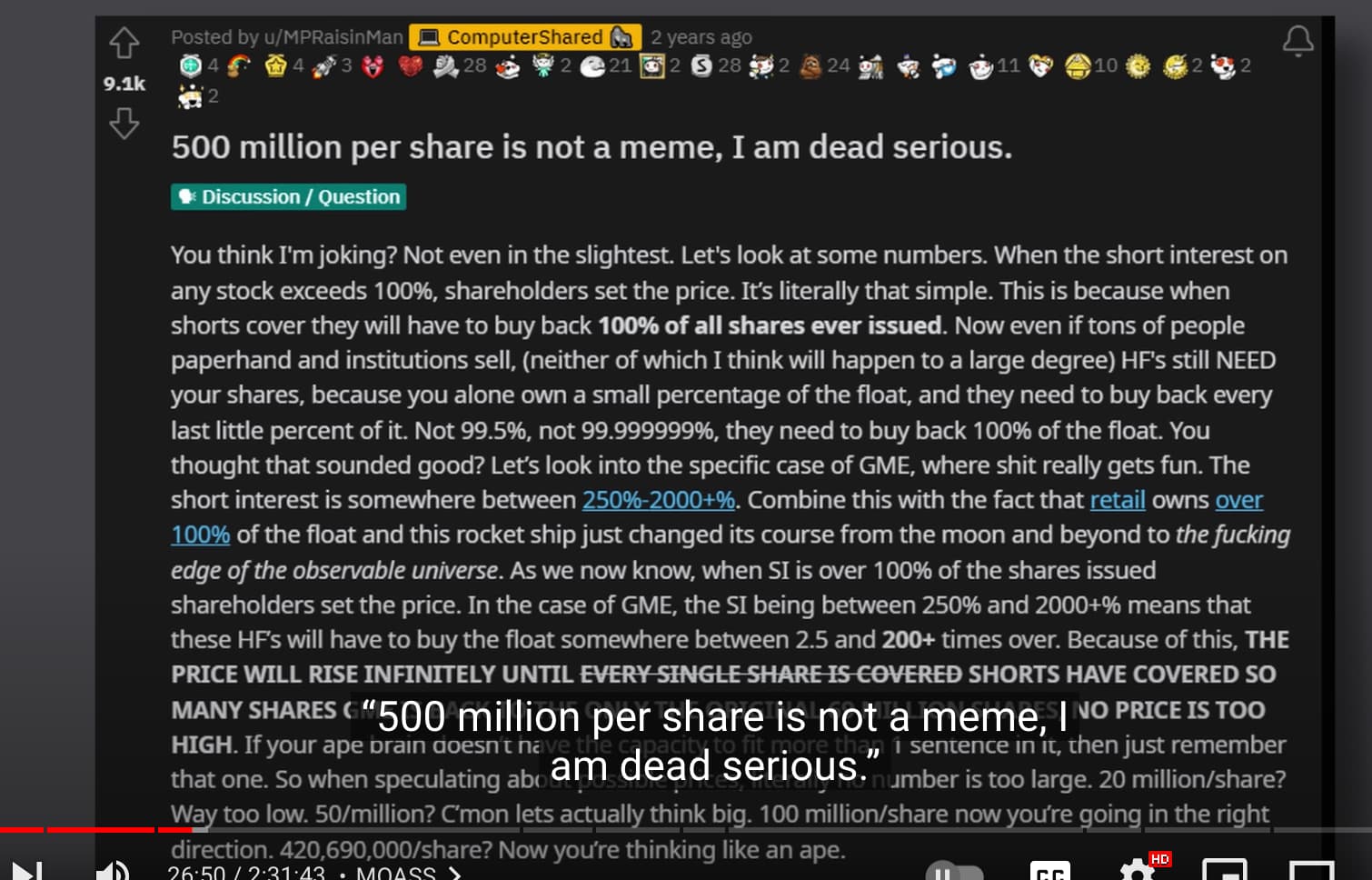

Lol they were really talking about $500 million per share. And the answer to anyone who questioned that? Literally, “Shut up! Do your research!”

That’s how these things always have to work. There has to be some talk about insane valuation somewhere down the line. Insane enough to make GME at $500/share look like it could be worth the risk, otherwise the music stops.

Right its as much of a ponzi as anything else. It only continues to work if more rubes buy in at higher and higher prices

1 Like

Which means you always have to peddle an exponential growth story for them to cling to, no matter how nonsensical.

Now do capitalism

2 Likes

Some person from the 1930s: Holy shit everyone who wants one has a job! Saints be praised!

CNN: No really, this is terrible. Let me explain why…

10 Likes

This guy man. Also note that Antarctica is spelled wrong. I guess the research didn’t involve how to actually spell the thing.

You know that nudes folder is filled with pictures he has solicited from his viewers, a bunch likely to be not of legal age.

I’m guessing it’s a joke. Those memers. Much irony. Wow.

Also from the icons it could be that the bottom 3 folders are actually empty? Windows users chime in.

you are correct, those three are empty folders