So PDEX hasn’t filed because they have to restate 3 years of financial statements because one of their investments they deemed materially worthless is actually worth 2.7 million according to their estimates which is worth about 5% of the company’s market cap as per the closing price today.

This should help the stock price I assume, but on a thinly traded microcap is their a strong possibility the headline of restating inaccurate financial statements makes the price go down?

I wouldn’t read this as good news at all. One of the resident experts can confirm, but I’m pretty sure you don’t restate because something you wrote off turns out to have value after all. Even if that was the rule, they aren’t delaying their 10-K because the auditors can’t add a number to their spreadsheets fast enough.

Reading between the lines, they took a material and unsupportable tax write off for the note and they’re trying to figure out exactly how big of a liability they need to book. 2018 should be out-of-statute, so in order for that year not to be closed and this to be a problem, they might need to be under audit already or be concerned that this is a fraud/penalty situation, which would make the tax bill worse.

I asked a question their website on September 13 when they would file and got a response from the CFO just now that they plan to file their 10k on October 13th. Unsure if that changes things.

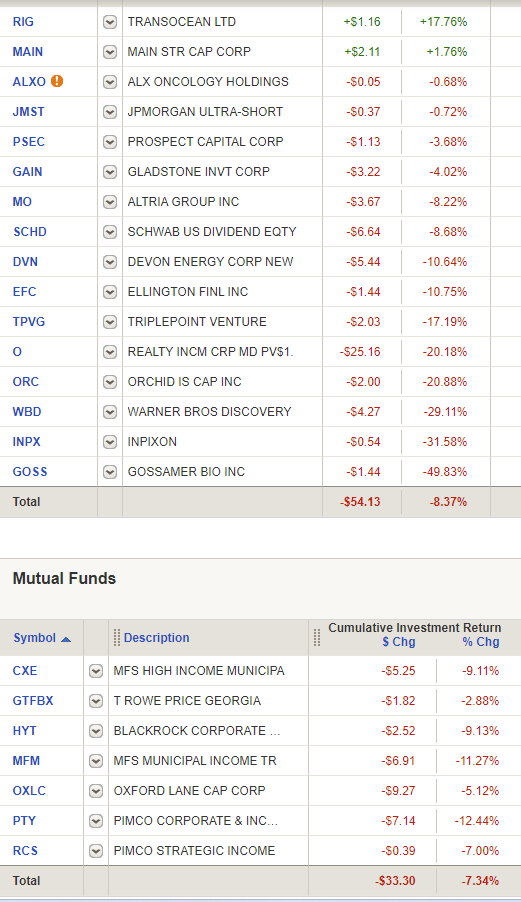

Those are a couple of muni funds, plus some CEFs that I meant to buy in my IRA but they went in my brokerage account by mistake and shouldn’t be there. I’m just stubbornly holding them at the moment because I don’t want to sell red ink.

Not buying shit but treasuries til the end of the year, not as long as the risk-free rate is 5% and climbing, screw it. Dow also now red for the year.

Was just reading an article yesterday about how long term bonds should be super attractive because investors can lock in today’s interest rates for decades, but bond owners are getting burned every time rates go up and people are afraid to jump into them because it’s not clear rate increases have peaked or that the inflation the Fed is trying to stop is under control.

If those municipal bond funds own a bunch of medium to long term bonds from a few years ago when rates were lower, they don’t look too valuable because today you can get a 30 year treasury for around 5%

If you buy the individual bonds and hold them to term then you’re not really exposed to this risk. You will (assuming the bond doesn’t default) earn the current yield to maturity, then you’ll reinvest the proceeds at the higher future rates. In the interim, you might see unrealized capital losses in the bond if interest rates rise, but you are not forced to sell the bond. And if you did sell the bond, you could theoretically invest the lower proceeds of the sale in the higher future interest rates, and you’d find it’s mostly a wash.

The risk of rising interest rates for bonds really only exists if you experience a bond fund like a typical retail investor, where you hold a number of units in a fund and the investment is a complete abstraction of a marked-to-market price that sometimes throws off interest. This is looking at bonds as if the bonds were stocks, and it’s not really the right way to look at them but I understand why people do. If you hold a bond fund and interest rates rise, you will get a statement from your investment company that says that you lost money. Modern portfolio theory is good for a lot of things, but the process of making every investment an abstraction that has an expected return, a standard deviation of annual returns, and a correlation matrix with other investments has led to a lot of investors who don’t understand what the actual investments are. They don’t think of bonds and loans and stocks as ownership, to their own disadvantage.

i think for most people who have started buying bonds/treasuries/CDs after rates have shot up recently they are doing it with money that would otherwise be invested in the SP500 so it’s only natural to compare the return of your individual bond/bond fund with your hypothetical return if you had stayed invested in SPY

I disagree with this idea that buying individual bonds is this one weird trick that fundamentally changes the risk profile of one’s fixed income allocation. The main difference between the two is that the individual bond’s duration is going down day by day whereas (typically) the bond fund is continuously re-upping its duration. All else equal, the longer duration bond investment will have more interest rate risk, and thus higher expected returns. Whether that’s good or bad depends on your investing goals.

Something like IBTI will be equivalent to buying a 5 year treasury and holding to maturity (and may be a cheaper and more convenient option).

I’ve got about 20% of my portfolio in the fidelity money market thing that’s earning close to 5% (I’m still paranoid that I’m reading that wrong somehow). It makes sweating market drops a lot easier. At least if the market totally crashes I’ll have some dry powder.

The key isn’t to actually buy individual bonds, that just helps to illustrate the main point which is that precipitous decreases in the market value of bonds because of increases in interest rate are compensated by the increased interest rates. The increase in the interest rate and the decrease in the present value of the bond are the same thing, and because people don’t generally understand the math of bonds, they can’t connect those two ideas.

All capital assets are a claim on future cash flows, so higher discount rates are always bad for their value unless the change in discount rates is accompanied by an offsetting increase in the cash flows.

This is exactly the point. When you are a bond investor, the same higher interest rates that depress the PV of the bond also increases the cash flows that bond investor can get by lending money in the new, higher interest rate environment.

I agree with that. The only thing that is unique about bonds is the pure mathematical relationship between the future cash flows, the yield you earn as an investor, and the market value. If you don’t sell the bond, then you collect the exact same cash flows from it as you did before interest rates rose. If you do sell the bond, you can reinvest the proceeds in the new, higher interest rate environment. In either case you tend to be okay in the long run, even though you might get an ugly looking report on the market value of your bond. Stocks are not as clean - if a stock’s price goes way down, it’s much more likely that it’s because market sentiment is that the future cash flows will be less than previously expected. It may also be because of changes in the risk free rate, but it is often just because of fears that the company will not be as profitable.

There are complicating factors in the bond market of course. If taxes are in the air then that matters. If there are liquidity or credit spreads in the bond yield then the purity of the math is reduced. I don’t think anything I’m saying is controversial. It’s well established that a highly predictive metric for expected future bond returns is the current yield on the bond. This is specifically because when interest rates inevitably change the short term capital gains/losses on the bonds are compensated by the prospects for lower/higher interest on bonds in the future.

I missed this before and I think it might explain why we’re talking past each other.

The changes in the price of bonds or stocks will generally reflect some combination of the market’s expectation of the future cash flows on the asset plus the market’s mathematical discounting of those expected cash flows at the risk free rate.

For bonds, most of the change in the price is from changes in the risk free rate curve. Not always, of course. In the GFC, the prices of corporate bonds fell mostly because credit spreads blew out, i.e. the market wrote down the expected future cash flows from the corporate bonds because of the higher probability of defaults. For stocks,most of the change in prices is from the change in the expected future cash flows. The impact of changes in the risk free curve will impact stock prices to the extent that they discount future cash flows more, but usually that impact is less that the volatile swings in market expectations of future cash profits.