I remember the lender telling us we could qualify for twice the amount my wife and I had agreed made sense for our budget, and that we should always buy as much house as we could afford because nobody ever regrets it.

That was in 2002, and I remember being concerned that we were surely buying near the top of the market. Had no clue it had many more years to run.

Yeah same here. I did the math on $600k and even if I had enough for a down payment (which I didn’t) I was going to be pretty poor for a while. People generally suck at math. How many others found their dream home and got sucked into that?

I make twice that now and I’d still struggle with $600k lol.

My friend managed to buy pretty much right at the peak (and then had to short sell to get out of it at the bottom). Nailed it.

He said that literally every time they went in to discuss the house or sign things, the mortgage douches made the deal a little worse, until they got right up to their breaking point where they were ready to walk away.

Big dip most Mondays, IMO, market seems to like to minimize the drip, drip on coronavirus that happens during the week then freak out about the news that piles up during the weekend.

Nah, the auto dip buyers counteract the people trying to beat the pre-Monday sell-off. Takes all weekend for the dip buyers to be temporarily convinced of corona seriousness, and they finally let stocks sell off Monday. By Tuesday, the dip buyers are done being patient and start buying again.

The problem with “obvious” future downward market moves is that you have to be right three ways, not one. You have to be right about the move, time your bet correctly AND time your re-entry correctly.

Nah, just sell with phased in BUY THE DIPS strategy. Then just need to be right in one decision that stocks will eventually be below were you sold at. And you are still getting a return in bonds in the meantime.

As a TRUST THE MARKET person, you can’t say that the market is pricing stocks correctly and bonds incorrectly. So it’s you want to go to the market and buy all the oranges you can afford cuz that’s what you do, buy oranges all day, everyday.

I say nah, they jacked up the prices on oranges this week, f that, I’m buying apples. I might start buying oranges in future weeks if the prices get more reasonable, aka Ill BUY THE DIPS.

JT,

Given your fears/concerns, it sounds like your current asset allocation is too heavily tilted towards stocks. You should figure out what your goal allocation is and then sell whatever amount of stocks gets you there. Then, once you’re at the “right for you” allocation, just keep it there.

On the other hand, if you’re saying, “I’m at the appropriate allocation for normal times, it’s just that right now are UNNORMAL times”, then either:

You’re wrong about your appropriate allocation, because it’s generating too much emotion right now

or

You should ignore those feelings, stop looking at your balances, and just carry on.

Edit:

The good news is that it probably doesn’t matter too much. Believing that the market is generally impossible to beat means ALSO believing that it’s very difficult to make obviously wrong decisions. (You can intentionally lose at chess, but it’s much harder to intentionally lose playing roulette on a wheel without zeroes.) The two things that you CAN do that will certainly cause worse results are:

Pay a lot of transactions costs via frequent buying and selling

Buying securities with high expense ratios

If you avoid those things and you focus on a diversified portfolio, then life should be good.

What you need is an asset allocation (of hopefully low cost index funds) you can sleep with. Then buy and hold and periodically rebalance to that predetermined asset allocation. Sounds like you are finding your way there now. It is really the perfect thing for you imo.

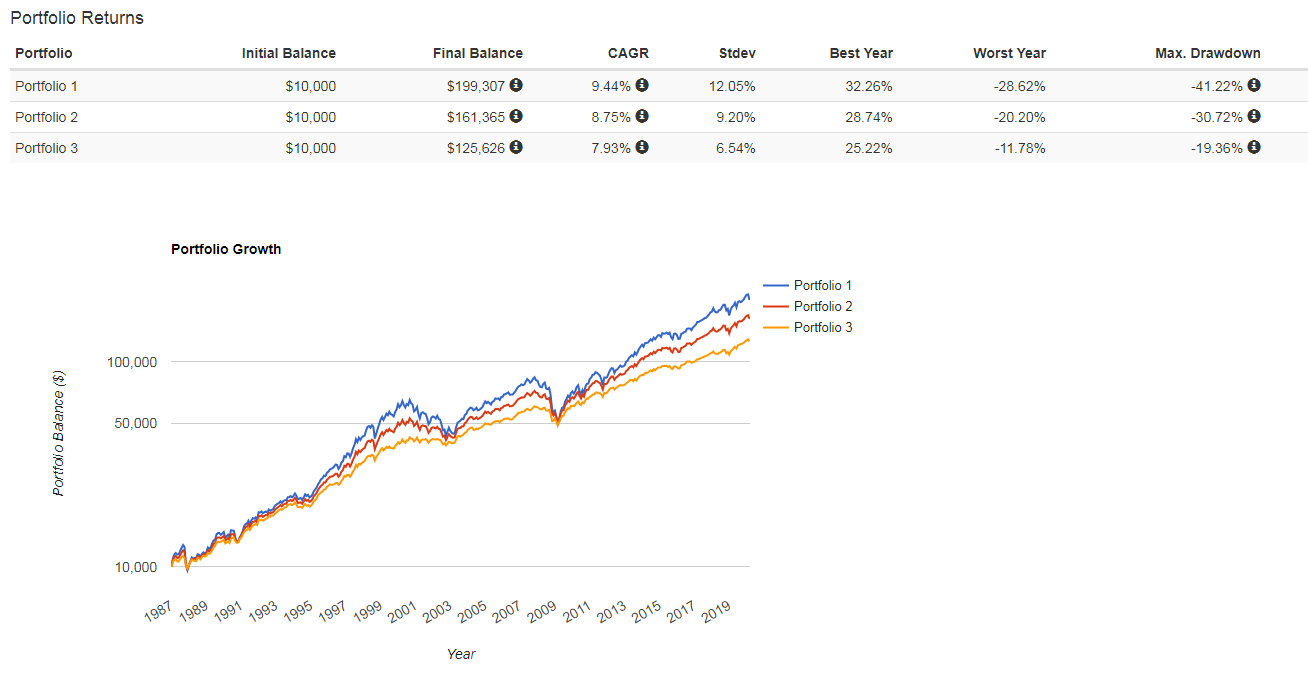

So all that just means that you were invested too much in stocks and not enough in bonds. Here’s three simple model portfolios, 80/20 stocks/bonds (close to what you were at), 60/40 (old fashioned asset allocation advice), and 40/60 (very conservative allocations that a conservative retired investor might use).

So in 2009 your 80/20 portfolio would have gotten killed, you would have had a 41% max draw down, more than twice what you’ve seen the past few weeks. You’re obviously not comfortable with that sort of risk level, so let’s look at the 60/40 portfolio. There you would have had a 30% drawdown in 2009. Comfortable with that? OK, if not then maybe a 40/60 portfolio is more your speed. You’re only going to take a 20% hit in the disaster that was 2009. But the point is to pick an asset allocation that matches your risk tolerance, and then just stick with that. And if you enter a period of volatility that makes you want to sell stock, then you should probably be holding more bonds. Not just then – always. Because you never know when the downswings will happen.

You can still save a lot of money if you time your re-entry badly and hold vs. hold the whole time. So once you sell and it crashes you’re already doing well. Assuming of course we don’t see 1929 where it took like 25 years to recover in inflation-adjusted dollars (note I heard that one time, could be wrong).

Or be right about the move, start putting money in when it drops 5% and keep adding every time it drops another 5% from ATH until you run out of powder, then ride it out.

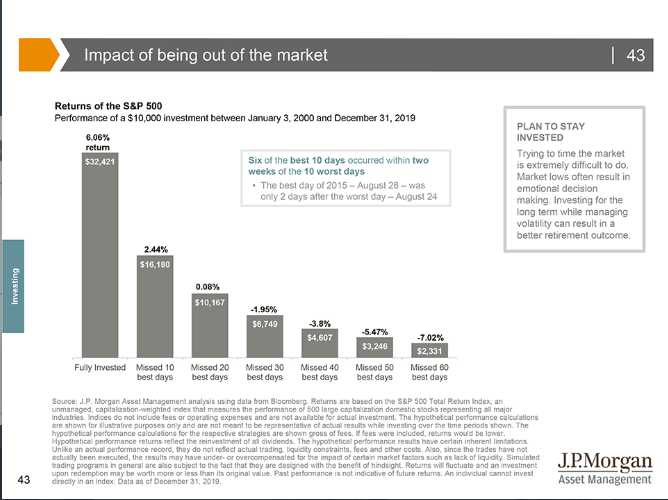

Obviously this is nit-picky because the odds of actually being in or out on the best or worst days are super rare, and most people don’t go 100% stock to 100% cash and back in but I think it adds some value to the conversation.

To me the interesting thing is that 60% of the best 10 days were within two weeks of the worst 10 days. This just shows if you make a knee-jerk reaction and go more conservative after incurring most of the losses in a more aggressive allocation, and then in turn catch less of the upside because you didn’t re-allocate before things turned around you can get hosed.

With that said I think it’s negligent to just blindly HODL forever and never make adjustments. However, if your long-term outlook and goals haven’t changed I think it’s foolish to make large changes to your AA on a gut feeling or whim.