Curious because I think we’re around the same age. What percent of your bonds are in inflation protected vehicles? I’m at 50% of bonds now being inflation protected (combo of TIPS and I-Bonds) and probably headed higher gradually over the next several years.

My overall allocation is:

40% domestic equity

20% international equity

10% cash/short term

15% inflation protected fixed

15% domestic bonds

I’ve been all over the place with my AA the last couple of years, but I’m determined to keeping a basic 60/40 (with some percent of the 40 being cash/short term) from now on and just riding out any bumps.

I think we’re 3-5 years out from FI, and 10 years out from retiring.

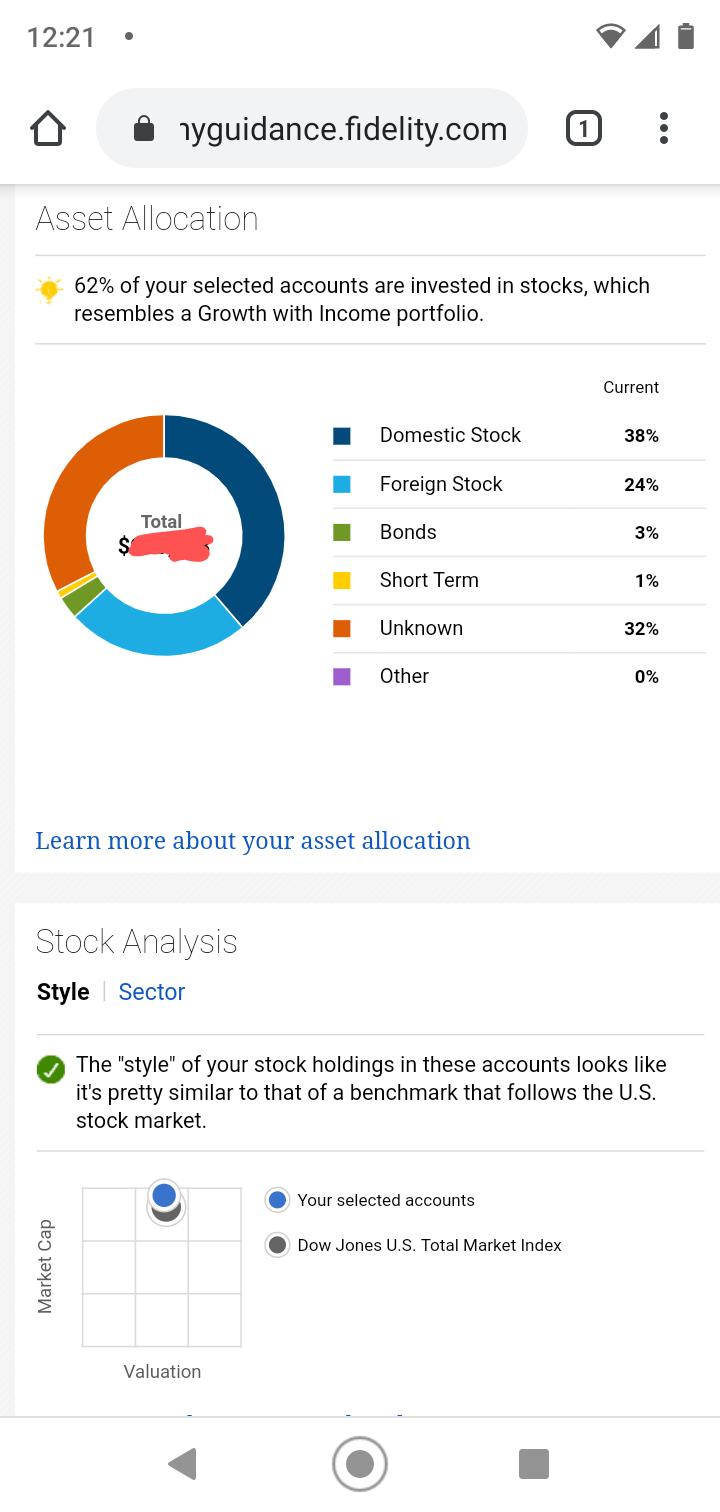

I don’t have any inflation-protected bonds. In the pie chart below the “Unknown” piece is an annuity invested 100% in the Vanguard Total Bond fund. At this point, I’m directing my ongoing deposits to go into the Vanguard BNDX fund.

Do you have no plans to? I figure as long as bonds are yielding crap that can at least provide me a good hedge against inflation. And inflation will likely bring higher interest rates, which will have a negative effect on most bond funds, but should help inflation protected bonds. (Of course I’m no expert and get this stuff wrong frequently, but that’s my thinking. Plus many of the finance pros recommend a heavy dose of TIPS as you approach retirement.)

Finance bros also love Series EE bonds, but you have to buy them through Treasury Direct and I’m too lazy to navigate that. Plus I think you can only buy $10k.

Yeah, $10k per year per SSN. And my opinion is that you shouldn’t purchase them unless you’re pretty sure you can hold for 20 years to capture the doubling. I have these as last on the list for our investments to max every year:

It took me 10 minutes each to set up TD accounts for me and my wife, so not that bad. I guess some people run into issues and create a mess, but it was straightforward for me anyway.

If you do it right now (and you’re married) you can have $40k in there by next month (or $80k if you do I-Bonds too) and $60k (or $120k with I-Bonds) in a little over a year from now.

I-bonds are ideal for short terms savings. Only downside is you have to hold for 1-year and then if you cash in before 5-years you take a small interest rate hit.

Upside is they pay much better than any other short term cash account.

I haven’t given any thought to them in a long time, but isn’t there some weird process for buying them? I’ve heard of people getting their tax refunds in I bonds for this reason.

Edit: I think the weird thing I was thinking about is that you can only buy 10K, so some people ask for part of tax return in I bond form to get more.

Speaking of all these low return investments. Do people have mortgage offsets in America? Basically everyone I know in Aus uses them. I just keep my cash in that savings account and save 2.04% interest I’d be paying on that amount within my loan regardless. I think of it as a 2% savings account with no tax on the interest.

Wow must be illegal in US for some reason. Its a joke how good it is and, at least for me, it only adds 0.05% to my rate (most big banks it adds 0.3-0.5%).

Also, in USA#1, people would get mad at the bank for reducing their mortgage interest payments because it they want the corresponding tax deduction. YOU’RE RUINING MY TAX DEDUCTION THIS IS ALMOST AS BAD AS GETTING A PAY INCREASE THAT PUTS ME IN A HIGHER TAX BRACKET!