Yeah, I know. The issue right now is it looks like they are going to withhold about $4k too much based on my estimates, and I would rather get that number closer to about 0. It used to be easy to do this. Maybe I just need to go through that entire IRS exercise and see what numbers they come up with. It’s just irritating that I can’t set it myself. All I can do is enter my numbers and then the IRS will decide what they want to withhold.

So you can’t just arbitrarily claim allowances anymore? I usually claim about 4 since my mortgage interest deduction balances that out.

Nope, apparently not.

Anyone with a guess as to when the IRS will start processing paper returns that were filed in mid-March?

I wonder if mine is still claiming them from last year, so I’m like grandfathered in at my work or something? I know my paycheck didn’t change much in 2020.

I don’t recall mine changing at all in January either. So I think things will stay the same until you want to update it.

Speaking of bonuses, did the May bonus come in as expected?

Yes, it did. I actually got 110% of what I expected to be the top end. We ended up donating our entire stimulus check to various charities because we felt so fortunate to both still have jobs and be getting bonuses and all. I ended up putting the entire bonus into our EF for now rather than investing most of it like I normally would.

I can’t remember, where you also waiting on a bonus and wondering if it would come through?

2 Likes

Congrats! I know that was a huge sweat.

Not me. Must have been someone else.

1 Like

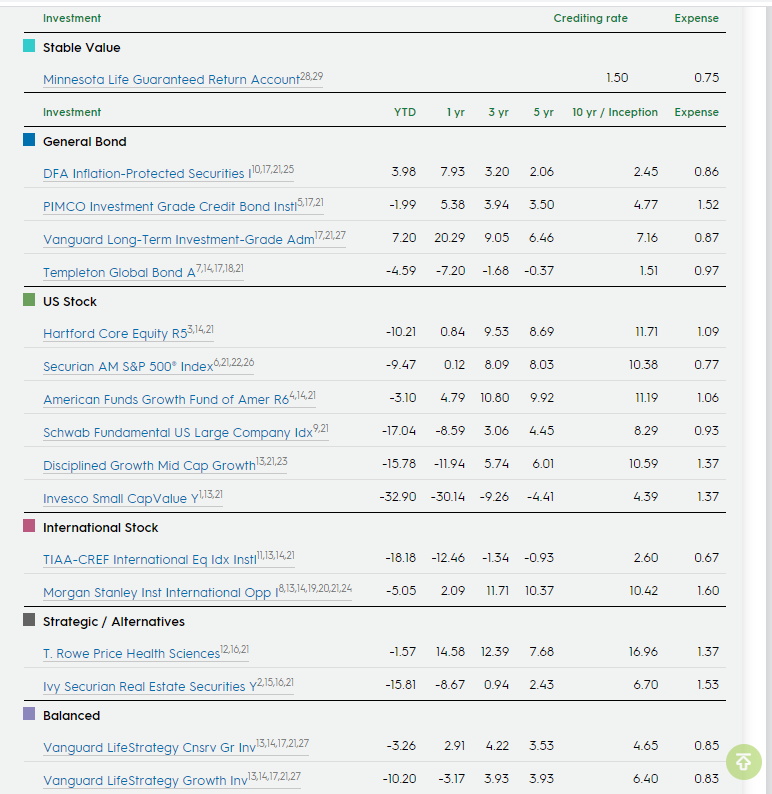

yes i work for a small company (<500 employees). the 401k is done through Securian Financial (Formerly Minnesota Life Insurance)

this one is even worse. 0.77 just to track the S&P

I wonder if you could work out a deal with your company where you quit for just a short time, don’t lose your seniority, but long enough you can convert your 401k into an IRA.

Can you imagine if W had succeeded in privatizing social security?

The entire financial services industry is basically a scam except for Vanguard, Fidelity and term life insurance.

im fairly young (30), only been at this company for a short time so only have low 5 figures in this 401k so probably not worth the time/effort to do something like that.

but i will be much quicker to take the next offer that comes along because of this (along with the shitty healthcare plan)

I would say that there is a useful industry for high net worth investors. For households with a couple of million dollars comprised of two full time professionals, you actually get reasonable service for your basis point fees. I am not confident about the value of active management but there is some real value to having someone deal with you asset allocation and tax loss harvesting, plus coordination with accountants etc., and HNW investors can negotiate on price.

It’s because the economic value of the option has two components: the immediate value and the time value. Might be easiest to see with a simple example.

Suppose you have a stock that currently trades for $100. This is a very special stock - you know that in exactly one month it’s either going to be worth $150 or $60. (Think of it like a single-drug pharmaceutical company whose major drug either will or won’t be granted a patent extension.) The odds are 50-50.

Now suppose you’ve got an option to buy the stock for $90 in exactly one month’s time. You could exercise that option now, paying the $90 exercise price and immediately selling the stock for $100, getting a net payoff of $10. That’s the option’s immediate value, equal to max(current stock price - option exercise price, 0).

But the immediate value isn’t the economic value of the option. Instead, it’s the lower bound of the option’s price - if the option ever traded for less than the immediate value, smart econheads could buy the option, exercise it, and immediately sell the stock for guaranteed immediate profit.

The economic value of the option takes into account that lots of good things could happen before the option’s expiration, which would make the option much more valuable. Lots of bad things could happen, too, but that’s ok because if the bad stuff happens, you’re not stuck with the stock, you just throw away the option without exercising it.

So in this case, you’d look at the two possible outcomes: the stock will either be worth $150 in a month or $60 in a month. If the stock ends up being worth $150, then an option to buy the stock for $90 will be worth $60 at expiration. If the stock ends up being worth $60, then the option to buy the stock for $90 will be worthless. If the probability of each outcome is 50%, then the expected value of the option is $60*.5 + $0*.5 = $30. (This is why higher variance/volatility makes options so much more valuable, even if they don’t change the EV of the underlying stock. In this example, if you ratchet up volatility so that the possible outcomes are $210 and $0, the EV of the stock is still $105, but the EV of the option goes up to $(210-90) *.5 + $0 * .5 = $60.)

So in this case, the immediate value of the option is $10. That’s what you’d get if you exercised early. But if you instead sold the option to someone else, you’d get the expected value of $30.

2 Likes

Thanks. That makes perfect sense.

3000 tonight!

Super interesting blog/article on lol doordash by former 2+2er andathar.

8 Likes

In related news, Uber is going broke (and their strategy is to…acquire a capital-incinerating firm). They’re firing thousands of people and abandoning self-driving / self-trucking. LOL Uber.

Yet they’re only 15% off their ATH!