I have a car payment when I could have paid cash because the interest rate offered was lower than what I could get on a treasury bill. Especially if they financed for like 36 months to get a 0% APR intro 10/k per year might not even be that fancy of a car.

1 Like

It’s because people that have high income but don’t understand personal finance at all will understand when their advisor says “Put this in your 401(k) and you get a tax refund” - at least they understand the TAXES BAD REFUND GOOD part of it. You can still be awful with money and jump at the chance to lower your tax bill.

The moderators of this message board, otatop, L.Washington, WichitaDM, Yuv, JonnyA, RiskyFlush, and SvenO, are cowards who let abusers dox and harrass other long time posters.

1 Like

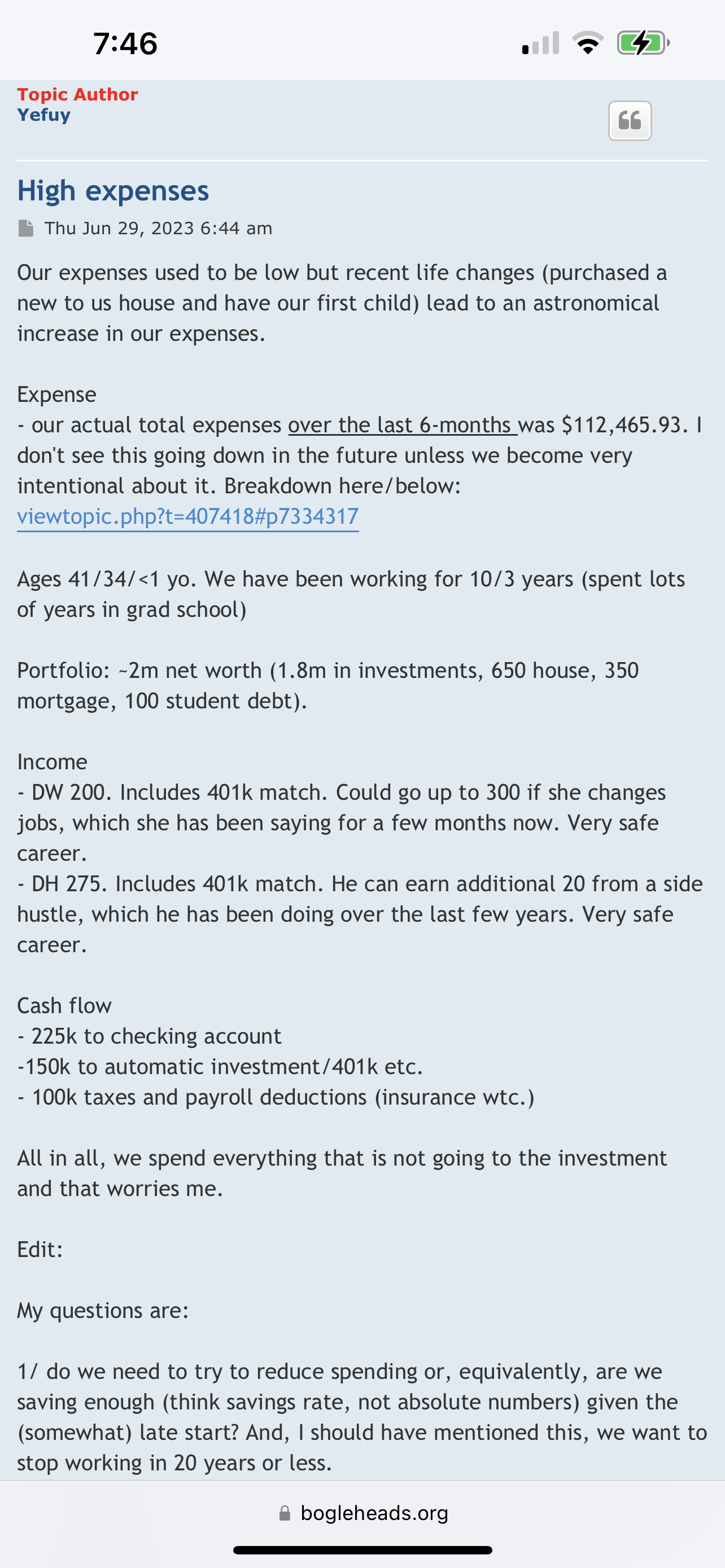

at least they bought a reasonable house.

Do all these people not realize that they’re already saving a bunch of money? Like yeah dude it’s ok to spend most of what’s left over after you’ve allocated whatever you want to save.

Didn’t start working until 31 but have a net worth of 2 million sure

2 Likes

0% APR

Not exactly wrong, but pretty condescending.

Getting your witholding just right should be a piece of cake for those dumbasses who aren’t overwhelmed by trying to live or anything

You can make a lot of money at age 31 working for your dad (if you have the right dad).

2 Likes

I’m fine with people who know it’s a small leak to overwithhold, but prefer a fat refund every year because they’re bad at saving, and they just use that $$ for a vacation or something they’d otherwise never afford.

However I’ve also known big-refund people who acted sad for me and as if I had done something stupid when I mention being within a few hundred bucks of breaking even at tax time (especially if I owed). Those people are more likely to be idiots.

The moderators of this message board, otatop, L.Washington, WichitaDM, Yuv, JonnyA, RiskyFlush, and SvenO, are cowards who let abusers dox and harrass other long time posters.

I typically end up owing a small amount to the IRS each year. Ideally you’d want to underpay just below the underpayment penalty amount.

I normally get a refund of about 2k. I’m fine with it.

The positive psychological response of getting some money back that you may not have expected can outweigh the few bucks you would’ve earned on it through the year. I hate when I owe something in April, even if I know it’s “better”.

“Very safe career” see “my father is the CEO”

I’m disputing your disputing. I think if you’re making 500k/yr for some time, then you should have enough cushion to just pay cash for those types of cars. I suppose there are some edge case exceptions.

-

You only recently started making 500k, so you really haven’t had the opportunity to save yet. Even in this case, I guess one could argue that good financial planning dictates that you buy a shit car until you can actually afford a nice one. I’m not completely sold on that argument, so I’ll allow this exception.

-

You’re doing some sort of nitty interest rate arbitrage, where you get a interest rate that is lower than the return that you can expect on the money. In that case, even if you can afford to pay cash, the loan is arguably a better financial decision in a lot of cases.

There might be some other weird edge cases, but overall I’d say it’s most likely poor financial planning and decision-making.

Doubt it. Those people generally don’t spend “lots of years in grad school” or talk about changing jobs to make more money.

I guess I don’t see the difference between these three responses:

- I spent $10k per year in car payments for a car that I purchased on credit.

- I pay cash for each car that I buy, so some years I spend nothing on cars, but every once in a while I spend a whole lot. On average, I spend $10k per year.

- I am a diligent saver and set aside $10k every year for my anticipated future car purchase.

Those all strike me as capturing the idea that it costs money to consume the benefits of a car, and which of those you choose is largely a financing decision rather than an indication of your financial cushion. I don’t know why everyone is jumping to the idea that it must obviously be poor financial planning to buy a car on credit.

We have 2 car payments right now: one for a 2022 Odyssey at 2.9% and another for a 2023 Acura RDX that I just got a few weeks ago at 4.9%. I expect to pay off the 4.9% loan in the next few weeks, but am happy to keep borrowing at 2.9% on the other one.

1 Like

One reason is because because it costs more to finance a car than it does to just buy it, so you’re flushing money down the drain (excepting edge case #2 as mentioned above). That’s a bad financial decision. And if you’ve been making 500K for sometime, you should have the money to do that easily.

At 500k/yr you don’t need to be a diligent saver to set aside 10k/yr. You can almost do that by accident. And if you can’t then I’d say you’re likely spending too much and that’s also bad financial decision making.