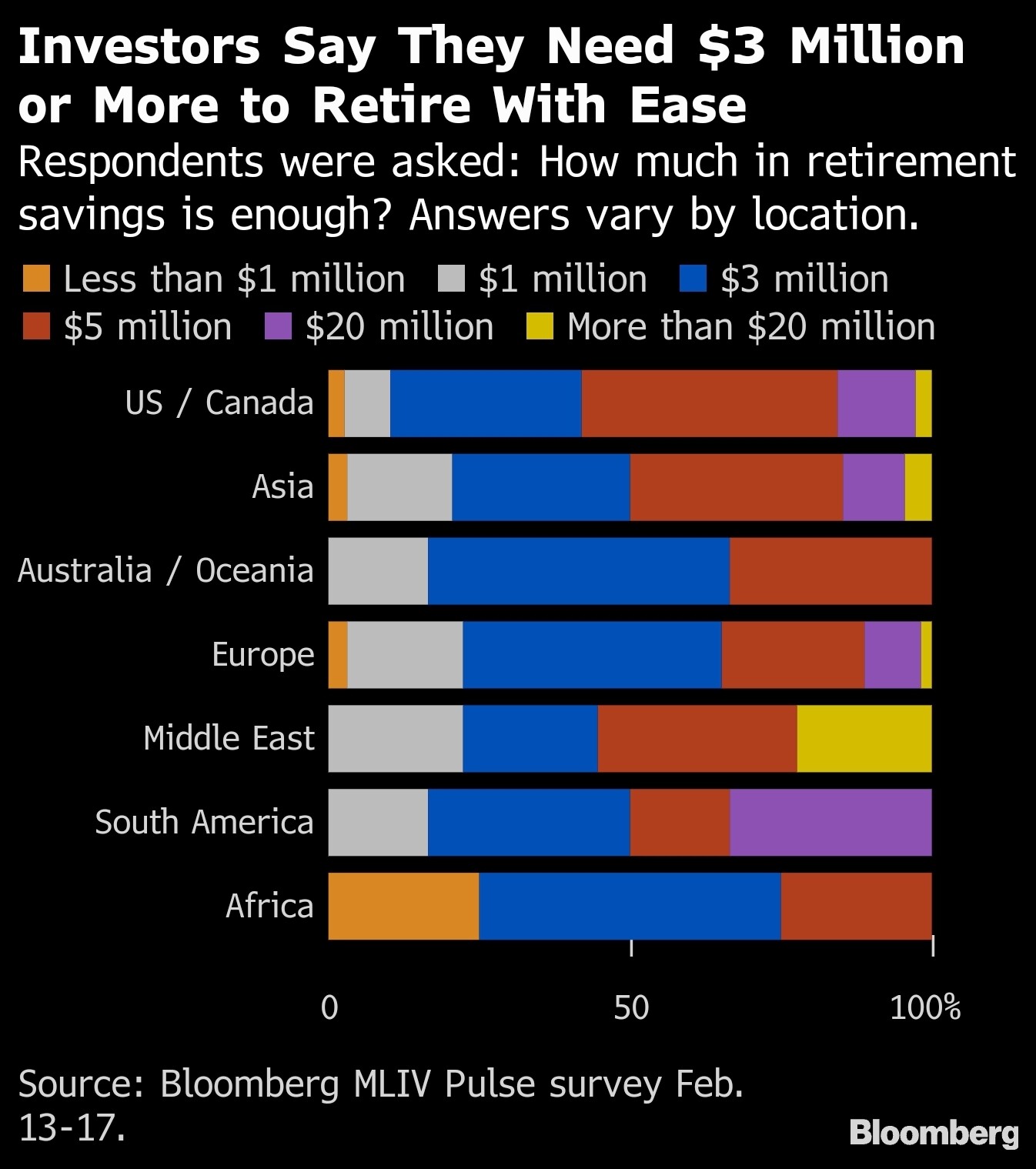

I’m getting a lot of articles served to me online about this concept. They say more people are trying to achieve this through various combinations of working and investing. I’m probably seeing them because I start every morning by Googling “get rich quick” and “easy to fake illness to get out of work” but maybe you’re seeing these stories too.

From what I can gather, the general guidelines for reaching this status are having at least 25 years full salary saved up. And that, supposedly, if conservatively invested, can maintain one’s normal lifestyle indefinitely.

I’m curious if any of the other Big Brains here are reaching for this goal, and maybe we can share tips or at least repost news articles about it and laugh at how delusional other people are for thinking they could ever extricate themselves from the soul-crushing gears of capitalism

Based on how things are going right now, at what age do you realistically expect to retire?

Under 40

40-50

51-60

61-65

66-70

71-75

76+ (aka never)

0voters

What multiple of your current salary do you think would be appropriate for you to call it quits and retire?

5x

10x

15x

20x

25x

30x

35x

40x

45x

50x

I’m a federal judge or something and my job is so easy I could comfortably do it while sitting on the toilet half-conscious

Your age pole is a bit wonky, 40-50 and 51-60 are too big of increments imo. I’m shooting for 50 but that’s only like six years away. 52 might be more reasonable. And I might not retire but if I don’t then for sure try to find an easier job with half the pay.

This is VERY conservative. Safe withdrawal rate is like 4%. There are a few bad runs in history where you might have gone broke with this rate but it’s a good rule of thumb. And of course for early retirement you can make adjustments: cut costs, get a job, whatever. A few adjustments like that go a long way. 3.5% might be a safer SWR. 3% would be way overkill.

But you’re asking about multiples of current salary when you should be talking about multiples of current expenses. 25x is a reasonable multiple of your expected retirement outlays, but way overkill if you’re saving aggressively and don’t expect your spending to increase when you retire. And if you’re thinking about retiring early, you’re not spending your whole salary. One more thing to consider is that retirees tend to spend the most early in their retirement and less as they get older.

I’m shooting for 53 or so, but I plan to work a little, hope to just get something like working at a greenhouse part time, seasonally. There’s a Dunkin’ that is near some snowmobile trails, where I could mountain bike or cross country ski to work, but that might suck.

Second @TheHip41 strategy - I have a good job but my wife works in finance.

I’ve always kind of figured on a 3.5% withdrawal rate.

Some of the articles I’ve read on this topic interview couples in their 30s and they talk about how they want to cut expenses, but I don’t think it’s realistic to expect the recreational benefit of more free time to really replace the base human desire to buy the newest gadgets or fashions.

I don’t want to have to sell my blood plasma or work part time as a cashier so I can buy a holographic iPhone 16, that’s not early retirement to me. That’s being unemployed, or trading down my current lifestyle for a bohemian one, which I respect but don’t want to do. Like any of us could become a surf bum and live full time in a motel by picking up recyclables from the beach and panhandling. But that’s not FIRE, that’s a mental breakdown.

My vision of FIRE is maintaining the lifestyle I’m accustomed to, and cutting out both working and saving.

My reference point right now is 55, since that is when I would be able to quit without losing my deferred compensation. But I’d like to retire earlier than that. Realistically I could retire now, but I feel like I’d be leaving so much money on the table. And if I did that it would probably be prudent to move somewhere with a lower cost of living, even though I really like living in NYC.

I feel like there’s a shit ton of information out there but like 98% of it boils down to one of two things:

Make more money either through income, investments, or both.

Spend less money

I think your focus is in the right place and the people who are the FIRE true believers who take #2 to the extremes are largely living a miserable life.

I think the biggest key is to be very thoughtful about what you spend your money on so that you’re using your money to actually give yourself happiness and not just to spend up to what you make because you’re capable.

I’ve been thinking about when I can retire a lot. I’m unsure of how to calculate everything as I’ll get a pension plus the more normal retirement stuff.

Yeah I always felt the people who spend 20 years living in a shoebox and eating rice and beans so they can retire at 40 are gonna have the hardest time learning to enjoy their long retirement, those habits tend to stick.

I mean it should just be a matter of calculating what you’d have coming in from pension + your nest egg withdrawal % of choice, and see if it meets what you want to live off every year.

Of course figuring that second part of it can be tricky. Things like a paid-off mortgage, reduced car expenses from not commuting, not actually having to save X% of your salary anymore, etc. all reduce your monthly nut, but things like having to pay for your own medical coverage until Medicare kicks in can be a doozy the other way. And some people might want to double what they spend on hobbies and vacations after retirement, while others might be happy with the status quo.

I’ve also got half a ribeye and some mashed potatoes left over from a vendor taking me out to dinner yesterday. Free dinners and lunches: another cornerstone of my financial planning.

Here’s some grist for your FIRE mill: People don’t actually enjoy spending lavishly; people spend lavishly to justify all the life they wasted working.

There are so many great hobbies that cost basically $0: reading, chess, talking to friends, masturbation. Quit being so precious and thinking you need to beat off on a yacht or some shit. Get a library card ffs.

FIRE is a romantic idea for me. It is a personal moonshot goal because even if I miss a little bit (on either money or time side), I’ll still be in a very financially strong position for decades. I struggled financially living paycheck-to-paycheck for most of my 20s and early 30s, so a lot of the “why” to strive for financial independence is long-term basic financial security. I have learned a lot along the way about money and even though I’m about 15-20% of the way into this journey, I already feel a lot less anxiety around money, work, and switching jobs which is saying something since I work in tech in a big tech hub.

As a late starter to the game, my conservative projections still have me in a place to FIRE at around 50-52 with around 25x my annual spending. These numbers may be a bit fluid for a few reasons though:

I don’t own any property. Due to my financial security issues, I could totally see me continuing to work to pay off a mortgage once I get one. Though at that point I’d probably stop or slow investing to shovel more into the house.

My partner has expressed little interest in the “retire early” part and she wants to keep making a lot of money. I wonder if her tune will change after I retire though. Thankfully we have a number of years to continue having this conversation before it is reality.

I probably won’t “retire” fully. I will likely downshift a few gears in my career into either some sort of small business or even maybe playing live/online poker to bring in some money that hedges a portion of my living expenses which allows my nestegg to compound more. A lot of FIRE folks do this by investing rental real estate, but I’m not too interested in that.

One trope about FIRE people is that they live like paupers, a la Early Retirement Extreme, and while I read that book, it is not something that resonated with me. I have never had a car payment and the max I’ve paid for a car was about $7k in 2020. My rent for a 2BR apartment in Seattle is half the price I’ve seen of some studios. Sure, it’s not the nicest or the biggest place, but why am I doing this in the first place?? I don’t really care about spending on things that make me happy though and take multiple vacations per year, buy the things I want for myself and family.

Most FIRE fundamentalists use annual spending as the benchmark here because that is the value you would be withdrawing from your investments to pay for your life. The 4% safe withdrawal rate or “25x of annual spending” comes from a paper called The Trinity Study which is worth a read since it’s only 6 pages of content including grafs.