If McConnells hands were any blacker they’d decay and fall off.

My lol $600 hit my account this morning. Just in time for me to pay my $1200/month student loan payment. Thanks for the support, government!

6 Likes

Same

Ditto

Does this mean all Trump voters should get Covid and all Biden voters should not?

Btw, it’s $600 per person, adult or child. My family of four got $2400.

1 Like

I support Bernie, so I’ll be looking forward to our 2k/ mo backdated to March.

8 Likes

Cliffs for prior EIDL or PPP applicants? Are the coffers opened anew?

Still kicking myself for not maxing out my EIDL offer.

1 Like

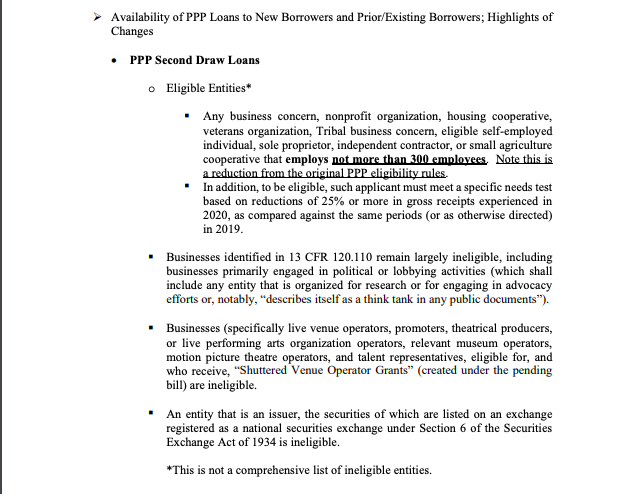

Looks like 2nd ppp (same amount) if you made 30% less than 2019 in any quarter.

Are you aware of regulations that would encourage or prohibit someone from applying for PPP if they previously were granted an EIDL (or vice versa)?

Lots of hookers. Lots of blow.

Who we kidding. A moderately priced escort and SOME blow.

3 Likes

EIDL advance used to be deducted from PPP forgiveness, that is no longer the case.

For both the EIDL and new round of PPP loans, the applicant still has to attest that the loans are necessary to support ongoing operations. That’s a trickier question for my business now than it was when the first round of PPP was rolled out. I can still make a good argument given the uncertainty of what’s coming in 2021.

1 Like

No, pretty sure you can get both, but can’t use them both for the same thing.

1 Like

Been hearing that the rule that your forgiveness is lowered by your EIDL amount might be axed

So it’s just more free money for rich people.

1 Like

It’s just another version of the audit lottery

Just take all the money. The government is so inept they won’t ever know.

4 Likes

Much appreciated. Also found this summary from the mid-size law firm Genova Burns.

Specifically to my question:

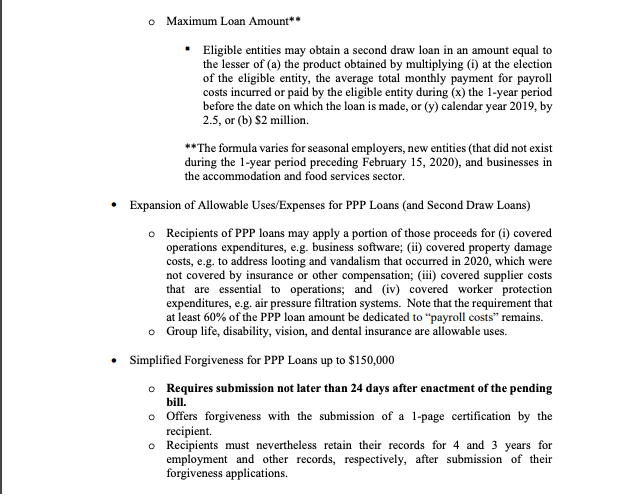

Maximum Loan Amount**

Eligible entities may obtain a second draw loan in an amount equal to

the lesser of (a) the product obtained by multiplying (i) at the election

of the eligible entity, the average total monthly payment for payroll

costs incurred or paid by the eligible entity during (x) the 1-year period

before the date on which the loan is made, or (y) calendar year 2019, by

2.5, or (b) $2 million.**The formula varies for seasonal employers, new entities (that did not exist

during the 1-year period preceding February 15, 2020), and businesses in

the accommodation and food services sector.

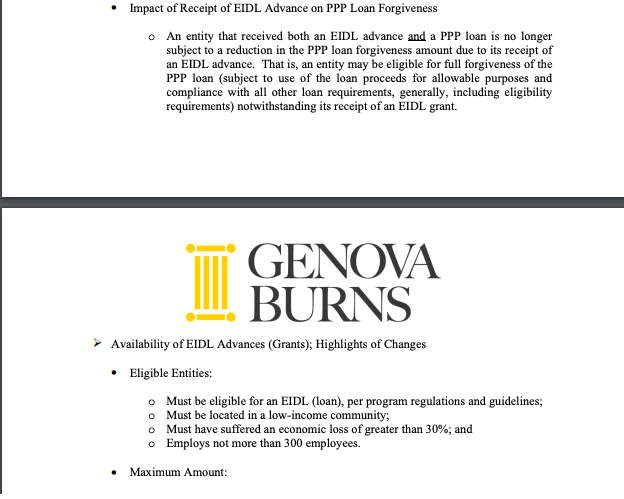

An entity that received both an EIDL advance and a PPP loan is no longer

subject to a reduction in the PPP loan forgiveness amount due to its receipt of

an EIDL advance. That is, an entity may be eligible for full forgiveness of the

PPP loan (subject to use of the loan proceeds for allowable purposes and

compliance with all other loan requirements, generally, including eligibility

requirements) notwithstanding its receipt of an EIDL grant.

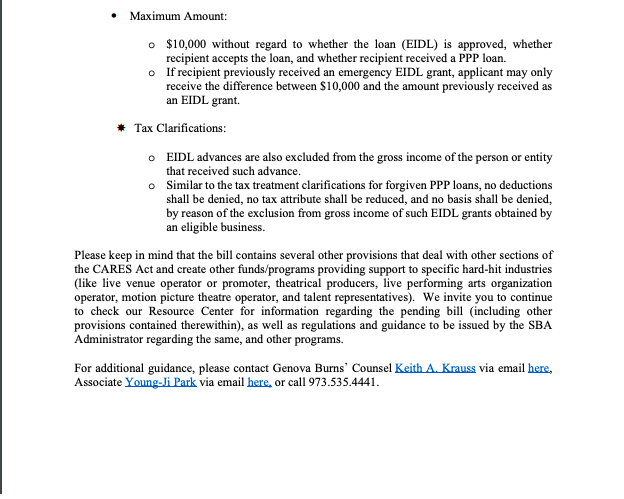

$10,000 without regard to whether the loan (EIDL) is approved, whether

recipient accepts the loan, and whether recipient received a PPP loan.o If recipient previously received an emergency EIDL grant, applicant may only

receive the difference between $10,000 and the amount previously received as

an EIDL grant.

Booo guess moms doesn’t get any stimulus because I claim her as a dependent. Not like $600 would have made much of a difference lol.

1 Like