Can confirm my dad grew up rich enough to have a meaningful trust fund and died owing me 45k after raising me in pretty extreme poverty. He was born in 1950. What was left of his trust got disbursed and didn’t even cover what I’d lent him in my late teens- early 20’s.

Absolutely an apex boomer who spent his entire life mooching (past the point of grifting often including outright fraud) off other people.

The idea that there’s going to be some huge generational wealth transfer from any but the wealthiest boomers to their millennial / gen x offspring is ignorant of the many traps that have been setup to gank middle class retirees and separate them from their nest egg before they die. Most of the money Boomers with <10M net worths have is going to evaporate before their kids ever see a penny.

Exactly. There are highly efficient businesses built exactly for this generational transition. Senior housing can run up to $10k a month, financial advisors are going to absolutely feast on boomers, they’ll leverage the shit out of their houses, etc. These are the most selfish people on earth, they’re going to spend every dime and borrow more when it’s gone, all while looking down on the kids they fucked up.

We’ll see, my parents are lower middle class but they have a small nest egg that would be super meaningful to me right now but hopefully won’t by the time I get it, which is to say hopefully they live long lives and I have more money after that long time than I do now.

Anyway they’re trying not to spend it so they can pass some on, although ironically the stuff they want to spend it on is the exact opposite of what I think they should spend it on lol… My Dad wants to do projects around the house to increase the resale value, and I want them to travel some and do fun things with some of it. I think if he does the projects he’ll basically end up lighting the money on fire because he’ll spend more on it than the resale value will go up.

I do think if nothing else there will be a transfer of wealth from homes being passed on, but most of them will need extensive remodeling to update them and make them desirable for Millennials and Gen Z.

My current thought is that sometime next year there will be a bunch of listings like that for 3-4 bedroom houses in my area that are like:

$600K → $570K → $550K → $515K → $495K → $475K

And pre-COVID they were probably like $400K houses.

And I intend to keep offering like $350-375K on houses that have been sitting on the market for 60+ days until someone gives up and takes it. Because while it’ll be a lowball offer and piss most of them off, it probably won’t be an unreasonable offer in the market conditions, and the monthly payment on a $375K home with 20% down at 8% = the monthly payment on a home at $575K, 20% down, 3% interest.

We’ll see where the exact numbers fall, but if houses are sitting on the market for long stretches of time, there should be opportunities to make a ton of low offers and get one accepted eventually.

My other thought is to buy an empty lot when prices crash and rates are high, sit on it, and then finance the new home build in a year or two when the rates come back down.

I’d advise not getting too aggressive in trying to buy at the bottom/bottom. Never know when the Fed is going to flip the switch back on and you’ll miss your chance.

Only scenario I see your plan working is after the Fed has tried, and failed, to pump the economy back up and so we are kind of permanently fucked. Possible that happens but not advisable to treat that as the base case scenario, imo, if you really want to buy a house.

Yeah I agree with you somewhat, one thing that keeps it simple for me right now is that I really don’t have the money for a down payment on anything I’d be interested in buying. Like, I could, but I’d have to move down from 5/10/20 and 10/25 to mostly 2/5, because most 5/10 near me runs with a straddle. It’s not worth cutting my earning power that much as opposed to being patient, so I’m hoping the timing kind of works in my favor.

If I’m going to buy at what I view as a bad price, the home needs to be nice enough that we’d be happy in it for ~10 years I think, which means being in a good/safe area and at least having space for an office and one extra bedroom in case we have kids in that timespan. Right now I can’t put that kind of down payment together and afford the monthly payment thanks to the rates. Before the problem was the down payment due to the total price.

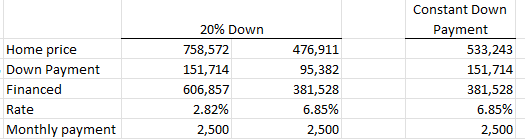

I agree this is a pretty crazy change, but I think it overstates the case a little bit. You needed a $151k down payment to be able to afford that $758k house, now you only need a $95k down payment to afford the $476k house. If you keep the $151k down payment constant, I think this analysis would have you being able to afford a $533k house.

I have a habit of objecting to unimportant details of an argument even when I completely agree with the thrust of the argument. My wife finds it a delightful trait.

Purely anecdotal observation: I was looking for a new place to live about a year ago and briefly looked into SFH/townhouses for rent, the market was nearly nonexistent though. Checked again today and my area is flooded with listings. I’m assuming (hoping) that means everyone who still needs to move but doesn’t want to give up their sub-3% mortgages are turning to the rental market, which might keep rent prices suppressed (hoping again), which might trigger more investment property sales or at least pump the brakes on further investment buying. No idea if the statistics actually support even the first postulate though, I’m just trying to console myself in my apartment.

Yeah, but this also needs to take into consideration the appreciation of home prices, since you are getting less bang for your buck as well now than before.

Sure, but not everyone is going to make the decision to throw all that money at the down payment. It would make a lot of sense to do that because of the interest rates.

I think the other thing both these analysis don’t explicitly point out is that $758k home in early 2021 is now a ~$1M home, whereas the $533k home now was probably a lower $400s home in early 2021. So the house is still a significant different.