What do you all like for index ETFs? Once we hit a 20% drop from ATH, my Roth will be approximately 65% in the S&P (half in VOO and half in the Schwab S&P mutual fund) and 35% in QQQ.

I now have about 2.6 times the total in my Roth in my newly created SEP-IRA in cash. I plan to work it in as this drop happens, and if the markets bounce back and we move past coronavirus and things return to normal, I’ll just cost-average it in over a longer period of time. It’s more than I’m comfortable popping in over a short period of time under normal conditions, but I’m thrilled to do it at a big discount.

Current plan is to put it in in even amounts every additional 2% off ATH. I was thinking of putting in smaller pieces earlier on and bigger pieces as it drops, but I think that’s just a form of trying to time the bottom and probably not good.

The plan is to put it in different index funds or ETFs, and obviously I can’t go too wrong there since I’ll be taking broad exposure to the markets, but should I keep it all with the S&P and QQQ and either keep or adjust that roughly 2-to-1 ratio, or should I be looking for a DJIA ETF, Nasdaq ETF, Russell ETF, etc?

I’m in the process of reading The Intelligent Investor, and not looking to do any playing around picking stocks or trying to outsmart the market in that regard until I’m done, at which point I might give myself 1-5% of my portfolio as a “bankroll” to fool around with on that and see how I do and whether I enjoy it. Even if it’s a little -EV in a vacuum, if it keeps me more focused on getting money into the markets over the long run and I keep it in the 1-5% range, it’s probably +EV overall just by getting me to invest more.

I’ve goofed around in the past, so now my rollover IRA is some weird blend of various indices, but there’s no real benefit to trying to allocate between the Dow/S&P 500/Nasdaq. IMO

Not only are these two beliefs not at odds with each other, they’re perfectly intertwined. It’s not that you must hold through downswings, it’s that you might as well because all other choices are likely to turn out worse.

For tax advantaged accounts I go with something like 30% VTI, 25% VBR, 30% VXUS and 15% VNQ. Foreign and reit because they’re a bit less correlated to the US market. VBR because I like to gambol. For taxable accounts 60% VTI 40% VBR.

Tax efficiency. REITs pay high dividends and they are taxed as regular income. Nearly 100% of the dividends in VBR are qualified dividends so are taxed at the long term capital gains rate. VXUS dividends are mostly qualified but like a third are ordinary and will be taxed at your marginal income tax rate.

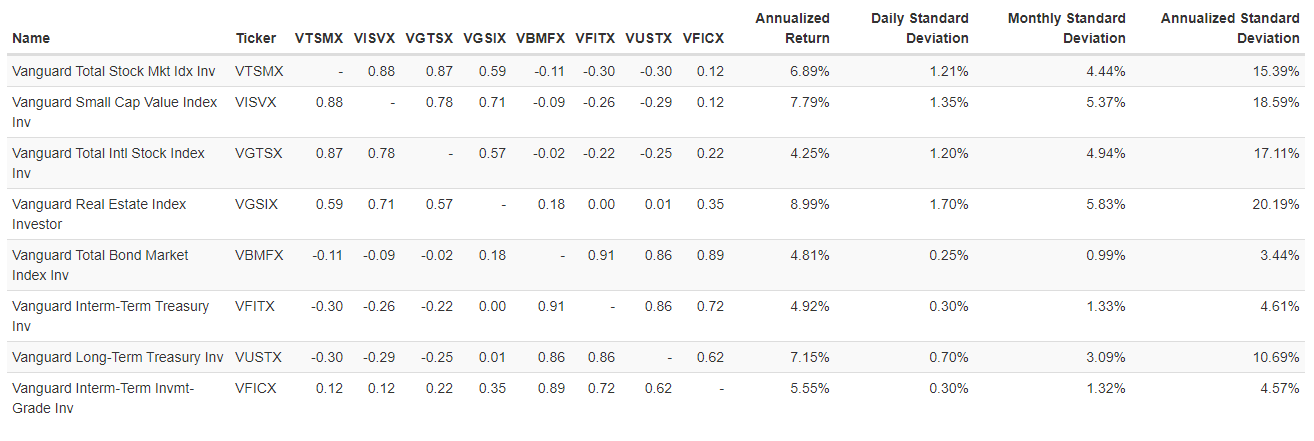

Here’s some correlations between the different assets I listed above and a few bond funds. 1 is perfect correlation, 0 is uncorrelated, -1 is perfectly anti correlated. The more uncorrelated assets you have in your portfolio, the less variance you will get.

So look at the first column, which is the correlation of various assets to the asset that spidercrab recommended. Small cap value index and international index are both highly correlated to the total market, so there’s not much value in diversifying there. REITS are significantly less correlated, so there’s some diversification value there, which is why I overweight them in my portfolio. That’s particularly valuable because their returns are historically pretty much what the total market returns have been. I overweight small cap value because the returns on that sort of fund have been higher than the total market (volatility higher too, which makes sense).

Then on to the real smoother of volatility, bonds. Bonds are anti-correlated with stocks, which is the whole point of including them in portfolios despite their lower expected returns. The total bond market index is slightly anti-correlated, intermediate term treasuries are more strongly anti-correlated, and long term treasuries are even more uncorrelated than that. Then comes the most interesting, the last row, investment grade corporate bonds. These are actually positively correlated with equities! Bad! And that’s the reason why the total bond market funds are less anti-correlated with equities, because the total bond market funds contain about 35% corporate bonds. Moral of the story – if you can buy just treasury bond funds to diversify your portfolio in your 401k, do that.

I’m absolutely not missing the point of that graph. The point is just profoundly irrelevant.

You may be missing the point of my post though.

Half of this thread this week is insisting no one can time the market, or that if you ‘opportunistically step in and out of the market’ that the market is equally likely to rise or fall, with a small bias towards rising to the tune of something like .04/365 or +.0001095 per day.

The fact that the distribution of days with increases has a large proportion of its value concentrated in a few very big gaining days is useless information, because the distribution of big losing days is going to turn out to be identical.

I can create an equally stupid graph showing that investors who ‘miss’ the 60 biggest losing days in the last 20 year period actually showed enormous profit compared to people who were in the market for the entire period, and use it to advertise my brokerage firm for people who like even more money.

That graph is manipulative because it leaves out the only pertinent information, that being someone who exits the market only on the best days is as equally impossible a strategy as being someone who exits it only on the worst.

“After 11 years, 13% annualized earnings growth and 16% annualized trough-to-peak appreciation, we believe the S&P 500 bull market will soon end,” Goldman Sachs equity strategists wrote in a report to clients Wednesday."

People aren’t saying no one can time the market. Individuals are saying “I don’t think I can time the market so I’m going to commit to not trying.” And if you think you can time the market then wtf are you doing in this thread yelling at people who have no interest in trying to do so, get out there and start making moves. Lot of FREE MONEY out there.

Did you even read my post? I said it was cherry picked and no one goes 100% S&P to 100% cash and back.

The entire point is to just pick a plan you can stick with and do that unless your goals or financial situation change drastically. The information simply illustrated that missing the big days can hose you, and often those come after large drops. It’s not good to time the top or bottom of the market and due to the proximity of the huge swings you’re likely to miss a mixture of big up and big down days. No one is only going to miss the 10 or 30 or 60 best or worst days.

I may agree with your conclusions, but still argue that the specific evidence you present is bad evidence that doesn’t say anything at all.

As Zara said I’m arguing completely given the premise that predicting short-term market moves is impossible, which this thread is still somewhat split on

The reason tons of people lose when trying to time the market is that they sell low after a cluster of big drops, (because they got scared), and then they wait too long to get back in and miss the clusters of big gains.

The other really common situation is people selling near all time market highs because there is no way the market can keep going up. And then it keeps going up for years and they never get back in. These people tend to miss the clusters of big drops, and sometimes catch the clusters of big gains, but miss so much of the long steady grind up that they still lose out.

If people just randomly moved in and out then I would agree more strongly with your point. (And I do agree that the chart is bad and you could just as easily make a similar chart about missing the big losing days.)

If a bad market timing strategy could be determined, a good one could do the opposite and make infinite money.

Buy and hold works because the market generally goes up and being out of it is wasted opportunity. Also trade costs of moving in and out - but those are often negligible these days.