Is 30% in international stocks foolish for my 401k? Looking to increase my risk a bit. I’m 30 years from retirement.

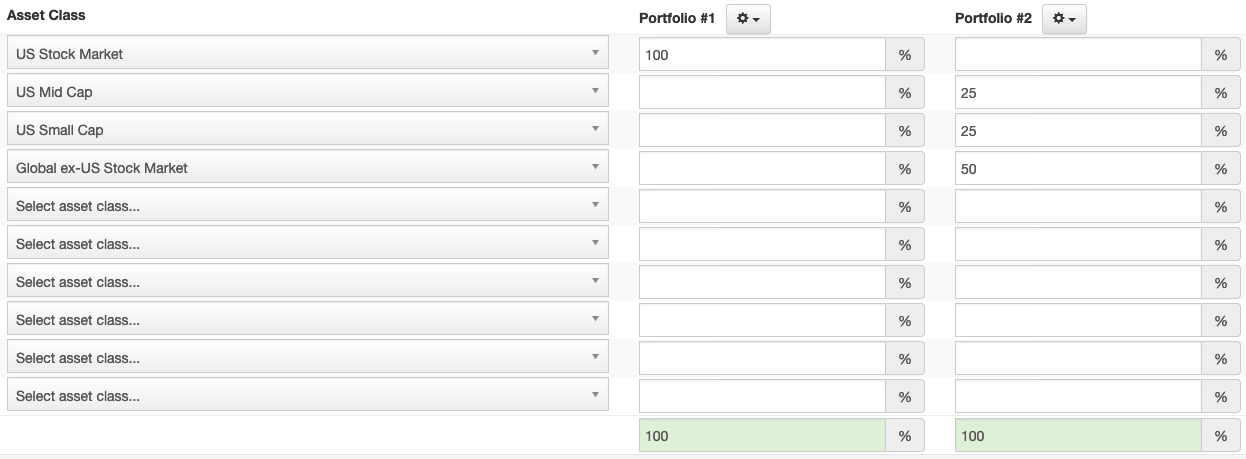

Edit: adjusting to 25% mid cap US. 25% small cap US and 50% international stock. Unless someone tells me that’s a bad idea.

Is 30% in international stocks foolish for my 401k? Looking to increase my risk a bit. I’m 30 years from retirement.

Edit: adjusting to 25% mid cap US. 25% small cap US and 50% international stock. Unless someone tells me that’s a bad idea.

What is your overall asset mix?

You will get a lot of different advice on that. Personally about 30 percent of my equities are held in international. I’m hopefully between 5 and 10 years out from retirement.

I personally like international exposure and use Vanguard Life Strategy funds to obtain it. International has significantly under performed in the last 10 years. I see that as an opportunity, others see the opposite.

25% mid cap US. 25% small cap US and 50% international stock. All Vanguard with low expense ratios.

I think its fine. It’s helpful to articulate what a 30% allocation actually means in terms of investment choice. If a US investor allocates 30% of their equity portfolio that is an overweight to US equity. Is that the intention?

On the other hand if someone has an asset mix of 70% US bonds and 30% international equity there’s a lot more going on. There is choice to be conservative and a choice to massively overweight equity to international. This would be harder to justify.

This all seems fine. What’s the concern? Your risk and return profile won’t change that much shifting the international weight a bit.

Not really a concern. It’s just a topic I need to be more knowledgeable about. Wanted a sanity check before I adjust. Thank you.

I think you will find a lot of disagreement with that statement. A lot of people feel that US equity already has a ton of international exposure. I feel like 30% international equities (strictly from my equity allocation, not 30% of investments) gives me a fairly even weight.

This is true. It had long been a habit to associate the country if a company with the country where it is principally registered as a business, but globalization reduces the meaning of that.

We gonna need to dig up the “You know what’s cool? Losing 2000 points” meme again?

My DIS puts are looking better by the minute.

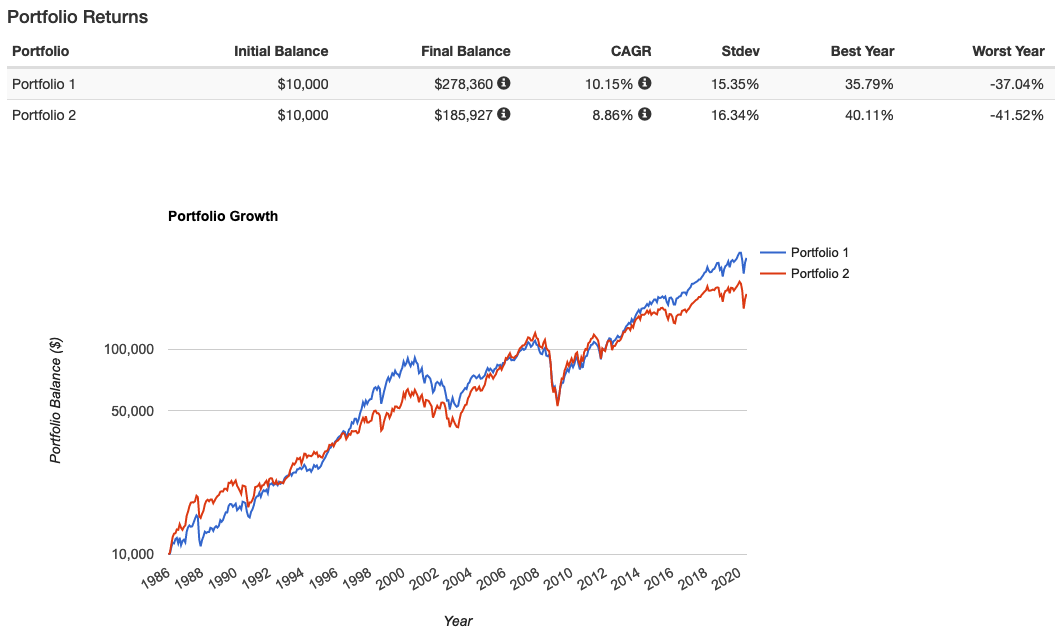

portfoliovisualizer.com has a “backtest asset allocation” feature that allows you to specify two or more general portfolios and generates a detailed report.

This example clarifies Riverman’s point about intl underperforming over the past 10 years, since the two portfolios were basically even coming out of the bottom of the financial crisis.

The real question is why are you completely ignoring US Large cap?

Also, I personally think developed markets ex-US aren’t great. If you look at the Vanguard total international index fund 18% of it is allocated to Japan. I’m not a huge fan of that at all considering how stagnant their markets have been and what their demographics look like. Emerging markets are a lot riskier but certainly should provide more upside.

Well they are riskier because they may not, correct? I mean it’s not just volatility that’s assumed, I think it’s real risk.

It could be good to guess that the headlines are just pulling ideas out of their ass on why the market is dropping and the market could be tanking for a completely different reason.

The headlines don’t seem to have a clue either when the market is shooting up for no apparent reason.

Being half in cash kinda sucks. The last few days I couldn’t stop mentally adding the amount I would be up if I was all in. Then today I’m still losing a good amount, which is never fun.

Being in any allocation other than the long-term allocation that you’ve strategically decided is risk and reward optimal for your situation will always suck for exactly that reason. You can’t win. There’s always a better decision you could have made. And if you shove all in on your long term allocation and stop making decisions, you can’t lose. You can’t lose because you can’t make a wrong decision because you’re not making any decisions.

I understand the concept, and 99% of the time that’s my strategy. But the bottom line is I’m up 10% since my previous high in Feb, and about 40% from my low in March/April. If I was just buy and hold I’d still be down from Feb.

I was able to do something similar in 2008, which you were there for.

Probably just dumb luck, and I definitely don’t jump in and out lightly - pretty much black swan events only, but I guess I’m going to need to get burned by underperforming buy and hold before I learn my lesson.

I just can’t see a ton of upside to stonks or sectors that are at or near all time highs, while covid is still raging and most of the US is in denial. Not enough to feel comfortable being 100% in stonks right now.

What’s my asset allocation supposed to be right now anyway on money I can’t touch for 7.5 years?

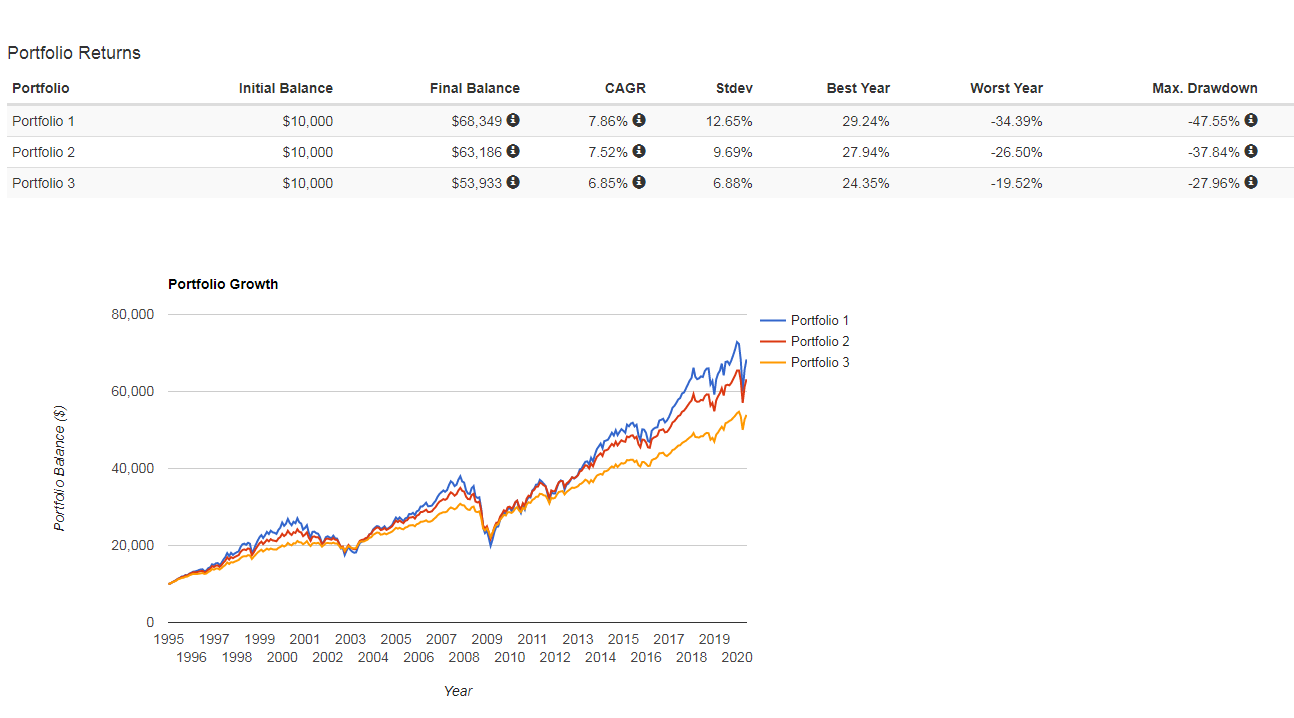

Whatever you’re comfortable with. I think that conventional wisdom is 60/40 stock/bonds or 50/50 stock bonds. Below are the Vanguard lifecycle funds, 80/20 to 40/60. Which dip in 2009 looks acceptable to you for that money? That’s the one you should pick.

If it were me I’d have it 100% stonks in your situation but I’m a degenerate. Hell I have my emergency fund in the 40/60 vanguard lifecycle fund.