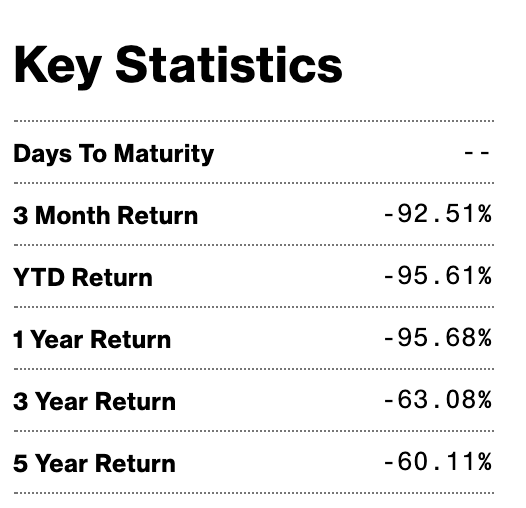

Lol UCO - it’s gone from -2% to this in less than an hour. Meanwhile Exxon is still negative and has barely moved.

Solid track record though:

Lol UCO - it’s gone from -2% to this in less than an hour. Meanwhile Exxon is still negative and has barely moved.

Solid track record though:

UCO - up 8% in 2 days so far. Time to move my whole portfolio to it and go by my own island somewhere.

TGT up 3%, close to all time record.

stonks

Either some combo of VBTLX, VTSAX, and VTIAX (based on how aggressive you want to be as well as your opinion on international versus US stocks) OR one of the target date funds.

Those are legit fantastic options, your employer is doing a good job.

When I started at the firm they used a financial advisor that was just killing them. He had us in funds that were charging enormous fees.

I spearheaded the campaign to fire him and get us into something that had vanguard funds. I had to present the firm’s owners with a spreadsheet of how much money they missed out on by paying those fees. They acted pretty quickly after that.

Damn dude, good work.

Think of the poor advisors kids, though!

Were you invested in the stock market in the latest downturn? If so, what was your stock/bond ratio and how did you handle the downturn emotionally?

All of their funds are fine, but no one can answer your “What should I buy?” without knowing a lot more about your risk tolerance, years until retirement, current assets, etc.

Well that’s why I said some combo of the big 3, or a target date fund. The big 3 would have different proportions depending on how aggressive he wants to be, (i.e. - risk tolerance, and years to retirement will play into that), or the appropriate target date fund.

If you want a set-it-and-forget-it solution with low fees and even lower brain power and decision fatigue involved with it, then it’s Vanguard target date fund. That’s never a substantial mistake. You can just keep buying that til your retirement date, and that’s always a good strategy. If you want to geek out a bit and rebalance and fidget and such, then yeah, mix it up with Jbro’s set depending on your risk tolerance.

Not so sure about this for 401k retirement savings. Almost across the board, given that you are in an employer sponsored pension plan the simple answer (contribute at least as much as needed to attract the full company match, invest it in the target date fund corresponding to the year you turn 65) is going to be super close to optimal for most people. I think considerations around risk tolerance and personal circumstances become much more meaningful when you’re getting ready to retire, or if you’re talking about extra discretionary saving outside the pension plan.

I generally hold more bonds in tax deferred accounts but in this interest rate environment it doesn’t really matter as stock dividends are roughly equal to bond yields.

What’s the best “risk free” (guaranteed return, obviously still some risk the US or AAA bonds default or w/e) % these days? 2%?

About 1.5%

Woo hoo. I think putting it all in bullets may be a better option. Mostly as trading chips in road warrior times. I feel like trading gold is just inviting someone to attack, figuring rightly that you have a lot more gold somewhere.

Seems like any awful news is met by a 500 point drop over a day or 2 before rallying and then some over the following few days.

Stock futures are basically flat with widespread civil unrest across the country. STONKS