Since COVID is coming back I’ll give this thread a bump.

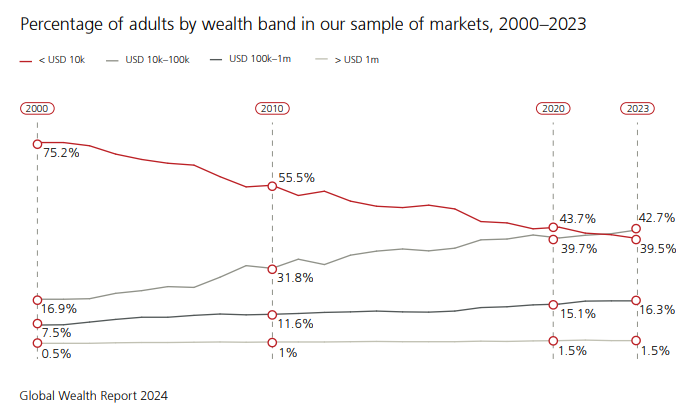

From UBS Global Wealth Report. I’m thinking this is may be more of a function of home values than anything else really, but I thought it was interesting to see the change in cohort size swap from the lowest wealth category to the 2nd lowest.

This is an interesting graph, but it’s hard to believe that the shift from <10k wealth to 10-100k wealth is driven by home prices when those groups are least likely to be homeowners. (Or maybe your homeowner comment referred to the two richest bands at the bottom and I misunderstood.)

This is a global wealth report, so I’d expect that the biggest factor for the lowest $ categories is just the increasing output of non-US countries. Inflation is an interesting thing to think about. On one hand, of course inflation matters given the nominal dollar amounts (even though it’s a little tricky to think about how inflation affects the large group of people in that lowest $ group with no assets to speak of).

between $2.9 and $6.6m in retirement, other investments, and cash combined

between $860k and $1.7 sitting in cash or equivalent

Her largest holding is Target Date 2030 fund with $250k-$500k

S&P 500 and large-cap growth funds, each worth between $100k-$250k

She defined benefit plan from city of San Francisco valued between $250k-500k (not clear if that is per year?)

Emhoff has a lot of ETFs “offered by Vanguard, BlackRock , and Charles Schwab . His largest holdings were the iShares Core MSCI EAFE ETF and the iShares Broad USD Investment Grade Corporate Bond ETF, each worth between $250,001 and $500,000. He had another $402,000 to $1.1 million in iShares and Vanguard funds invested primarily in U.S. stocks.”

It’s probably the total value. In a typical public sector plan, to get a pension of $250,000 per year you’d have to work there for 20 to 30 years and retire with a final salary of about $300,000. Harris only worked for the city of SF for 7 years or so according to her Wikipedia page, so she probably has a pension that is more like, I don’t know, $30,000 a year. That would map to a value in the $250,000 to $500,000 range on an actuarial basis.

Haven’t gone through the thread but a couple reactions

taxes seem too high. How do they get to an average tax rate of 43%? Maybe they are including taxes on investment income that isn’t part of the W2 income that they start with

having a full time nanny plus daycare is an extravagance. They can afford it, but they don’t get to complain about it

Re #1, the majority of their income is being taxed at 32-37% federal, plus 6-7% state + 4%-ish NYC. 43% doesn’t seem unreasonable. Maybe they’re also including stuff like FICA.

The post strikes me as a strained attempt to frame it as “boy everything gets eaten up after expenses and taxes!” when they are throwing a quarter million dollars a year into investments. That’s partly due to OP talking about how frugal they are with their nanny, FT daycare, and $50K vacations. But also partly due to how the software shows savings/investments. If it showed it in-line with the expenses, it would look different.

I plugged in $1,000,000 to this tax calculator, and it gave total federal, state and city taxes of $422k

However, the part of their income they contribute to 401k and HSA isn’t taxable, and they may have some other deductions that push things down further

On the other hand, the tax calculator doesn’t include FICA. The Social Security part of that goes away after 160k for each spouse, but the Medicare part applies to the full amount of income. So maybe it ends up evening out.

I’m always surprised that the thing that usually gets called out on these is the “high” vacation budget. I spend ~8% of gross income on vacation, which is significantly more than this couple. Four economy comfort tickets to Europe plus a nice hotel for 7 nights is going to be $20k alone.

Just look at the per person prices at adventures by Disney. You are going to spend that entire $50k budget on one trip.

I’d also be completely shocked if a family of four in NYC is only spending $25/yr on food. That sounds borderline impossibly low unless the nanny is doing the grocery shopping and cooking.

I always love these “once I account for consumption, spending and charity, I have nothing left” posts. But the best part of this is that there is no charity! Since the tax stuff is almost certainly a lie, you would think they would pop some in there before posting. Atrocious.