It’s a less than 5 minute process to open a new account–a Performance 360 Savings Account–and transfer assets. The information is already populated, so it’s trivial to do.

But the fact that I had to do it at all, and that I wouldn’t have even known about it, is incredibly scam-like.

If you have or had an open 360 Performance Savings, 360 Savings, 360 Money Market, Savings Now or Confidence Savings account as a primary or secondary account holder with Capital One on or after January 1, 2019, you will be ineligible for the bonus. If your account is in default, closed or suspended, or otherwise not in good standing, you will not receive the bonus.

If it’s this promo, $10K gets a $100 bonus. $100K gets you $1000.

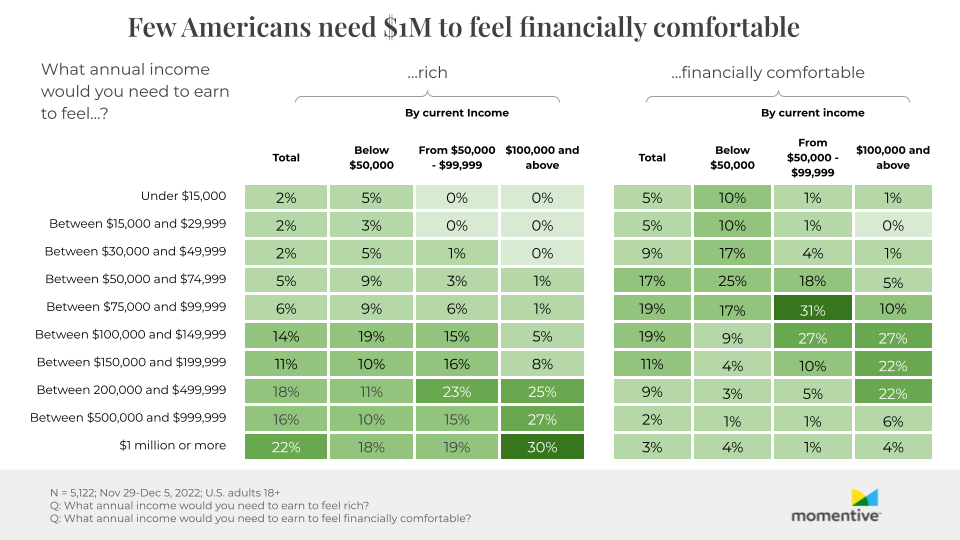

Surveys of Americans about what they think they need financially to achieve X are about as useful as asking my dog how how to design a nuclear reactor. The median American is a fucking moron with money.

Obviously Jerome Powell knows way more than me but it seems like they could go ahead and chill the fuck out with the rate hikes right about now. Prices have stabilized and are dropping in huge sectors like car prices and rent. He’s already crushed the housing market to shit, people are loading up on credit card debt, the only place inflation is still happening is wages, which like, fine?

2007 Toyota Highlander, parked in driveway. A tree limb falls on it and breaks the front windshield and puts a few cosmetic dents in the roof, the hood, and the door. I don’t think the dents will affect driving or safety at all.

Since the car is so old and was a little beat up to begin with, insurance declares it a total loss, because multiple panels need to be replaced. Their settlement offer is around $6,900. So I can give them the car and take that amount.

Apparently I can also keep the car, fix the windshield myself, and keep driving it. In that case I would get the $6,900 minus salvage value, which they say is $2,000, so I get a check for $4,900 and keep the car. That $2000 is probably too high but whatever.

If I think I can drive the car for another 2-3 years, I should probably keep it, right? I give up $2,000 in salvage value, and $300 to repair the windshield myself, but I get to postpone buying a new car for a couple years (if I’m lucky).

If it matters I could buy a new car without financing. I just would rather run the old car down to nothing. Cuz I’m cheap and like having a beater car.

Apparently they can declare it a total loss when it’s only 65-75% of the total value, this varies by state. In my case the estimate was about 70% of the value.

There were multiple panels dented, each panel has to be replaced I guess. $1,500 plus per panel?

Ironically the dents were not around the windshield. I think the limb fell in two pieces, one hit the windshield directly and the other dented above and below the rear passenger door. Slightly worried about the seal of the rear passenger door, but the front windshield has no dents around the seal.