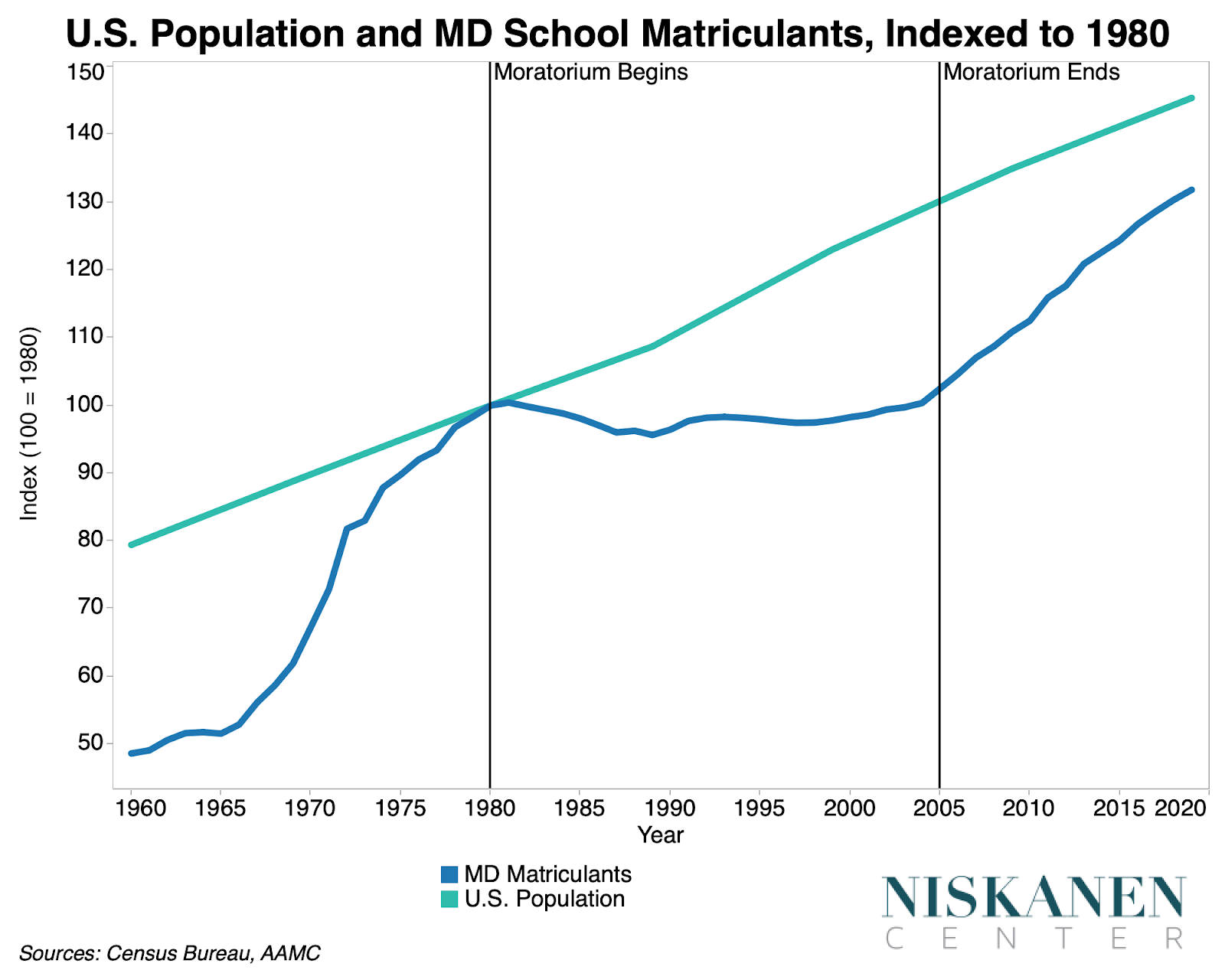

That’s not quite right. The reason for no new medical schools wasn’t the cap on residencies. The cap on residencies still exists but medical school enrollment has gone up since 2004 or so. LCME stopped adding new MD programs because there was a concern about too many doctors around the 1980s. The was 15-20 years without a single new MD program in the nation. Those things go hand in hand. It happened because that’s what physicians wanted.

Currently, having too many newly graduated doctors not match into residency is a big problem. If the cap was the issue, you wouldn’t have expected to see the med school growth that we’ve seen.

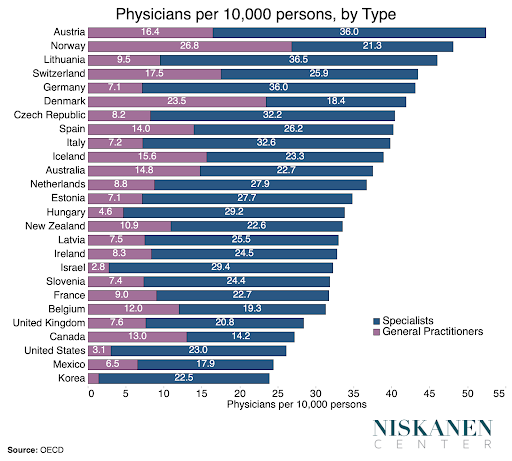

I also don’t buy that 12% of US physicians are ‘general practitioners’. I suspect some definition game is the reason for that, same for Israel/Korea. There’s definitely a shortage of primary care physicians, but that group can be Family Medicine, Internal Medicine, Pediatric, or even OBGYN trained, and I’m guessing a fair number of those to IM/Peds/OBGYN are listed as specialists. I guess that’s getting pedantic because there’s definitely a shortage.

The shortage of primary care physicians isn’t lack of medical students or residencies, it’s that they pay shit compared to specialties. I get paid roughly 2x-3x what a typical pcp gets paid for 40 hours of clinical work per week. In 2020 according to the NRMP, there was 0.3 US MD applicants for every open family medicine position.

There’s lots of reasons for this, but a big part of it is the pay structure of medicare/medicaid. Private insurers obviously set their own prices but those standards are definitely followed.

You’re better equipped to talk about some of the details than I am, and I might have mis-summarized the post. This is the original story that Matty G cites in his post, and it doesn’t seem inconsistent with your view:

Not sure that doctors per capita is a meaningful metric. Note that half the people in the US can’t afford to get a checkup regardless, take those folks out of the calculation and we would be close to the top of that ranking.

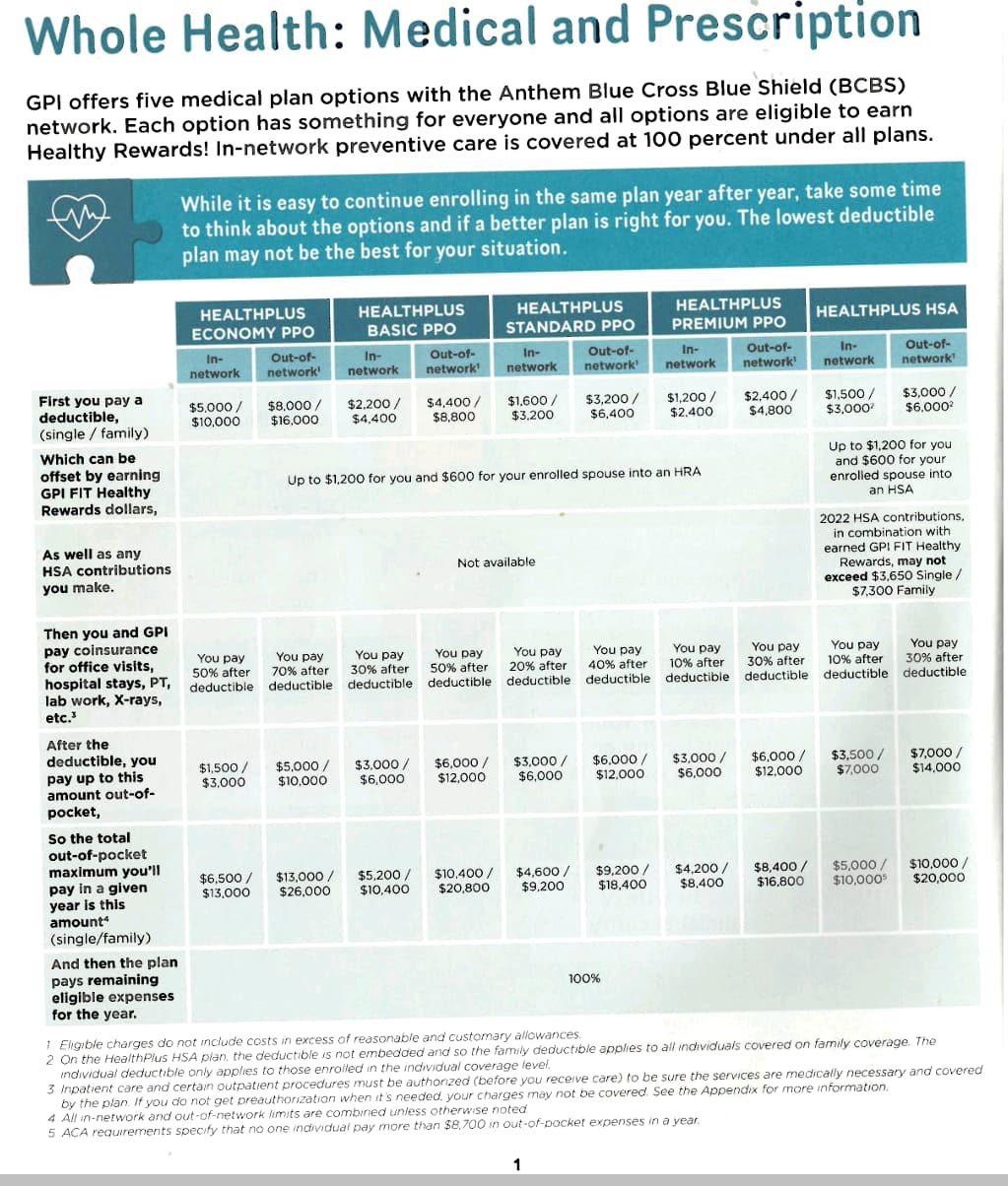

How do you guys decide which health insurance plan to choose, if given several options? Family of 4, with 2 kids <5. We don’t normally rack up awhile lot in the way of healthcare costs, but kids are a wild card. I think the only times we’ve hit our deductible in the past was the 2 kids being born. I kind of lean towards the cheapest plan, but my wife wants to go the opposite route.

No kids here, but the HSA plan seems very appealing to me if you expect costs to be low, and particularly if you can afford to pay those wild card expenses out of pocket. $1800 free from your employer (you probably have to do a bunch of activities and quizzes online and stuff) plus the tax benefit if you max out the HSA with your own contributions. Divide that by sum by 12 and you’ve made up a lot of the difference in premiums between the cheapest and most expensive.

Plus, if those wild card big expenses do arise, the HSA deductible is almost the lowest available, which is surprising considering it’s a “high deductible” health plan. And then after the deductible, coinsurance is only 10%.

And if you don’t need to touch the actual HSA dollar you can invest and let them grow tax free.

That’s how I’d look at it but don’t personally know your family’s situation.

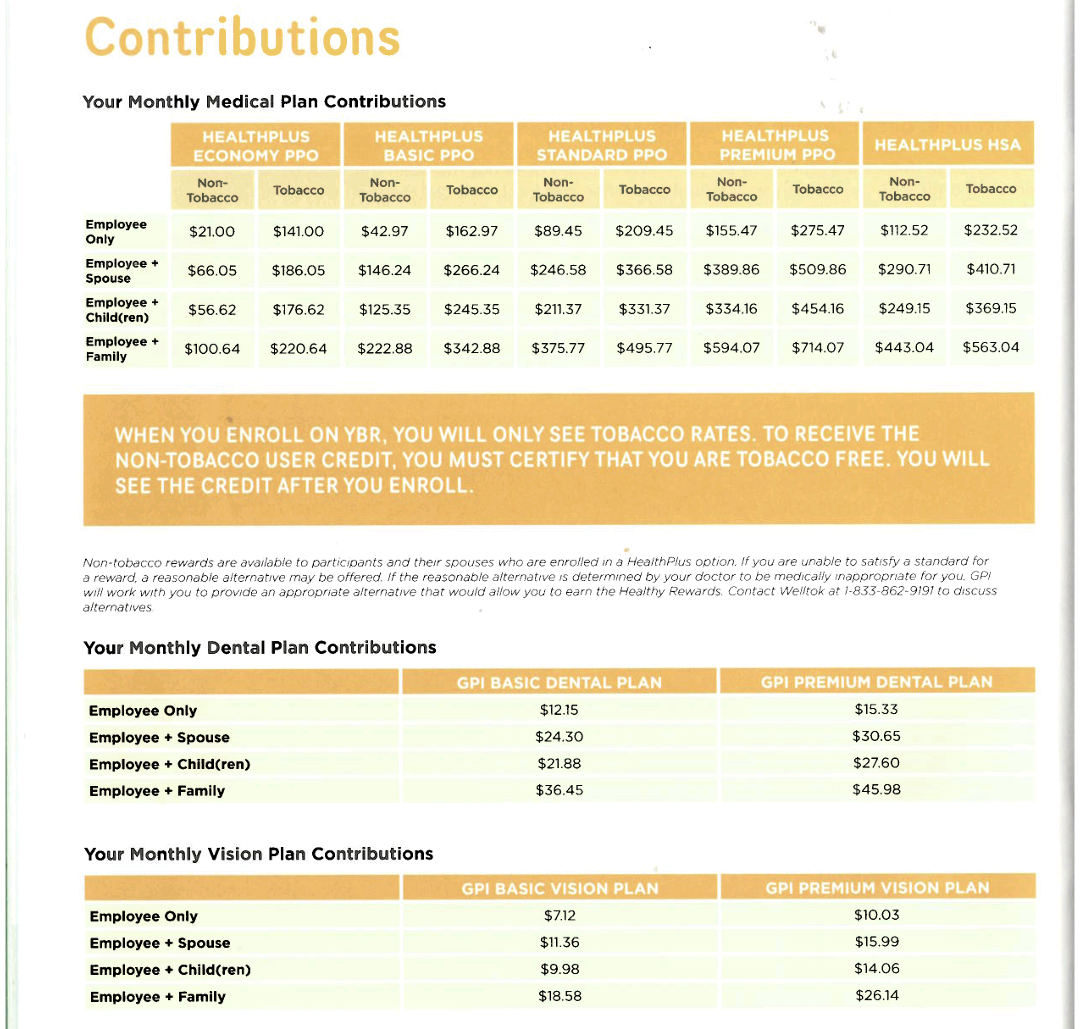

Edit: just realized you get those free company $$ in all the other plans. Just in an HRA. Which I don’t know much about. So that maybe makes my HSA plan calculus not as appealing.

I have some of the same thoughts as you. Torn between hsa plan and cheapest plan.

HRAs are absolutely obnoxious, stupid, corrupt bullshit compared to HSAs. Similar concept but you choose at the beginning of the year how much to contribute. And then at the end if the year, however much you didn’t spend, your employer gets to keep. Not just what they contributed, they get to also keep what you contributed. And you can’t change your contributions mid year.

We already had one disaster a few years back. Wife starts a new job in October or November. Tells her company to contribute $50/month (I don’t remember the exact number) to HRA/FSA. And then the company matched. At the end of December I look to see how much we have to spend or lose. And it’s like $1200. Instead of taking $50/month for like 2-3 months, they took$50x12months=$600 and then took that out of her check over 2-3 months. She didn’t pay attention/notice. So we had to spend $1200+ on dumb shit we didn’t need. Mostly a lifetime supply of sunscreen.

My quick googling earlier indicated that unlike FSA, HRA isn’t use it or lose it by calendar year. It is, however, tied to your employer, so if you leave you lose it. Or wind up with a lifetime supply of sunscreen.

You can work out the expected costs and often show that they’re better when you’re in a high deductible plan. The problem is at the margins, when you’re making decisions about whether to treat something or to go to the doctor or not. With a high-deductible plan, you’re often in a position where you’re explicitly asking yourself, “Is it really worth $250 or whatever to go to the doctor for this thing that obviously isn’t an emergency?” It’s fine if you respond to that question with, “Of course I shouldn’t be reluctant to go to the doctor just because I’d pay for it now, rather than prepaying it (via insurance). I took this into account when I chose this plan.”

But I don’t think most people operate like that. I wouldn’t, and we have friends that went through exactly this process - the husband convinced the wife to choose a high-deductible plan (based on the very easily-explained calculations that it would likely be cheaper). But then when their daughter faced a non-emergency medical issue, he was reluctant to take her to the doctor (or emergency room? I don’t remember), because it would incur a large incremental cost. I mean, that’s supposed to be one of the benefits of universal health care - that you don’t have to constantly evaluate the financial cost/benefit of getting medical treatment. You just go when you need it.

It’s why I always liked the idea of all-inclusive vacations more than other people. I can compare the cost of an all-inclusive resort to a pay-as-you-go resort and conclude that the pay-as-you-go resort is likely to be cheaper. But I know myself, and if I choose that pay-as-you-go option, I’m going to make exactly the same cost/benefit decisions at dinner that I do every day. I’m going to get chicken rather than steak because the steak isn’t worth an extra $40. But I like steak more! And if I had paid for the all-inclusive, I’d be happily scarfing down steak and shrimp and margaritas, rather than worrying that one more appetizer would keep my kid from going to college.

Get high-deductible plan one year, try not to go. Get low deductible plan the next year, try to get all your health shit out of the way.

If you think you might quit and not go immediately to another corporate job, get the lowest premium possible (including company match). Because you’re stuck with that for COBRA for 18 months. Or at least you used to be. Maybe you can switch to ACA now.

Totally agree. It is the aspect I hate about HDHP also. It essentially disincentivizes going to the doctor. And I have probably been guilty of leaning towards not going at times because of it.

I have the opposite take. Once you have enough money in the HSA you’re incentivized to go TO the doctor so you have the receipt to pull the money out before you’re a million years old at a (marginal rate + FICA) percent discount.

Good lord. It’s hard to imagine that people prefer this system.

Your plan options suck so I don’t have any advice. Our insurance is about $300 to insure myself, my wife, and our daughter (though the price wouldn’t go up if we had more kids), and our deductibles are $250/pp $750/family.