The hard part of convincing people to support UHC is that healthy people don’t actually know what their healthcare plan is and what their provider is capable of doing within the law until they need to use it. Only then do they find out how fucked they are.

It’s incredibly difficult to understate how much better an even poorly funded UHC program is compared to what America has.

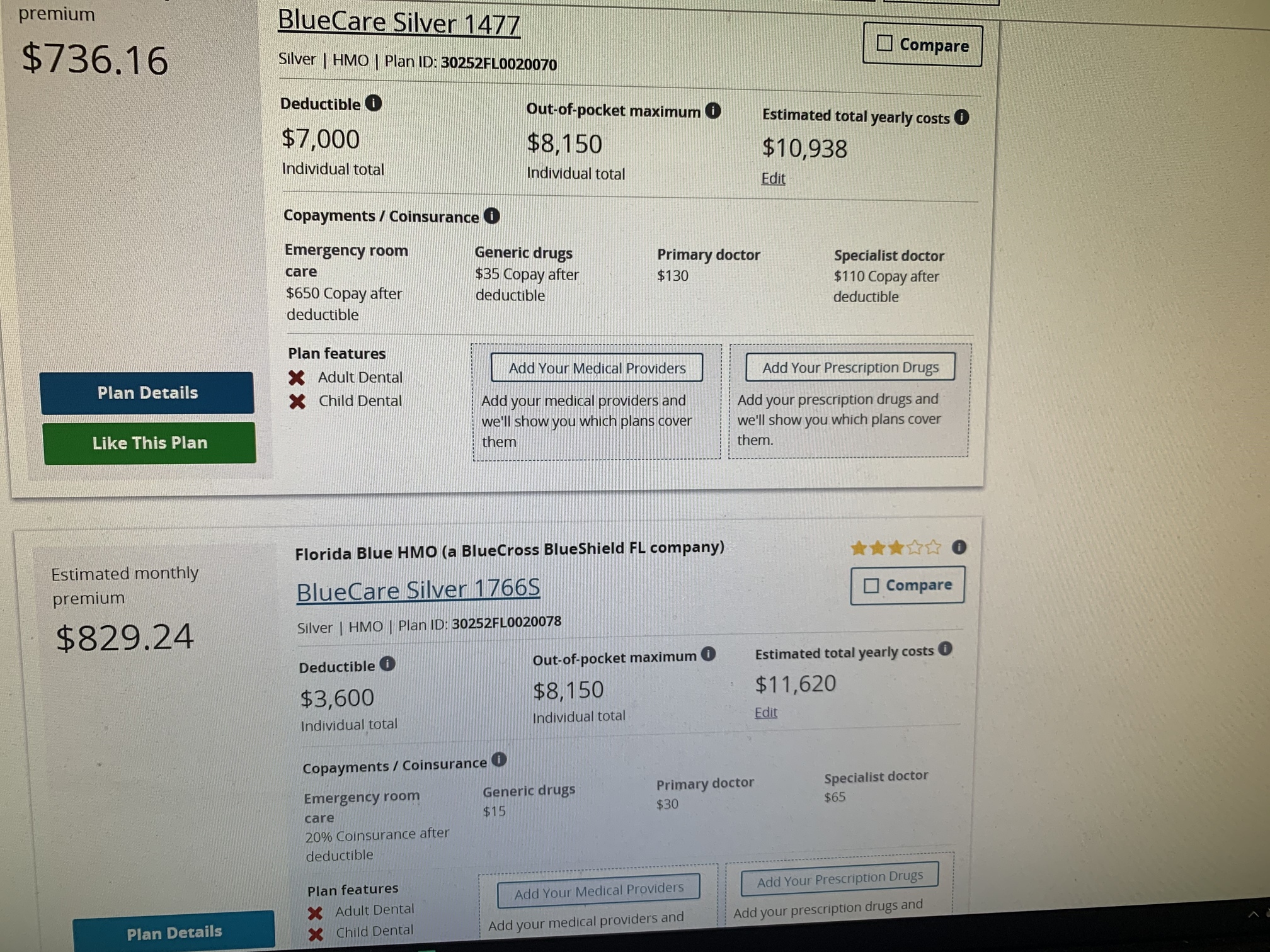

The monthly premium would actually be more than that. Note that the quoted premium includes a subsidy(“Tax credit”) of over $300 per month. That is based on my current salary. Obviously I’m not changing companies, especially to one which doesn’t offer bennies, for the same pay. So I’m probably not getting all of that subsidy, if any of it!

This is a silver plan. I only selected this plan because it’s roughly equivalent to the one my current employer has in place now. Bronze plans are much cheaper per month, but the deductibles are typically much higher. Also instead of 20% coinsurance, you’re looking at 40-50%. It’s absurd. It’s barely insurance.

But anyhoo, based on their “estimated total yearly costs,” I’ll need a minimum $18,984 salary increase at the new gig just to break even. Why even bother? There’s no way they’re gonna do that.

Not to belabor the point but the healthcare system here is really insane. I’m lucky enough to have “good insurance” where our prescription co-pays are $0 or like a quarter. Or for example, this weekend I was an idiot cutting some vegetables and cut right thru the top of my left index finger/nail. The visit to the walk-in and subsequent follow ups are going to cost me like $10 total. I couldn’t imagine having to deal with that situation happening and thinking to myself “well let’s not go get this fixed ASAP because I can’t afford it”.

During the experience I’m sitting there in the exam room and they ask me exactly what type of insurance plan I have, so I have to dig through my wallet with one hand while the other is bleeding to find my insurance card so they can figure out which type of drug they can give to me that’s covered. Absurd that a simple medical decision like that is governed by your type of insurance plan.

Other than that the doctor was great - he tells me to stick my finger in the iodine “because this will disinfect anything… Well disinfectants work on almost everything, not COVID, despite what some government officials will tell you.” Got a chuckle out of my despite being in some obvious pain. To distract me while he’s stitching me up he tells me about his brother who is deplorable-adjacent. 10/10 would go see him again.

I’m not sure of the point of this post other than to wonder how we can really convince others UHC is a better go, especially for people like myself who are fortunate not to have to worry about it. I think though that (as with every other topic) unless it directly affects the conservative person, they don’t want to change it.

Every time I see this stuff it just makes my blood boil.

I got another I surance denial letter yesterday saying I owe $1,000 for lab work that was drawn at the place I get a monthly infusion. The place is obviously in network, but the lab is not. They drew the blood right from the IV. This is after I met my $5,000 personal deductible and $10k family back in January.

I’m still paying my son’s emergency room bill from November. And my wife had a breast cancer scare earlier this year (it’s all cool, hence “scare”), which resulted in a bunch of tests that we are also still paying off. Technically we could have paid them in one shot, but it would have been a painful shot, so we got on a payment plan for both.

Which reminds me, need to pay $250 on one of the payment plans today.

Unless my book sells like crazy, I’m probably going to do w/o insurance for a while. There’s no point paying those rates while I’m traveling and being a nomad.

Although what do I do if say I settle down and come back to the US at 55? It’s going to be tough to come back to the US where heatlhcare costs 10x more than say Mexico or Costa Rica. USA #1 healthcare may be the driving factor in where I live from 55-65.

For the year my oncology med just 700000 with one last MRI next week next (please god) - so I have 300 K or so for the rest thru Nov to get my sweet Medicare kicks in. Others I pay nothing from our insurer than pocedeor.

This is some straight up Lyin’ Ted right here. Mifepristone has been around as long as I’ve been alive. It’s an abortifacient, but it’s also the only glucocorticoid receptor antagonist that’s ever existed and, as such, is used as one pharmaceutical option in Cushing’s syndrome for people in which surgery is contraindicated. It has some side effects, but typically not severe or irreversible ones, which puts it ahead of the curve of most other drugs used to treat hypercortisolism in that regard.

It is on the World Health Organization’s List of Essential Medicines.

Serious complications with mifepristone are rare with about 0.04%-0.9% requiring hospitalization and 0.05% requiring blood transfusion.

Didn’t catch this before but #neverforget that these are still the players Skipper Chuck is penciling in on the lineup card before he hands if off to the umps:

I think if we can get people with good, employer-based insurance to ask their company how much the company pays, it’ll go a long way. Finding out that a company was paying $1800 a month for two people in their late 20s was insane, it’s just an absurd amount of money.

I really believe that if instead of hiding the employee cost of health care in your pay stub (also which nobody reads) and instead getting that money as pay, and then billed every month by BCBS or whoever, real progress would be made towards M4A.