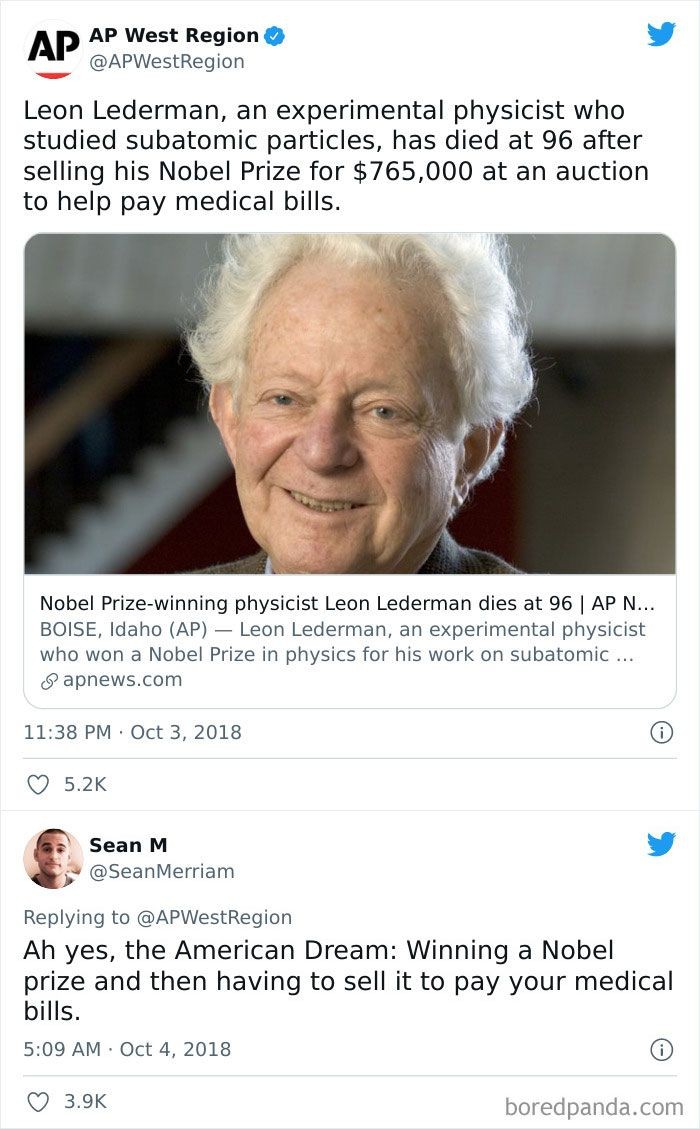

I’ve run into this issue with my $14k/month medicine. My dad, who has extensive experience with insurance, explained that a lot of insurance providers are disallowing copay assistance because the out of pocket maximums are designed to be painful. They are there to make you not want to use your insurance. The point is to make you avoid getting the care you need. When the drug company covers your oop max you are more likely to then you your insurance for stuff like going to a doctor when you are sick instead of deciding it’s not worth it.

Can you contact the drug company and see if they’ve run into this issue before? They may know how to get it paid without it showing up as copay assistance.

Great system we have.

ETA: One workaround I’ve seen is for you to pay out of pocket then have the copay assistance program reimburse you directly. Obviously that carries some risk and is more work/headache, but if the drug company is willing to work with you that can resolve the issue.

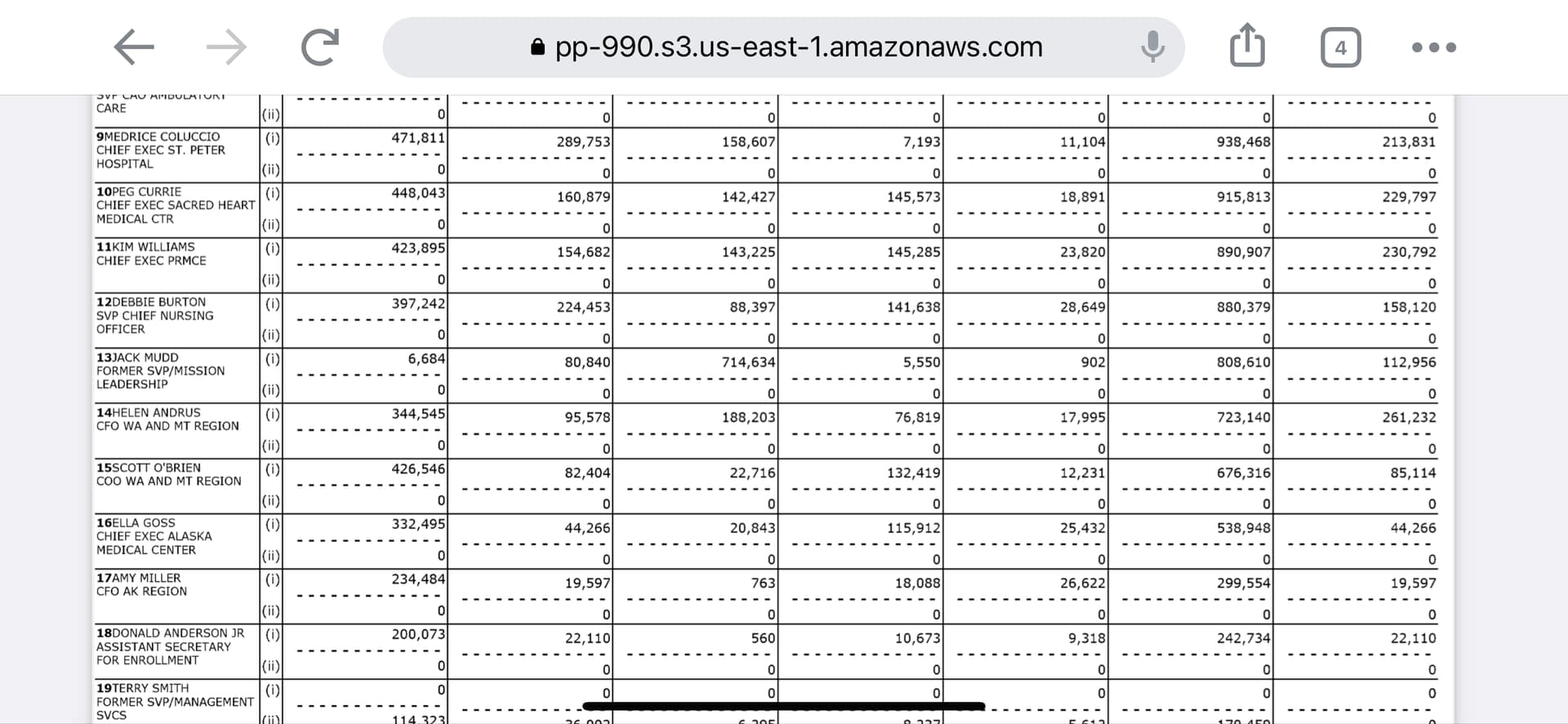

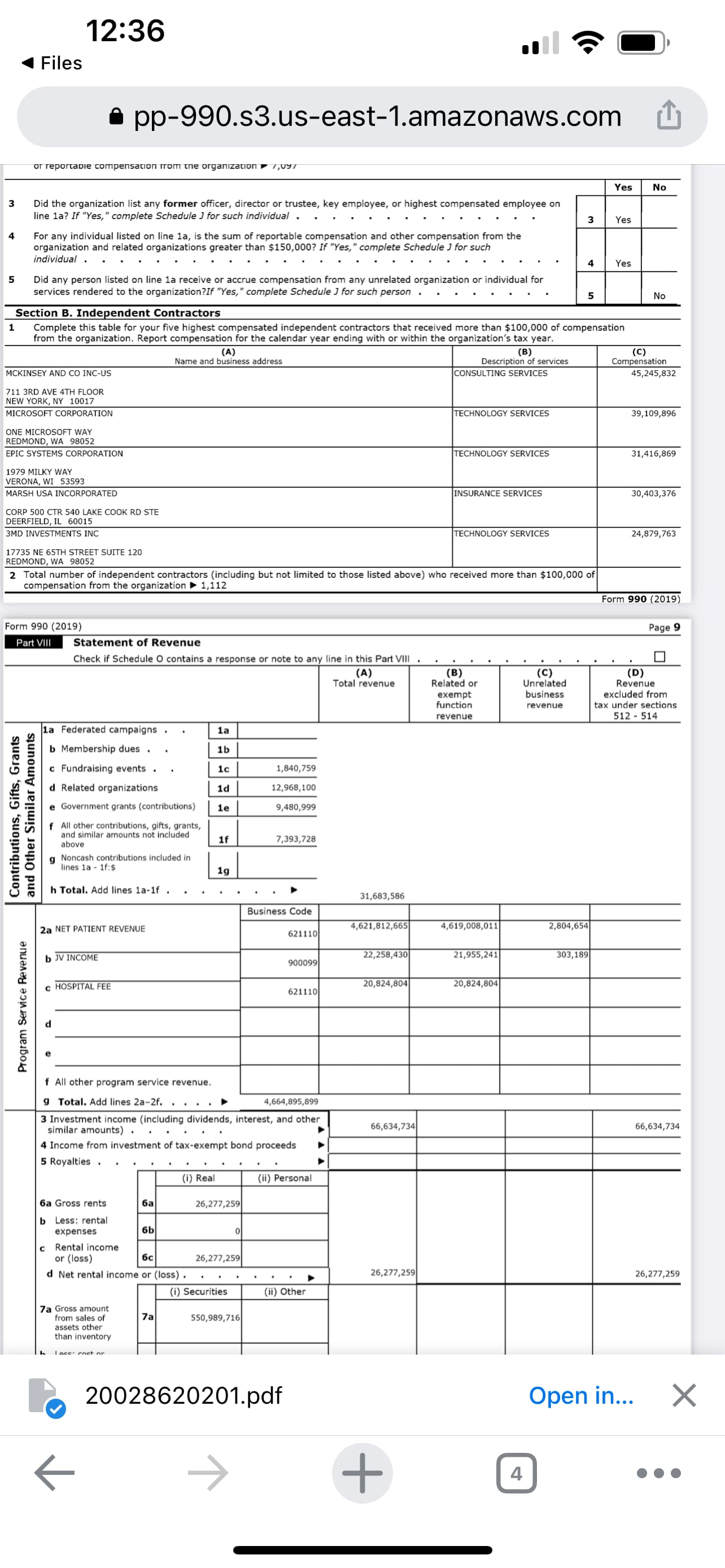

One of the things the article touches on is that while many of these hospitals have to provide free care to low income patients, but they don’t have to make it easy.

They hide the fact to patients and do everything to frustrate and alienate these people and make them afraid to actually use the hospital. Meanwhile providence is sitting on 12 billion dollars and gets over a billion dollars a year in tax breaks, but only spend less than 1% of their earnings on charity.

Chatted with my Providence friend Saturday. They all knew the story was coming but she hadn’t had a chance to read it yet.

With that said, she said that the Providence’s mission is to provide health care to as many people as possible, regardless of circumstances. Some people do fall through the cracks, especially if they the patients don’t make any efforts to contact the hospitals about making financial arrangements. The Rev-Up thing happened before she joined the C-suites so didn’t have any information about that. In regards to Providence making money and having investments, she said that all of that is in driving their mission. The more money they are able to make, the more they can help people. They were facing huge shortfalls a few years ago and had to figure out ways to earn money in order to keep their mission alive.

In defense of Providence, I can share my story. When my wife was 6 months pregnant, she lost her job, and she had the insurance. I went to our local Providence hospital and told them we were having the baby there and we had no insurance an no money (we weren’t in great financial shape 10 years ago). I explained to them that they could pay the $1200/mo COBRA payment for the next 3 or 4 months and they’d still make $5-$10k from insurance paying for the birth. They ended up doing that for us.

A surprising number of those people actually drink the koolaid. They really believe it. So when they’re peddling it, it’s the honest truth as far as they are concerned.

I’m not sure if this is better or worse, but it’s definitely a thing.

Oh, it’s definitely talking points. The only question is how true she believes them to be. And I suppose if you are less cynical, how true they actually are.

Decide I need medical care. Am I dying in the next 15 minutes without it? If yes, proceed to nearest hospital. If no, confirm that it’s in network before leaving the house.

Get medical care.

Politely decline to pay anything more than a copay.

Doctor’s office bills insurance

Doctor’s office bills me. I politely ask if they billed insurance, politely confirm that they used the right insurance policy, politely confirm that my insurance company received the claim, and politely inform them I’m good for whatever I owe but not until the insurance company confirms what I owe, so go ahead and just send me whatever paperwork you want. Some of these steps can often be done online, so I can non-politely curse under my breath about the shit show that is the American healthcare system while doing them.

Insurance company sends me the report on what they paid and what I owe.

Double check that I’m not over the maximum and that what I owe matches what my plan says I should owe.

Pay what I owe.

Hope I don’t get a collections notice six months later. So far, it hasn’t happened.

I’ve gone past the DUE DATE on the bill numerous times with this plan, and it’s never actually caused any more of a problem than them re-billing me or calling me about it, despite the fact that it says DUE DATE in red all caps bolded font with underlines under it.

Well there’s freeroll equity on both ends. If you pay up and the insurance pays up, the provider got the double-dip payout. If you pay up and the provider stops billing the insurance company, the insurance company realized the freeroll equity. The only person in the game who cannot win is the patient. The patient will, at a minimum, be on the hook for every bit of what they’re supposed to owe.

This is all begging for a massive class action suit. It feels like insurance companies kind of followed the ACA for a while, then realized that it’s way more profitable to deny stuff they aren’t actually allowed to deny and then go, “Oopsie! We’ll get right on that!” when you call them on their bullshit, because plenty of people will fall through the cracks by giving up or misunderstanding the situation, and virtually nobody ever sues them because who the fuck can actually figure out what they’re actually not allowed to deny?

This is my favorite part of the American healthcare system. Every now and then I get a letter in the mailbox from an insurance company or medical provider, and the chill it sends down my spine on the way inside to open it hoping that it’s not the bill out of nowhere that’s going to fucking bankrupt me makes me truly feel alive.

GOD BLESS AMERICA, LAND THAT I LOVE!

The insurance company is more like: “Let’s pit the hospital and the patient against each other and see if we can get one of those dumb fuckers to just give up!”