Assuming an 8% return for 30 years your money will increase by 10x at retirement. You should be considering how much the withdrawl will cost now vs paying it off using your future income. Your estimate of $100k to pay off the $65k debt after penalty and taxes (all at your marginal rate in 2020 or higher) sounds reasonable. So with compound interest you’re giving up $350k.

Have you considered your options for negotiating or restructuring the debt?

Since you are not in a huge rush because you’ve already determined that waiting until 2020 is the better move tax wise, I think you should register for an account on the bogleheads forum and ask for advice on your specific situation. Be prepared to share budget info, income, etc. You will receive very good advice assuming you are willing to share the info they ask for.

I don’t believe there is any way to know for sure. In the late '80s and early '90s we were supposed to be doomed due to US debt burden and Japan buying up the world, etc. Dozens of books were written and all the financial people explained how royally fucked the US was.

Since then the market has increased massively, with of course a few big bumps in the road, but for the most part straight up.

I think it was 2010/2011 that all the finance geniuses on 2+2 were talking about the big correction that was coming and how they were 100% cash and would have lots of “dry powder” to invest into the meltdown. Wonder if they are still waiting?

US politics are a complete mess. The US is hopeless when it comes to competent fiscal policy. Monetary policy is increasingly politicized. The debt is, at some point, going to be an issue.

Demographics are bad. Thanks to boomers, millennials don’t have any fucking money and can’t afford houses and kids. Further, the US consumer is already up to their eyes in debt, a bubble that is sure to burst eventually.

Not really. The counterpoint is that we have the capacity to make more stuff every year… and the older I get the more I suspect that money isn’t real, never has to balance, and that we’re just pretending to know what’s going on.

When idiots insist that stocks go up forever I always point out that if you invested in Japan’s market in 1987, you still have lost money on your investment in 2019. As you’ve noted, it’s a completely different long term than the previous one outlook wise in the US right now.

As for me, I look more at specific stocks/industries nowadays than I do overall markets. I was bearish this year but mostly went against the stuff that gets out there in the public hype sphere (ie when marijuana stocks got ridic on them–the market took forever to finally correct that nonsense and yet I still didn’t really get much there as I was a little too soon entering that one) tl;dr everyone can be a moron for a long, long time.

I’m actually overall bullish this upcoming year. So the market will tank hard, sorry.

I’m trying to navigate a mortgage refinance right now, and I wonder if anyone can help me think about some variables in the process. Here are the facts:

My house is worth somewhere between $500k and $600k. It’s hard to predict how it will appraise. It’s about 2400 sq ft, 4 BR/3.5BA townhouse (although I think it’s technically a “condo” for mortgage purposes–no idea what’s going on here). The curveball is that one of the three floors (which includes the master bedroom) is a terrace level, and I have been told that appraisers don’t count rooms/square footage that are below grade.

Debt that would definitely be part of the refi (total of about $340k, call it 60% LTV if that is a magic number):

First mortgage (15-year that is 8 years in): $211k @ 2.875% fixed

HELOC for renovation (I have no idea how the payments on this work): $130k @ 4.03% floating

Optionally, I have about $125k of student debt at rates between 4.25% and 4.56%, mostly floating. I’d like to roll as much of this into the new mortgage as I can to save on interest.

Assume tons of income and perfect credit. Other debt includes about $50k of student debt and about $100k of car loans.

As I understand it, this is going to be treated as a cash-out refinance because the HELOC doesn’t count as purchase debt. I think, but am not certain, that it doesn’t matter whether the cash-out uses are limited to the HELOC or whether they also include the student debt.

What I would like to understand better is:

Are there any magic numbers (either LTV or absolute dollars) that I should be mindful of? My primary goal is ultimate interest savings, although it would also be nice to extend the maturities a bit if the rate is good. If we assume a home value of $550k, the weighted average rate on the debt I would payoff with a 60% LTV loan is 3.29%, 70% is 3.45%, and 80% is 3.55%. That kind of suggests 70% as a sweet spot if that is a magic number?

When I got my renovation loan, I didn’t have to pay anything at closing. What I’m seeing with a refinance is that even if lenders are advertising that there are no “fees”, there are usually a bunch of closing costs at a minimum, and often there actually are substantial origination fees or points or other charges. Is it possible to get a genuine no-fee refinance, or do I just need to bake the upfront costs into the analysis?

Any good lenders/places to find lenders out there? A lot of the search tools I have found have been pretty disappointing and obviously optimized for generating referral $$.

I don’t have much to say, other than I’ve been through a similar process recently. Some random thoughts:

I worked with a mortgage broker that I had used when we first bought the house in 2010. I’m sure that cost me some unknown dollar amount, but I was happier dealing with a single entity than interacting with a bunch of direct lenders.

I took out a $380k mortgage, which included about $60k of cash out. The house appraised at $585k, which was deemed “acceptable” for my refinance transaction, according to the broker. That’s right at 65% LTV, but I’m not sure if going to 60% or 70% would have changed the rate I got (3.625% on a 30-yar fixed in September 2019). Given the scummy nature of some lender/appraiser relations, it wouldn’t surprise me if the broker/lender said to the appraiser, “this thing needs to appraise at at least $585k”, which would imply that the 65% LTV threshold actually was meaningful.

My reading of IRS publication 936 is that interest on the cash out dollars used to pay off the HELOC wouldn’t be tax deductible, but I could imagine an argument to be made that if the HELOC was originally used to purchase or substantially improve the home, then paying off that HELOC would result in tax-deductible interest as well. But I’d want a tax attorney’s blessing on that before trying it. (Aren’t you a tax attorney?)

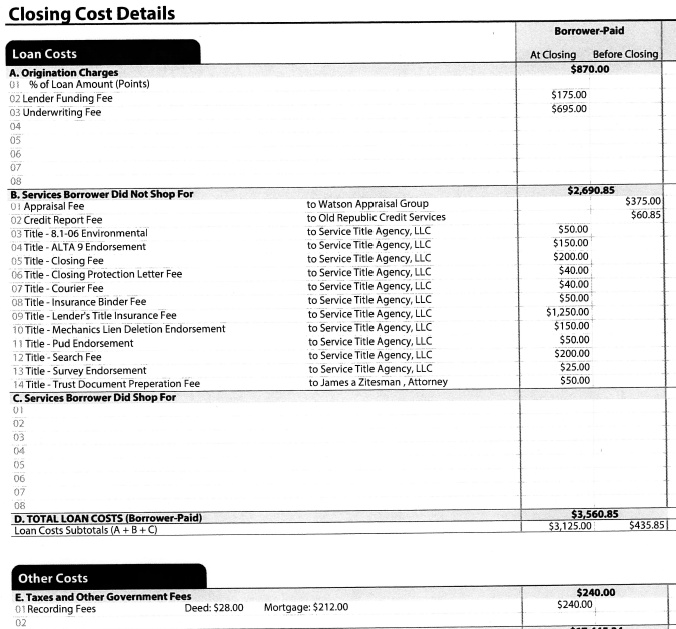

It’s hard to imagine there being a no fee transaction - the only question is how those fees are going to be captured. I paid just under $4k of fees:

Maybe some of those fees are scams, but I assume that most of them are effectively mandatory and, again, the only question is whether they get rolled into the loan balance (as mine did), whether they’re paid upfront, or whether they’re baked into the interest rate.

The idea of taking out a HELOC or refinancing in order to pay off student debt is interesting because you could view it as converting non-bankruptcy eligible debt into bankruptcy-eligible debt.

Mostly I’m replying because I want more information on the $100k of car loans and what you’re driving.

Thanks! I think it is pretty clear under Reg 1.163-8T that you trace the use of debt through refinancings, so as long as the HELOC is traceable to renovation costs, then I feel pretty good about the refi mortgage being a substantial improvement loan as well.

I double checked and the car loans are actually $125k . In my… defense?.. it’s two new cars we bought at the same time to replace 2007 and 2009 cars. But yeah, one of them is a very sweet Tesla Model X. I’m saving so much on gas!

This is interesting - thanks for the reference about tracing. Two follow-up questions this raised:

Do you know how this notion of tracing would affect the treatment of student loan interest? For example, suppose I took out student loan debt, then paid off that debt using the proceeds from a HELOC. Would the HELOC interest be deductible as student loan interest, since the proceeds could be traced back to educational expenses originally funded with a conventional student loan?

Do you happen to know how a refinancing of a student loan via a HELOC would affect bankruptcy treatment of student loan debt? If you can convert bankruptcy protected student loan debt into bankruptcy eligible HELOC debt, that would seem like a smart thing to do for someone looking to declare bankrtupcy. (Of course this assumes that the lender would be dumb enough to offer a HELOC in this scenario.)

I also seem to remember reading something about how extending the life of an existing loan via a refinance changes the characterization of that loan (makes it harder to consider it a purchase loan), but I don’t recall the details.

Congrats on the cars. I had actually assumed that you typo’d $10k of car debt into $100k, but your reality is more interesting.

Hopefully you’ll keep the thread updated with what you end up doing.

Notice 88-74 has the rules about tracing for acquisition indebtedness purposes.

On student loans, a qualified education loan has to be incurred “solely” to pay qualified higher education expenses (section 221(d)(1)), so if you refinance a QEL together with other debt, the interest is no longer deductible (at least as student loan interest). The preamble to the 2004 regs says this:

Another requirement of a qualified education loan is that the borrower obtain the loan solely to pay higher education expenses. One commentator suggested that if a taxpayer refinances a qualified education loan and receives an amount in excess of the original qualified education loan, the taxpayer may take an interest deduction under section 221 for interest paid on the refinanced loan. The commentator is correct, but only if the taxpayer uses the excess amount solely to pay higher education expenses and satisfies all other requirements of a qualified education loan. Thus, if the taxpayer uses the excess amount for any other purpose, the refinanced loan is not solely to pay higher education expenses, and no interest paid on the loan will be deductible.

I have no idea about the bankruptcy question. Intuitively, it’s hard to see why a mortgage lender should get more protection on a cash-out mortgage if the excess debt was used to repay a certain kind of lender, but it’s possible they just do.

Judge discharged about $225k in student loans in bankruptcy yesterday. Would not be surprised to see more of this, and probably wouldn’t repay student loans beyond the minimum required payments at this point (assuming a reasonable interest rate).

Wife is supposed to have 6 payments left and then government forgiveness on $200k worth of student loans. Our fingers are crossed that Florida Man and Betsy don’t fuck us over.

. In my… defense?.. it’s two new cars we bought at the same time to replace 2007 and 2009 cars. But yeah, one of them is a very sweet Tesla Model X. I’m saving so much on gas!

. In my… defense?.. it’s two new cars we bought at the same time to replace 2007 and 2009 cars. But yeah, one of them is a very sweet Tesla Model X. I’m saving so much on gas!