First order effect - Anybody w/ exposure to oil in America is fucked. Not only producers and their lenders, servicers, etc. but entire cities and even states.

Second order effect, which we all already know for a fact but refuse to acknowledge - um, the reason there is so much oil is because economic activity has grinded to a halt.

How much of that activity will come back to previous levels immediately after Covid is gone? Conversely, much will come back slowly and haltingly. How much will never come back? People are being way too optimistic about how much falls into the first category.

Yeah, if you bought it through a broker, I think the broker ends up with a receipt for that oil in your name, and gets charged for storage and transportation fees, which they then charge to your account. So they bleed your account down for those charges until you go busto. Surprisingly hard to find concrete language for this contingency, though.

I somewhat agree with this, have a lot of liquid cash and I’m not sure what to do with it. Buying stocks at current prices seems crazy. GLD? I keep asking about what to do if you have inflation fears, I guess I should move cash to GLD or TIPS? But Treasury Inflation-Protected Securities were down big during the crash, contrary to what I’d have expected. Should I buy shares of an ETF or actual inflation-protected securities? Can they even be bought by an individual?

All of this stuff makes me feel like such a newb, which is scary because I’m sure a huge percentage of the population is totally clueless compared to me, and I feel totally clueless.

Ultimately it seems like if shit gets wild from this, it gets really wild, and predicting the fallout in order to hedge against it is difficult.

So essentially the difference between the June and May prices is just “how much does it cost to arrange for storing oil for a month with no planning or foresight” and the answer is apparently like 40 dollars a barrel.

Or maybe worse than no planning or foresight, since the person arranging the transport and storage has no reason to spare expenses and is likely highly amused by this whole scenario.

I think so, as long as “storing” includes transportation. I’ve done an amazing job today proscratinating in my real work by trying to read up on oil futures. As I understand it, there are significant storage facilities in the Oklahoma location where physical oil delivery takes place. So normally, you’d just pay a rental fee to them. But now, the local storage facilities are more or less full, so it’s a question of either transporting oil yourself or figuring out how much to pay the supplier not to deliver.

Looking at the terms of Western Canadian Select heavy crude futures (rather than Western Texas Intermediate) suggests that you need shipper status on a particular pipeline in order to be eligible for physical delivery, which makes sense - every entity who could conceivably take physical delivery actually has some capacity to do so. I don’t think that’s the case with WTI crude.

I think everyone else is talking about something else. That we are in the middle of a black swan event where traditional model of risk to earnings are failing, you cannot just look at past variance to assess risk. This has major implications for both 1 and 2.

Regarding 1, in the bad case but realistic case, this will likely making earnings negative for many companies until they are bankrupt, and for much longer than investors are currently expecting (no back to business as usual this year). Investors are pricing stocks as if earnings expectations are only 10% below where they were at beginning of the year, when the reality seems to be most companies are losing money.

Regarding 2, investors should be demanding a much higher risk premium because traditional models of risk pricing based on the variance of the asset class can be thrown out the window when we are in an economic storm that has not been seen in a hundred years. There is nothing like our current situation in the range of any asset pricing models. A 5% premium over risk free rate makes no sense if you think we are 25% risk of complete collapse in a range of industries like oil and gas, travel and entertainment, brick and mortar retail, corporate real estate, even many sectors of healthcare. this collapse would lead to demand destruction in other industries like housing and automotive.

I’ve already told you, buy that 3x short ETF tied to 20 year treasuries. Long treasuries will get absolutely killed if there is inflation significantly higher than current expectations. TMV.

I would suggest just holding a little GLD along with your cash to put your mind at ease, but it seems like the risk is still toward deflation. If we do see inflation it will likely come gradually.

You should do a quick google on the relationship between velocity of money and inflation and then think about what the virus is doing to the velocity of money. This effect is probably greatly outweighing any printing by the fed at present and I think it will take a while until it picks up again.

Right. The reasons WTI is the benchmark are 1. It’s used a lot because it’s relatively easy to refine and 2. Cushing is the main US pipeline hub, so it’s easy to move the crude. Canadian oil is lower quality and has less pipeline service.

I still don’t get it. If inflation is higher, inflation protected securities get killed? This makes no sense. And holding a triple leveraged short as a hedge for 6+ months seems crazy.

I’ll Google that tonight. What’s a little, as a percentage of net worth?

I can make some sense of the value of the market overall. While many firms will be severely impacted there are many firms with exceptionally strong balance sheets who are likely to consolidate industries in this political environment (zero antitrust enforcement). There is also a ton of cash on the sidelines dying to finance new entrants into decimated industries.

Not inflation adjusted bonds. Regular government bonds. 20 year treasuries are yielding 1.04% right now. If inflation is an actual concern then that yield would go up. Way, way up. Who would hold a 20 year bond yielding 1% in an environment with significant inflation? No one. So that yield would get bid up and long bonds in particular would get absolutely destroyed.

I agree that a triple leveraged short bond ETF is very risky but it would also be an extremely effective inflation hedge. If you’re looking for a safe inflation hedge, well, I can’t think of one that exists.

I mean stocks are an OK (not great) inflation hedge but you don’t seem too thrilled about that. Having a fixed-rate mortgage would be great in an inflationary environment and is probably the safest one around.

I agree with a lot of this but the current indexes are comprised of current companies. A lot of which are going to zero. Now i agree that AMZN and the like might just gobble everything up and their stock may soar and it balances out (This is basically already happening as you alude to. A handful of companies are a huge % of the s&p 500 today) but at some point I have to imagine we would actually enforce antitrust laws.

Narrator: They did not enforce anti-trust laws.

(Nah jk we are going to just have Amazon, Costco, Brawndo and Buttfuckers at the end of this like the Mike Judge prophecy foretold. Hopefully getting to see Beef Supreme work in person in a packed arena balances that out).

Aren’t Treasury Inflation-Protected Securities indexed to actual inflation? So if I bought the iShares ETF TIPS, wouldn’t it go up if inflation went up?

One of the biggest hoarders of crude is the federal government. A month ago, Trump wanted to fill it with 75m barrels, but Congress didn’t approve the money in the Stimulus. I guess now he doesn’t need an appropriation. Someone has already floated this to him, he likes the idea.

I thought it might be useful to look at some industry-level data in an effort to assess what a “right” level of market correction is for the coronavirus. I was lazy and didn’t pull the data myself, but NYU Finance Professor is one of the world’s leading academics in terms of valuation, and makes a ton of data available on his website. I’ve pasted the most relevant one into a google sheet here:

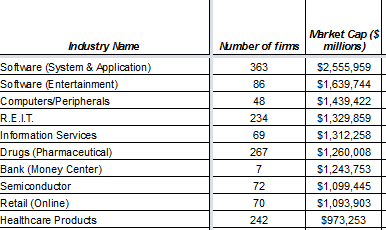

The reason why I thought this would be useful is that people can play around with the specific industries and the likely hit those industries will take in order to assess how that would influence overall market caps. Here are the 10 industries making up the largest percentage of aggregate market caps as of the end of 2019:

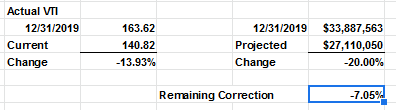

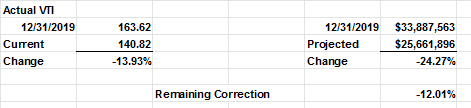

In total, they make up just over 40% of aggregate US market cap. There are 94 listed industries overall. Toward the right, there’s a haircut column where you can input what you think an appropriate loss in value would be for the aggregate industry. I started by just wild-ass guessing 20% for each industry, even though some industries are obviously going to do far worse than others. At the bottom, there’s an aggregate projected market cap based on the haircut numbers, and a calculation of what those haircuts would imply in overall market values. For comparison, you can see what the overall market (as proxied by VTI) has done year-to-date in 2020). In the sample world where every industry loses 20% of its value, the outcome is obvious - the overall market should have lost 20% of its value:

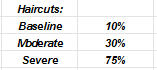

Year to date, assuming I haven’t dorked anything up, the market has actually gone down about 14%, so you’d say current levels imply a further 7% decline. But where I think this gets really interesting is if you play around with some of the harder hit industries. The current version of the sheet has three broad inputs: a baseline estimated effect, a moderately worse effect, and a severe effect. Right now, I’ve plugged in:

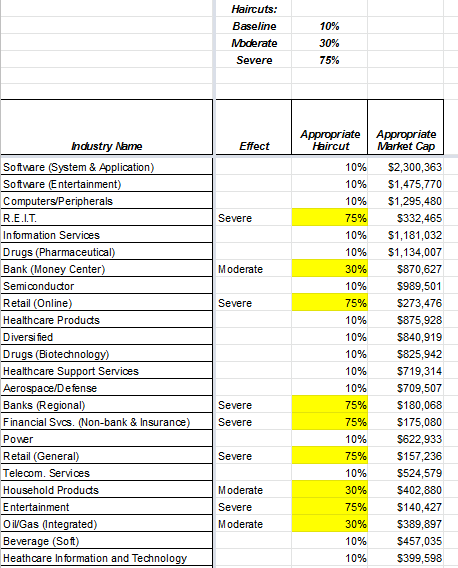

And I haphazardly applied those estimates to the top 20 or so industries as follows (baseline assumed unless cell is highlighted):

So of the big industries, this hits banks, REITS, and Retail really hard, with every other industry down 10%. The effect on aggregate value:

So in this much more severe world, the total year-to-date drop “should be” about 24%, which leaves another 12% drop from today’s prices. So go play with these numbers if you’re interested, and see what your assumptions do to aggregate implied market values. For me, it’s pretty reassuring that even a pretty pessimistic view implies only a 12% downside from here. And I think a big reason why that might seem out of line with the obvious business carnage around us is that the very visible industries (restaurants, theaters, hotels, casinos) don’t actually make up a huge percentage of aggregate market values, so total destruction in those industries doesn’t actually affect aggregate market values all that much.

Anyway, curious what UPers best estimates are, and what they imply for future returns.

I was suggesting it more for your own peace of mind, so it is more about how much makes you feel better.

Of the money that you have, that you could invest in stocks but don’t want to because of risks to stocks maybe keep 20% gold and 80% cash? I am not aware of a standard advice for this scenario because standard advice is always to stay in the market and regularly rebalance between stocks and bonds according to your risk preference.