Sorry I can’t help myself

Just need some vintage Chanel stuff lying around baby

Maybe millenials would have some Chanel they could use if they weren’t wasting all their money on avocado toast. Whatabuncha babies, oh I don’t have any Chanel vintage clothing, wah wah wah. Typical.

Maybe I’m missing the joke, but it sounds like she buys the shit, turns it into necklaces, and then sells it at a ridiculous markup.

I get she probably started with some of her own stuff, but it seems like she is actually more or less running a legit business.

This whole thing is way over my head. I think someone is going to need to ELI5 it for me. I do find the whole thing pretty crazy but I don’t think in the exact way everyone else seems to.

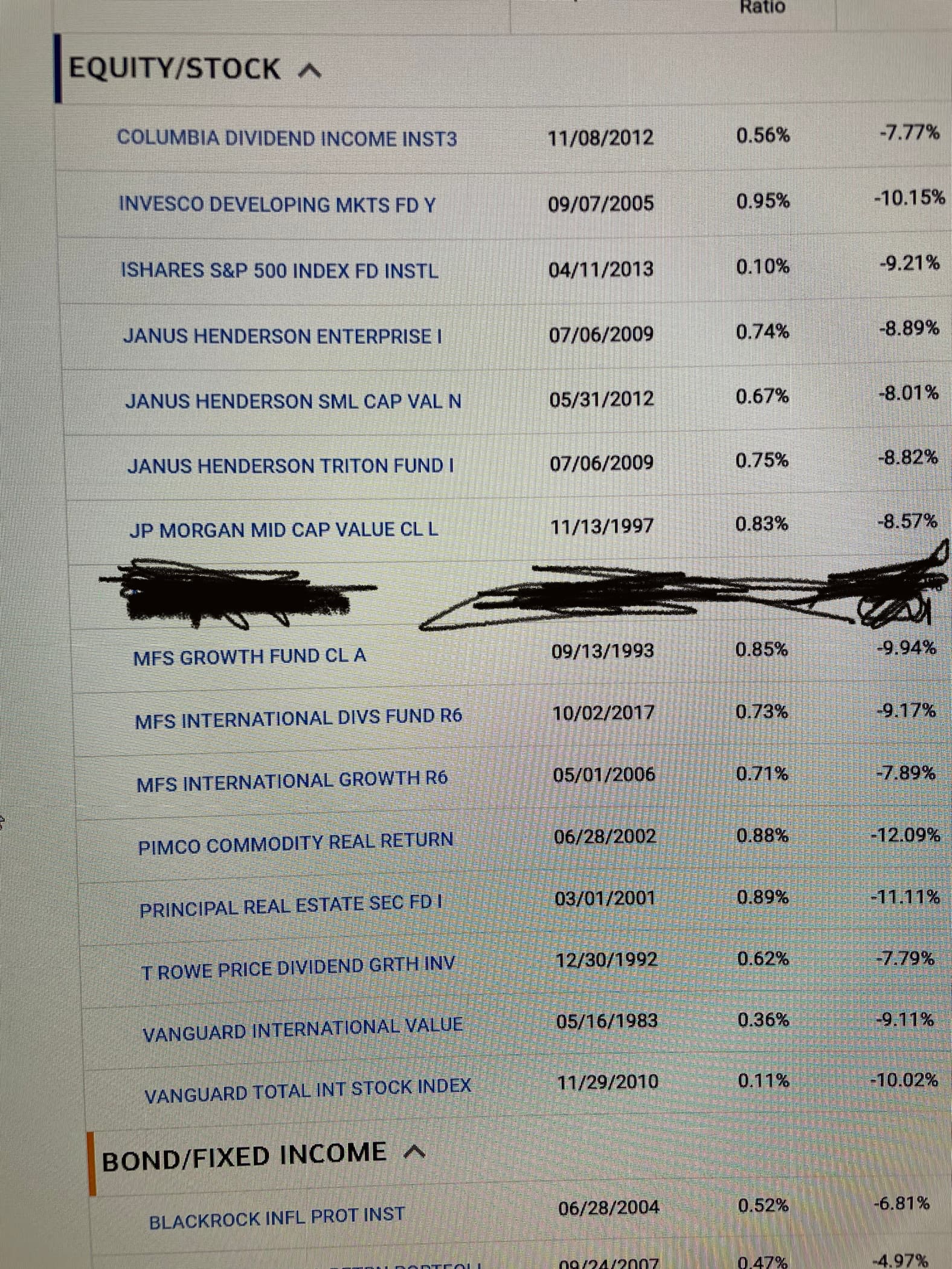

Is BSPIX fine to dump all of my domestic 401k contributions? The rest of them seem pretty bleh with high expense ratios. This one is at least at 0.10%. They offer vanguards international funds which I’ll go with for that.

I’ll probably rollover my previous 401k as well if you guys think BSPIX and VTIAX are good enough.

Thanks!

It seems to check all the boxes for a standard useful US equity investment (low cost , passive) but 10 bps is a bit “expensive” relative to some other institutional equity index funds. Vanguard’s is basically free, it’s like 3 bps.

It’s the cheapest available by far. Here is the full list. I didn’t really want to rollover my existing 401k into an IRA but only have 1 decent fund will suck.

1 Like

If you’re looking to do the Boglehead style index fund route, you probably want low expense versions of total us stock, total international stock, and total bond markets. As noted, .1% is higher than the Fidelity/Vanguard index funds which are probably something like .03%. So, if you could get all of the exposure you want at .1%, the question is whether it is worth the difference between burning $1.00 per $1000 invested in your 401k annually, vs. $0.30 per $1000 using lower cost stuff.

Problem is you only get a S&P 500 index, so if you use that for all of your domestic stock exposure, you’ll be more heavily weighted to large cap stocks. Can’t see the bond offerings if that is relevant to your desired asset allocation.

So I guess its a pretty meh 401k menu, but probably livable on the expense side, if you can get the right mix of domestic/intl/bond exposure for your desired allocation.

If you’re doing some other kind of allocation, good luck have fun no idea put it all in TSLA and DASH ldo imo.

1 Like

I don’t have a bond allocation at this point. Maybe when I get closer to 40. Currently at 70% / 30% international.

Here is probably a dumb question: is the expense ratio based on only what you put in that year or the entire balance of your account?

Calculated and charged annually, based on the value of shares you have in that particular fund. Think of it like your annual fee for owning shares of that fund.

2 Likes

Makes sense. I wouldn’t sweat 7 bps too much, the most important thing is to not be spending a lot on fees where there is a very dubious value proposition. Even if you have $1 million in the fund 7 bps is only $700 a year, which is not going to make or break your retirement.

1 Like

Yeah what you don’t want is to have your whole portfolio rocking those predatory funds that clip you for 1% of your portfolio balance annually. There are some pretty sick graphs that show how gross that ends up being over decades of compounding.

Wasn’t there a thread on 2p2 where someone was asking for financial advice and it turns out that the funds they were invested had like a 10% front load fee then a 2.5% annual fee on top of that?

Yes, very much this. The compounding of fee erosion over time is basically the same math that shows that compound interest is super powerful. Compound fees are equally devastating.

Sounds like the American Funds a dude at Wells Fargo tried to sell me on when I had a few K there. A quick google revealed what was actually up and I immediately withdrew all my money from Wells Fargo.

Yeah it was the same “American Funds” which seems like a massive scam. EddyB was the one getting ripped off.

CDL breaks down the details here.

Fucking hell 7%

IIRC the bank guy selling you on that fund gets a commission so of course they push it relentlessly to take advantage of people who aren’t aware